[Economic Insights] Revising the outlook for NZ growth and monetary policy

2 views

Skip to first unread message

Bevan Graham

Jul 6, 2015, 11:20:06 PM7/6/15

to worldview...@googlegroups.com

Recent weak data on dairy prices, business

investment and business confidence has seen us shave a bit move off our GDP

forecasts for New Zealand.

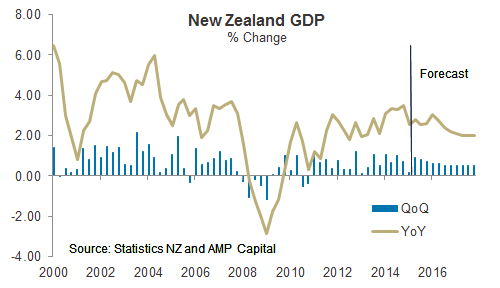

March quarter GDP growth disappointed as the

summer drought and lower oil exploration took a greater toll on the economy

than we expected. On the expenditure

side of the accounts investment spending disappointed most of all. Investment data can be volatile but the

decline appears consistent with the recent decline in business confidence, as

signaled by today’s release of the NZIER’s Quarterly Survey of Business Opinion

(QSBO), so it’s hard to dismiss as just volatility. Lower business investment clearly also has

implications for future growth.

In light of the continued weakness in dairy

prices and lower confidence levels we have shaved a bit more off our GDP

forecasts for this year and next. We had

already assumed a moderation in quarterly growth rates from the middle of this

year as both the Canterbury rebuild and net migration peak – we have simply

accelerated the pace of slowdown.

Our previous forecasts had annual average

growth at around 3.0% in 2015 and 2016, but this now looks like being closer to

2.5% in both years before a further dip down to 2.0% in 2017.

These forecasts are not as pessimistic as

some in the market as we put some weight on some positive offsetting

factors. As residential construction

activity slows in Christchurch, we expect it will be picking up in Auckland and

while dairy prices continue to slide, prices of some other commodities are

doing well. The exchange rate is also

significantly lower with the Trade Weighted Exchange Rate Index (TWI) now 15%

below the recent peak in April.

So what does this mean for monetary

policy? While we had acknowledged the

chance of lower interest rates this year we didn’t expect the Reserve Bank of

New Zealand to cut the OCR in June.

Developments since that time have vindicated the Bank’s move. When they cut in June they signaled a further

cut was likely which we know expect to be delivered at the July OCR

review. A further cut in September is now

likely.

From there it gets a bit harder. While the outlook for growth is deteriorating

we expect inflation to be rising over the remainder of this year and into next.

That’s a function of rising petrol prices (which the Bank will look through)

the decline in the exchange rate (which the Bank may look through), but also whether

pricing intentions and prices will remain low in the face of higher capacity

utilisation and the lower currency.

Margins can only be squeezed so much.

We think capacity pressures will remain elevated even as growth slows as

we believe potential growth will be slowing also. Finally, we believe global inflation will be

rising next year.

So the key message for today is the RBNZ was

right to cut in June, more is coming (we think two more 25bp cuts), but caution

is warranted about expecting too much.

--

Posted By Bevan Graham to Economic Insights at 7/07/2015 03:20:00 PM

Reply all

Reply to author

Forward

0 new messages