Dynamic linear regression with constrained coefficients

255 views

Skip to first unread message

Justin Wang

Sep 23, 2015, 6:37:07 AM9/23/15

to stan-...@googlegroups.com

Hi Stan users group

I'm using Stan to estimate a dynamic regression model specified as follows:

All of the error terms are Gaussian (0,σ2) and uncorrelated.

In order to impose the contraints, I'm using the following transformation (time subscript not typed):

I seem to get reasonable posterior means for the betas when put through WinBUGS, but when switched to Stan, the estimated means of betas are completely off. The code compiles and runs fine.

I'm not sure what went wrong, but I suspect it's around the transformation part. Here's my Stan code, I'm assuming k=3. Any insight is appreciated.

I'm using Stan to estimate a dynamic regression model specified as follows:

All of the error terms are Gaussian (0,σ2) and uncorrelated.

In order to impose the contraints, I'm using the following transformation (time subscript not typed):

I seem to get reasonable posterior means for the betas when put through WinBUGS, but when switched to Stan, the estimated means of betas are completely off. The code compiles and runs fine.

I'm not sure what went wrong, but I suspect it's around the transformation part. Here's my Stan code, I'm assuming k=3. Any insight is appreciated.

data {

int<lower=0> N;

vector[N] y;

vector[N] x[3];

}

parameters {

vector[N] phi[3];

vector[N] alpha;

real<lower=0> sigma_phi;

real<lower=0> sigma_y;

real<lower=0> sigma_alpha;

}

transformed parameters {

vector[N] beta[3];

beta[1] <- exp(phi[1])./(exp(phi[1])+exp(phi[2])+exp(phi[3]));

beta[2] <- exp(phi[2])./(exp(phi[1])+exp(phi[2])+exp(phi[3]));

beta[3] <- exp(phi[3])./(exp(phi[1])+exp(phi[2])+exp(phi[3]));

}

model {

sigma_y ~ cauchy(0,5);

sigma_alpha ~ cauchy(0,5);

sigma_phi ~ cauchy(0,5);

for (i in 2:N) {

alpha[i] ~ normal(alpha[i-1],sigma_alpha);

}

for (k in 1:3) {

for (i in 2:N) {

phi[k,i] ~ normal(phi[k,i-1],sigma_phi);

}

}

y ~ normal(alpha + rows_dot_product(x[1],beta[1]) + rows_dot_product(x[2],beta[2]) + rows_dot_product(x[3],beta[3]),sigma_y);

Bob Carpenter

Sep 23, 2015, 5:44:29 PM9/23/15

to stan-...@googlegroups.com

How did the estimates vary?

I couldn't follow the equations because I couldn't tell what

was being multiplied and what was a subscript and what the indexes

were. Do you have the JAGS model you used? Or could you go back

and write something like y[t] so it's clear where the indexes are?

This:

> transformed parameters {

> vector[N] beta[3];

> beta[1] <- exp(phi[1])./(exp(phi[1])+exp(phi[2])+exp(phi[3]));

> beta[2] <- exp(phi[2])./(exp(phi[1])+exp(phi[2])+exp(phi[3]));

> beta[3] <- exp(phi[3])./(exp(phi[1])+exp(phi[2])+exp(phi[3]));

> }

is going to be very inefficient compared to doing this the other

way around:

vector[3] phi[N];

...

simplex[3] beta[N];

for (n in 1:N)

beta[n] <- softmax(phi[n]);

but maybe that'll mess up your later computation, which I don't

quite understand. If you have to do it your way, at least cache those

exp(phi[k]) values for reuse!

Your version is overparameterized --- there are really only two

degrees of freedom in a simplex. This can make it hard to sample.

But that would show up as low effective sample size or non-convergence.

Did you run multiple chains and get convergence?

- Bob

> On Sep 23, 2015, at 6:37 AM, Justin Wang <jwan...@gmail.com> wrote:

>

>

> Hi Stan users group

>

>

>

> I'm using Stan to estimate a dynamic regression model specified as follows:

>

>

>

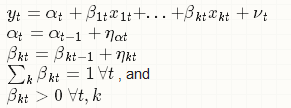

> yt=αt+β1tx1t+...+βktxkt+νt

> αt=αt−1+ηαt

> βkt=βkt−1+ηkt

> ∑kβkt=1 ∀t , and

> βkt>0 ∀t,k

> --

> You received this message because you are subscribed to the Google Groups "Stan users mailing list" group.

> To unsubscribe from this group and stop receiving emails from it, send an email to stan-users+...@googlegroups.com.

> To post to this group, send email to stan-...@googlegroups.com.

> For more options, visit https://groups.google.com/d/optout.

I couldn't follow the equations because I couldn't tell what

was being multiplied and what was a subscript and what the indexes

were. Do you have the JAGS model you used? Or could you go back

and write something like y[t] so it's clear where the indexes are?

This:

> transformed parameters {

> vector[N] beta[3];

> beta[1] <- exp(phi[1])./(exp(phi[1])+exp(phi[2])+exp(phi[3]));

> beta[2] <- exp(phi[2])./(exp(phi[1])+exp(phi[2])+exp(phi[3]));

> beta[3] <- exp(phi[3])./(exp(phi[1])+exp(phi[2])+exp(phi[3]));

> }

way around:

vector[3] phi[N];

...

simplex[3] beta[N];

for (n in 1:N)

beta[n] <- softmax(phi[n]);

but maybe that'll mess up your later computation, which I don't

quite understand. If you have to do it your way, at least cache those

exp(phi[k]) values for reuse!

Your version is overparameterized --- there are really only two

degrees of freedom in a simplex. This can make it hard to sample.

But that would show up as low effective sample size or non-convergence.

Did you run multiple chains and get convergence?

- Bob

> On Sep 23, 2015, at 6:37 AM, Justin Wang <jwan...@gmail.com> wrote:

>

>

> Hi Stan users group

>

>

>

> I'm using Stan to estimate a dynamic regression model specified as follows:

>

>

>

> αt=αt−1+ηαt

> βkt=βkt−1+ηkt

> ∑kβkt=1 ∀t , and

> βkt>0 ∀t,k

>

>

>

> All of the error terms are Gaussian (0,σ2) and uncorrelated.

>

> In order to impose the contraints, I'm using the following transformation (time subscript not typed):

>

>

> βk=exp(ϕk)∑kexp(ϕk)

>

>

> All of the error terms are Gaussian (0,σ2) and uncorrelated.

>

> In order to impose the contraints, I'm using the following transformation (time subscript not typed):

>

>

> You received this message because you are subscribed to the Google Groups "Stan users mailing list" group.

> To unsubscribe from this group and stop receiving emails from it, send an email to stan-users+...@googlegroups.com.

> To post to this group, send email to stan-...@googlegroups.com.

> For more options, visit https://groups.google.com/d/optout.

Message has been deleted

Justin Wang

Sep 24, 2015, 8:33:18 AM9/24/15

to Stan users mailing list

Thank you Bob

I didn't realize that my equations have turned into gibberish. Here's the model I'm trying to estimate

I tried to impose the constraints with the transformation below. As a result, the beta's are now deterministic (i.e. beta[1] <- exp(phi[1])./(exp(phi[1])+exp(phi[2])+exp(phi[3])), and the dynamic of the beta's is driven by Phi (i.e. Phi[k,t] ~ normal(Phi[k,t-1] , nu[k,t])).

Bob Carpenter

Sep 25, 2015, 5:00:00 PM9/25/15

to stan-...@googlegroups.com

As I just wrote into Stackoverflow (it always feels like belt

and suspenders answering questions in two places), the problem

may be a lack of prior on phi[k,1] and the translational/additive

invariance of the softmax transform (your exp transform --- it's a

builtin in Stan).

What happened to the posterior? Did the model converge?

It'd help to see the JAGS model that worked.

- Bob

> On Sep 24, 2015, at 8:33 AM, Justin Wang <jwan...@gmail.com> wrote:

>

> Thank you Bob

>

>

>

> I didn't realize that my equations have turned into gibberish. Here's the model I'm trying to estimate

>

>

>

>

>

>

and suspenders answering questions in two places), the problem

may be a lack of prior on phi[k,1] and the translational/additive

invariance of the softmax transform (your exp transform --- it's a

builtin in Stan).

What happened to the posterior? Did the model converge?

It'd help to see the JAGS model that worked.

- Bob

> On Sep 24, 2015, at 8:33 AM, Justin Wang <jwan...@gmail.com> wrote:

>

> Thank you Bob

>

>

>

> I didn't realize that my equations have turned into gibberish. Here's the model I'm trying to estimate

>

>

>

>

>

>

> I tried to impose the constraints with the transformation below. As a result, the beta's are now deterministic (i.e. beta[1] <- exp(phi[1])./(exp(phi[1])+exp(phi[2])+exp(phi[3])), and the dynamic of the beta's is driven by Phi (i.e. Phi[k,t] ~ normal(Phi[k,t-1] , nu[k,t])).

>

>

>

>

>

>

>

>

>

>

>

>

>

>

Justin Wang

Sep 26, 2015, 5:01:08 AM9/26/15

to Stan users mailing list

Thanks Bob.

I've reworked my Stan code using the softmax function and addressed the identification problem using the example on pages 52-53 of the User's Guide. I haven't tried specifying a prior for phi[k,1] yet. The model doesn't seem to have converged based on Rhat and N_Eff. I've also attached the BUGS code below.

I've reworked my Stan code using the softmax function and addressed the identification problem using the example on pages 52-53 of the User's Guide. I haven't tried specifying a prior for phi[k,1] yet. The model doesn't seem to have converged based on Rhat and N_Eff. I've also attached the BUGS code below.

data {

int<lower=0> N;

vector[N] y;

vector[3] x[N];

}

transformed data {

vector[N] zeros;

zeros <- rep_vector(0,N);

}

parameters {

matrix[N,2] phiraw;

vector[N] alpha;

vector<lower=0>[3] sigma_phi;

real<lower=0> sigma_y;

real<lower=0> sigma_alpha;

}

transformed parameters {

matrix[N,3] phi;

simplex[3] beta[N];

phi <- append_col(phiraw, zeros);

for (i in 1:N)

beta[i] <- softmax(row(phi,i)');

}

model {

sigma_y ~ cauchy(0,5);

sigma_alpha ~ cauchy(0,5);

sigma_phi ~ cauchy(0,5);

for (i in 2:N) {

alpha[i] ~ normal(alpha[i-1],sigma_alpha);

}

for (k in 1:2) {

for (i in 2:N) {

phiraw[i,k] ~ normal(phiraw[i-1,k],sigma_phi[k]);

}

}

for (i in 1:N)

y[i] ~ normal(alpha[i] + x[i]' * beta[i],sigma_y);

}Inference for Stan model: test_model

1 chains: each with iter=(1000); warmup=(0); thin=(1); 1000 iterations saved.

Warmup took (1038) seconds, 17 minutes total

Sampling took (1110) seconds, 18 minutes total

Mean MCSE StdDev 5% 50% 95% N_Eff N_Eff/s R_hat

lp__ 3.5e+003 1.8e+002 3.0e+002 3.0e+003 3.7e+003 3.9e+003 2.6 2.4e-003 2.9e+000

accept_stat__ 2.2e-001 1.6e-001 3.2e-001 6.6e-012 1.4e-002 9.1e-001 4.2 3.8e-003 1.7e+000

stepsize__ 1.5e-003 4.9e-018 3.5e-018 1.5e-003 1.5e-003 1.5e-003 0.50 4.5e-004 1.0e+000

treedepth__ 1.1e+001 1.4e-003 4.5e-002 1.1e+001 1.1e+001 1.1e+001 1000 9.0e-001 1.0e+000

n_leapfrog__ 2.0e+003 1.4e+000 4.6e+001 2.0e+003 2.0e+003 2.0e+003 1000 9.0e-001 1.0e+000

n_divergent__ 0.0e+000 0.0e+000 0.0e+000 0.0e+000 0.0e+000 0.0e+000 1000 9.0e-001-1.$e+000

sigma_phi[1] 2.2e-002 7.0e-003 1.8e-002 1.1e-002 1.4e-002 6.5e-002 6.4 5.7e-003 1.4e+000

sigma_phi[2] 5.5e-001 6.4e-002 1.5e-001 3.8e-001 5.1e-001 8.7e-001 5.2 4.7e-003 1.4e+000

sigma_phi[3] 3.3e+001 1.5e+001 1.3e+002 6.9e-001 6.0e+000 1.3e+002 72 6.5e-002 1.0e+000

sigma_y 4.7e-002 7.0e-004 2.1e-003 4.4e-002 4.7e-002 5.0e-002 8.8 7.9e-003 1.3e+000

sigma_alpha 3.1e-003 8.6e-004 1.7e-003 1.7e-003 2.6e-003 6.8e-003 3.8 3.4e-003 1.7e+000

Here's the equivalent Bugs model, from which I could recover the beta's fairly accurately.

model {

for (i in 1:N) {

y[i]~dnorm(meany[i],tauy)

meany[i]<-alpha[i]+beta1[i]*x[i,1]+beta2[i]*x[i,2]+beta3[i]*x[i,3]

}

for (i in 2:N) {

alpha[i]~dnorm(alpha[i-1],taua)

phi1[i]~dnorm(phi1[i-1],taub1)

phi2[i]~dnorm(phi2[i-1],taub2)

phi3[i]~dnorm(phi3[i-1],taub3)

beta1[i]<-exp(phi1[i])/(exp(phi1[i])+exp(phi2[i])+exp(phi3[i]))

beta2[i]<-exp(phi2[i])/(exp(phi1[i])+exp(phi2[i])+exp(phi3[i]))

beta3[i]<-exp(phi3[i])/(exp(phi1[i])+exp(phi2[i])+exp(phi3[i]))

}

#prior

tauy~dgamma(0.01,0.01)

taua~dgamma(0.01,0.01)

taub1~dgamma(0.01,0.01)

taub2~dgamma(0.01,0.01)

taub3~dgamma(0.01,0.01)

#State at t=1

m<-log(1/3)

alpha[1]~dnorm(0,taua)

phi1[1]~dnorm(m,2)

phi2[1]~dnorm(m,2)

phi3[1]~dnorm(m,2)

beta1[1]<-exp(phi1[1])/(exp(phi1[1])+exp(phi2[1])+exp(phi3[1]))

beta2[1]<-exp(phi2[1])/(exp(phi1[1])+exp(phi2[1])+exp(phi3[1]))

beta3[1]<-exp(phi3[1])/(exp(phi1[1])+exp(phi2[1])+exp(phi3[1]))

Thank you

Justin

Bob Carpenter

Oct 2, 2015, 2:43:36 PM10/2/15

to stan-...@googlegroups.com

Sorry I missed replying to this one earlier.

Have you tried running for more than 1000 iterations? Some models

take a while to warm up properly and it looks like you may just need

more time. This is especially true of models that are not very well

identified. It looks like you're doing the right thing to identify

the softmax component, though, so I'm not sure why this is taking

so long.

Also, we strongly recommend running more than one chain to diagnose

non-convergence.

This:

> for (i in 2:N) {

> phiraw[i,k] ~ normal(phiraw[i-1,k],sigma_phi[k]);

> }

can be vectorized for more efficiency as

phiraw[i] ~ normal(phiraw[i - 1], sigma_phi);

And this

> for (i in 2:N) {

> alpha[i] ~ normal(alpha[i-1],sigma_alpha);

> }

can be vectorized as

tail(alpha, N - 1) ~ normal(head(alpha, N - 1), sigma_alpha);

and this

> for (i in 1:N)

> y[i] ~ normal(alpha[i] + x[i]' * beta[i],sigma_y);

can be vectorized as

y ~ normal(alpha + x * beta, sigma_y);

But you have to declare x as a matrix[N,3]. The data input

format won't change.

- Bob

Have you tried running for more than 1000 iterations? Some models

take a while to warm up properly and it looks like you may just need

more time. This is especially true of models that are not very well

identified. It looks like you're doing the right thing to identify

the softmax component, though, so I'm not sure why this is taking

so long.

Also, we strongly recommend running more than one chain to diagnose

non-convergence.

This:

> for (i in 2:N) {

> phiraw[i,k] ~ normal(phiraw[i-1,k],sigma_phi[k]);

> }

phiraw[i] ~ normal(phiraw[i - 1], sigma_phi);

And this

> for (i in 2:N) {

> alpha[i] ~ normal(alpha[i-1],sigma_alpha);

> }

tail(alpha, N - 1) ~ normal(head(alpha, N - 1), sigma_alpha);

and this

> for (i in 1:N)

> y[i] ~ normal(alpha[i] + x[i]' * beta[i],sigma_y);

y ~ normal(alpha + x * beta, sigma_y);

But you have to declare x as a matrix[N,3]. The data input

format won't change.

- Bob

Reply all

Reply to author

Forward

0 new messages