gamma_log encountering negative inverse scale parameter

445 views

Skip to first unread message

rcdr...@gmail.com

Feb 4, 2016, 10:35:46 AM2/4/16

to Stan users mailing list

Hi,

I'm having some problems with a model I'm trying to run.

I have a series of values I'm trying to estimate and am fitting them as a random walk.

So in the parameters section I have:

parameters {

...

real exp_subclinical[n_years];

...

}where n_years is an integer passed in as data, and in the model section:

model {

exp_subclinical[1] ~ uniform(1,upper_lambda1);

for( oy in 2:n_years ){

exp_subclinical[oy] ~ gamma(exp_subc_k, exp_subc_k/exp_subclinical[oy-1]);

}

...

}where exp_subc_k is a positive number provided as part of the data.

When I am running the model I get Metropolis proposals rejected because of:

Exception thrown at line 104: stan::math::gamma_log: Inverse scale parameter is -61.6392, but must be > 0!Line 104 is the line within the for loop with the gamma sampling statement, and there can be quite a lot of these messages.

I don't understand how the inverse scale parameter can become negative, being the division of a positive value by a value which is either from a uniform(1,some positive value I supplied) or a gamma distribution.

I did not observe this when I initially ran the problem for few iterations with unrealistic initial values (all exp_subclinical were 1000) but did when running for many iterations - the values of exp-subclinical decline from 1:n_years so providing more realistic initial values lets me see the problem at lower numbers of iterations and would indicate that it is related to low exp_subclinical values.

I have tried this with cmdstan and rstan with the same outcome.

Why would this be happening?

Thanks.

Jonah Gabry

Feb 4, 2016, 11:03:00 AM2/4/16

to Stan users mailing list

One issue is that parameters with constraints need to be declared with those constraints in the parameters block or you can get invalid proposals. So if a parameter has to be positive it should be declared with <lower=0>, if it's a probability it needs to be declared with <lower=0, upper=1>, etc. So using a constrained uniform distribution on a parameter declared without those constraints is a problem. Does that parameter actually have a logical lower bound of 1? If you just think it's unlikely for it to be less than 1 than I would use a prior that places low probability mass in (0,1) but without impose a lower bound of 1 unless it's a logical requirement.

Jonah

Ron

Feb 4, 2016, 11:44:39 AM2/4/16

to Stan users mailing list

Hi Jonah,

On Thursday, February 4, 2016 at 4:03:00 PM UTC, Jonah Gabry wrote:

One issue is that parameters with constraints need to be declared with those constraints in the parameters block or you can get invalid proposals. So if a parameter has to be positive it should be declared with <lower=0>, if it's a probability it needs to be declared with <lower=0, upper=1>, etc. So using a constrained uniform distribution on a parameter declared without those constraints is a problem. Does that parameter actually have a logical lower bound of 1? If you just think it's unlikely for it to be less than 1 than I would use a prior that places low probability mass in (0,1) but without impose a lower bound of 1 unless it's a logical requirement.Jonah

Thanks, I'll explicitly include the constraints in the parameter block and try again.

The constraint on the first value could be placed at zero, since the upper bound is high (1000s) the probability would be very small.

If I made the prior on the first value something like ~ gamma(x,1) with x half way along my previous uniform range that might be better too.

Jonah Gabry

Feb 4, 2016, 12:31:28 PM2/4/16

to Stan users mailing list

Hi Ron,

I hope that works better, but I also wanted to take your example as an opportunity to point out a common (though totally understandable) misconception about Stan. You say

I don't understand how the inverse scale parameter can become negative, being the division of a positive value by a value which is either from a uniform(1,some positive value I supplied) or a gamma distribution.

I added the emphasis because it's not actually true that this value will be from a uniform or gamma. In terms of how the model is written it might seem like that would be true, but Stan isn't actually drawing values from those distributions. Taking the gamma as an example, when you do something like

theta ~ gamma(a, b)Stan does not draw a value for theta from a gamma(a,b) distribution. The value of theta comes from the state of the Markov chain. Taking that value for theta, Stan computes (up to a constant) the value log(gamma(theta | a, b)), i.e. the value of the

gamma(a,b) distribution evaluated at theta. The following are equivalent (up to a normalizing constant)

theta ~ gamma(a, b)

increment_log_prob(gamma_log(theta, a, b))So while it's true that this is equivalent (for Stan) as placing a gamma(a,b) prior on theta, it does not actually mean that theta is being sampled from a gamma distribution. The only place in a Stan program where that explicitly happens is in generated quantities, where you could do something like

x <- gamma_rng(a,b)

Bob Carpenter

Feb 4, 2016, 2:30:52 PM2/4/16

to stan-...@googlegroups.com

We only recommend uppper/lower bound constraints where necessary,

not as a kind of hard prior knowledge. The main reason is that

if there's any probability mass around the boundary it'll be

problematic both computationally and statistically, wheras there's

no downside for not including a hard constraint.

- Bob

> --

> You received this message because you are subscribed to the Google Groups "Stan users mailing list" group.

> To unsubscribe from this group and stop receiving emails from it, send an email to stan-users+...@googlegroups.com.

> To post to this group, send email to stan-...@googlegroups.com.

> For more options, visit https://groups.google.com/d/optout.

not as a kind of hard prior knowledge. The main reason is that

if there's any probability mass around the boundary it'll be

problematic both computationally and statistically, wheras there's

no downside for not including a hard constraint.

- Bob

> You received this message because you are subscribed to the Google Groups "Stan users mailing list" group.

> To unsubscribe from this group and stop receiving emails from it, send an email to stan-users+...@googlegroups.com.

> To post to this group, send email to stan-...@googlegroups.com.

> For more options, visit https://groups.google.com/d/optout.

Andrew Gelman

Feb 4, 2016, 8:46:45 PM2/4/16

to stan-...@googlegroups.com

This reminds me . . . have we considered removing the uniform distribution entirely from Stan? It seems like the _only_ use for it is either completely redundant or else wrong (e.g., a variable is defined as unconstrained but then the user gives a uniform with fixed bounds).

Jonah Sol Gabry

Feb 4, 2016, 8:58:29 PM2/4/16

to stan-...@googlegroups.com

On Thu, Feb 4, 2016 at 8:46 PM, Andrew Gelman <gel...@stat.columbia.edu> wrote:

This reminds me . . . have we considered removing the uniform distribution entirely from Stan? It seems like the _only_ use for it is either completely redundant or else wrong (e.g., a variable is defined as unconstrained but then the user gives a uniform with fixed bounds).

I have yet to see an example where calling uniform() is useful. If it's not already implied by the constraints then something hasn't been declared properly.

That said, I think some people like calling uniform() because when reading a Stan program it can be nice to see every unknown explicitly get a prior.

Andrew Gelman

Feb 4, 2016, 9:02:48 PM2/4/16

to stan-...@googlegroups.com

That’s another reason not to do it, then!

Bob Carpenter

Feb 5, 2016, 2:04:03 AM2/5/16

to stan-...@googlegroups.com

The only use I see for the pdf is normalization.

But we need the PRNG, and maybe the CDFs.

If we did get rid of the uniform distribution, we'd

probably want to flag it as missing on purpose in the

parser.

- Bob

But we need the PRNG, and maybe the CDFs.

If we did get rid of the uniform distribution, we'd

probably want to flag it as missing on purpose in the

parser.

- Bob

Andrew Gelman

Feb 5, 2016, 2:07:44 AM2/5/16

to stan-...@googlegroups.com

Yes, or alternatively we could have the parser spit out a warning if there’s a uniform and say don’t do it. But that would just confuse people more…

Ron

Feb 5, 2016, 3:39:04 AM2/5/16

to Stan users mailing list, gel...@stat.columbia.edu

Thanks for the clarification, Jonah.

And thanks for the discussion on the use of uniform, I'm going to try to avoid the temptation to use it from now on.

My model is running much better now with constraints declared explicitly in the parameter section and using a gamma prior instead of a uniform. Now to see if I can make any speed improvements.

Guido Biele

Feb 5, 2016, 6:04:41 AM2/5/16

to Stan users mailing list

about the usefulness of the uniform:

for me it was very useful when I had difficulties using the Cauchy distribution,

which, as the stan reference explains can be difficult to sample from because

different step sizes are optimal dependent on if one is in the tails or not.

as recommended in the stan reference I then re-parameterized

chauchy(location, scale)

to

location + scale * tan(uniform(0,pi()/2))

which worked much better.

so please keep the uniform!!

cheers - guido

Michael Betancourt

Feb 5, 2016, 11:23:56 AM2/5/16

to stan-...@googlegroups.com

Guido,

The point is that such a transformation could be implemented as

parameters {

real<lower=0, upper=0.5 * pi()> alpha_tilde;

…

}

model {

…

alpha <- location + scale * alpha_tilde;

…

}

No uniform is necessary once alpha_tilde is properly constrained.

Bob Carpenter

Feb 5, 2016, 11:47:04 AM2/5/16

to stan-...@googlegroups.com

Not just "could", but "should". The uniform by itself isn't

enough --- you need the constraint. But when you have the constraint,

you don't need the uniform (other than to normalize).

- Bob

enough --- you need the constraint. But when you have the constraint,

you don't need the uniform (other than to normalize).

- Bob

Guido Biele

Feb 5, 2016, 11:53:16 AM2/5/16

to stan-...@googlegroups.com

OK,

I had constrained alpha_tilde as you write,

and now I also remember that the manual

stated that the statement

alpha_tilde ~uniform(0,pi()/2)

is not necessary if alpha_tilde was

properly constrained.

You received this message because you are subscribed to a topic in the Google Groups "Stan users mailing list" group.

To unsubscribe from this topic, visit https://groups.google.com/d/topic/stan-users/AqBZT2h5Jyw/unsubscribe.

To unsubscribe from this group and all its topics, send an email to stan-users+...@googlegroups.com.

Guido Biele

Feb 5, 2016, 12:24:28 PM2/5/16

to stan-...@googlegroups.com

Let me continue this wit a question about that I could

use instead of the uniform in a specific case:

I am estimating a multilevel model with group-specific

over-dispersion parameter "phi" for the negative binomial.

at the moment I am doing the following:

parameters {

...

real<lower=0, upper=50> alpha_phi;

real<lower=0, upper=50> beta_phi;

real<lower=0> phi[M];

...

}

model {

...

phi ~ gamma(alpha_phi, beta_phi);

...

}

(I started with a Cauchy as a priors for the over dispersion,

but then switched to the gamma, which Kruschke uses as a

hierarchical prior for error variance in his book).

I tried to avoid using the uniform priors (even though

the model converges just fine) by putting priors gamma-priors

on the mean and variance of the gamma and then transform

mean and variance to phi_alpha and phi_beta in the transformed

parameters block:

parameters {

...

real<lower=0> phi_mu;

real<lower=0> phi_sigma;

real<lower=0> phi[M];

...

}

transformed parameters {

...

real phi_alpha;

real phi_beta;

phi_alpha <- phi_mu^2/phi_sigma^2;

phi_beta <- phi_mu/phi_sigma^2;

...

}

model {

...

phi_mu ~ gamma(8,6);

phi_sigma ~ gamma(8,6);

phi ~ gamma(phi_alpha , phi_beta );

...

}

but here my problem was that I "data peaked" to get an

idea about the priors for phi_mu and phi_sigma, and that

this did not converge nearly as well as directly

using uniform priors.

What would you recommend to model hierarchical error

variances/over dispersion?

Guido

Taking the risk to one again expose my ignorance :-)

I understand that the log probability is incremented

when one uses "~" or increment_log_prob. I guess log_prob

is also incremented when puts constraints on a parameter

and does not use uniform(), i.e. log_prob would in this case

be incremented without a "~" or an increment_log_prob statement?

Bob Carpenter

Feb 5, 2016, 12:56:05 PM2/5/16

to stan-...@googlegroups.com

[changed subject]

Every constrained variable contributes a Jacobian term

to the log density --- they're all defined in a chapter of

the manual. The uniform is a scaled and translated inverse

logit. That's because Stan's densities are expressed on

the unconstrained scale.

I think part of the issue for hierarchical variances is how

plausible values near zero are (i.e., complete pooling).

Andrew discusses behavior around zero in his papers (cited

in the manual).

What we need is an update here:

https://github.com/stan-dev/stan/wiki/Prior-Choice-Recommendations

- Bob

P.S. That's "peeked", not "peaked"! You want to do sensitivity

analysis whatever you do on these priors and make sure you're

not adding in too much prior information (where "too much" is

of course dependent on your prior knowledge!).

Every constrained variable contributes a Jacobian term

to the log density --- they're all defined in a chapter of

the manual. The uniform is a scaled and translated inverse

logit. That's because Stan's densities are expressed on

the unconstrained scale.

I think part of the issue for hierarchical variances is how

plausible values near zero are (i.e., complete pooling).

Andrew discusses behavior around zero in his papers (cited

in the manual).

What we need is an update here:

https://github.com/stan-dev/stan/wiki/Prior-Choice-Recommendations

- Bob

P.S. That's "peeked", not "peaked"! You want to do sensitivity

analysis whatever you do on these priors and make sure you're

not adding in too much prior information (where "too much" is

of course dependent on your prior knowledge!).

Jonah Sol Gabry

Feb 5, 2016, 2:56:05 PM2/5/16

to stan-...@googlegroups.com

On Friday, February 5, 2016, Guido Biele <guido...@gmail.com> wrote:

about the usefulness of the uniform:for me it was very useful when I had difficulties using the Cauchy distribution,which, as the stan reference explains can be difficult to sample from becausedifferent step sizes are optimal dependent on if one is in the tails or not.as recommended in the stan reference I then re-parameterizedchauchy(location, scale)tolocation + scale * tan(uniform(0,pi()/2))which worked much better.so please keep the uniform!!

As others have pointed out you don't actually need to call uniform() to do this. Although even if you did you could get around it by going a different route and inverse-cdf-ing a standard normal.

Ben Goodrich

Feb 5, 2016, 3:00:36 PM2/5/16

to Stan users mailing list

To clarify, Jonah meant inverse-cdf-ing the CDF of a parameter whose prior is standard normal.

Ben

Andrew Gelman

Feb 5, 2016, 4:15:51 PM2/5/16

to stan-...@googlegroups.com

Yes, exactly. You should not do the uniform unless you have the corresponding constraint on the parameter. And, if you have the constraint, the uniform adds nothing. Hence, the uniform can only cause trouble.

On Feb 5, 2016, at 11:23 AM, Michael Betancourt <betan...@gmail.com> wrote:

Andrew Gelman

Feb 5, 2016, 4:29:14 PM2/5/16

to stan-...@googlegroups.com

On a more practical point, if you were planning to do a uniform(0,50) prior, you could instead do a half-normal(0,50), i.e., constrain the parameter to be greater than 0, and then give a normal(0,50) prior. But I really don’t like priors with a scale of 50. I like models to be scale free so that parameters should rarely be much more than 1 in absolute value, in which case we can use normal(0,1) priors or, if you want to be really weak, normal(0,5).

Jonah Sol Gabry

Feb 5, 2016, 6:14:08 PM2/5/16

to stan-...@googlegroups.com

On Fri, Feb 5, 2016 at 3:00 PM, Ben Goodrich <goodri...@gmail.com> wrote:

To clarify, Jonah meant inverse-cdf-ing the CDF of a parameter whose prior is standard normal.

Ben

Yes, thanks for clarifying. That is indeed what I meant.

Guido Biele

Feb 24, 2016, 8:00:43 AM2/24/16

to Stan users mailing list

Thanks everyone for chiming in!

About Andrews advocacy for scale free models:

I try to follow this recommendation when possible.

However, for the data I am working with I need

to use the negative binomial distribution, and here

the over dispersion parameter can take larger values

that are maybe not best modeled with normal(0,1) or

chauchy(0,1) as priors

About my attempts to find suitable priors for hierarchical

modeling of the overdispersion parameter (i.e. the phi of

neg_binomial_2):

I chose to model the hierarchical prior phi with the gamma

distribution, because it has to be larger than zero.

I could also have tried the chauchy, but it appeared more

natural for me to choose the gamma for a _hierarchical_ prior

whose mean I expect to be larger than zero.

Modeling the gamma directly with shape and inverse scale

parameters alpha and beta did not work well. Instead I used

priors for the mean and sd of the gamma distribution

and transformed them to alpha and beta.

Using the cauchy as a prior for the mean of the gamma works

well. Finding a good prior for the sd of the gamma seems

harder. I get the same posteriors for the variance of the

gamma independent if I use a cauchy or uniform prior, but

n_eff is generally low (around 50-80 effective samples from 3

chains with 400 samples each). The low n_eff seems mainly

to be caused by relatively high auto-correlation of the sd

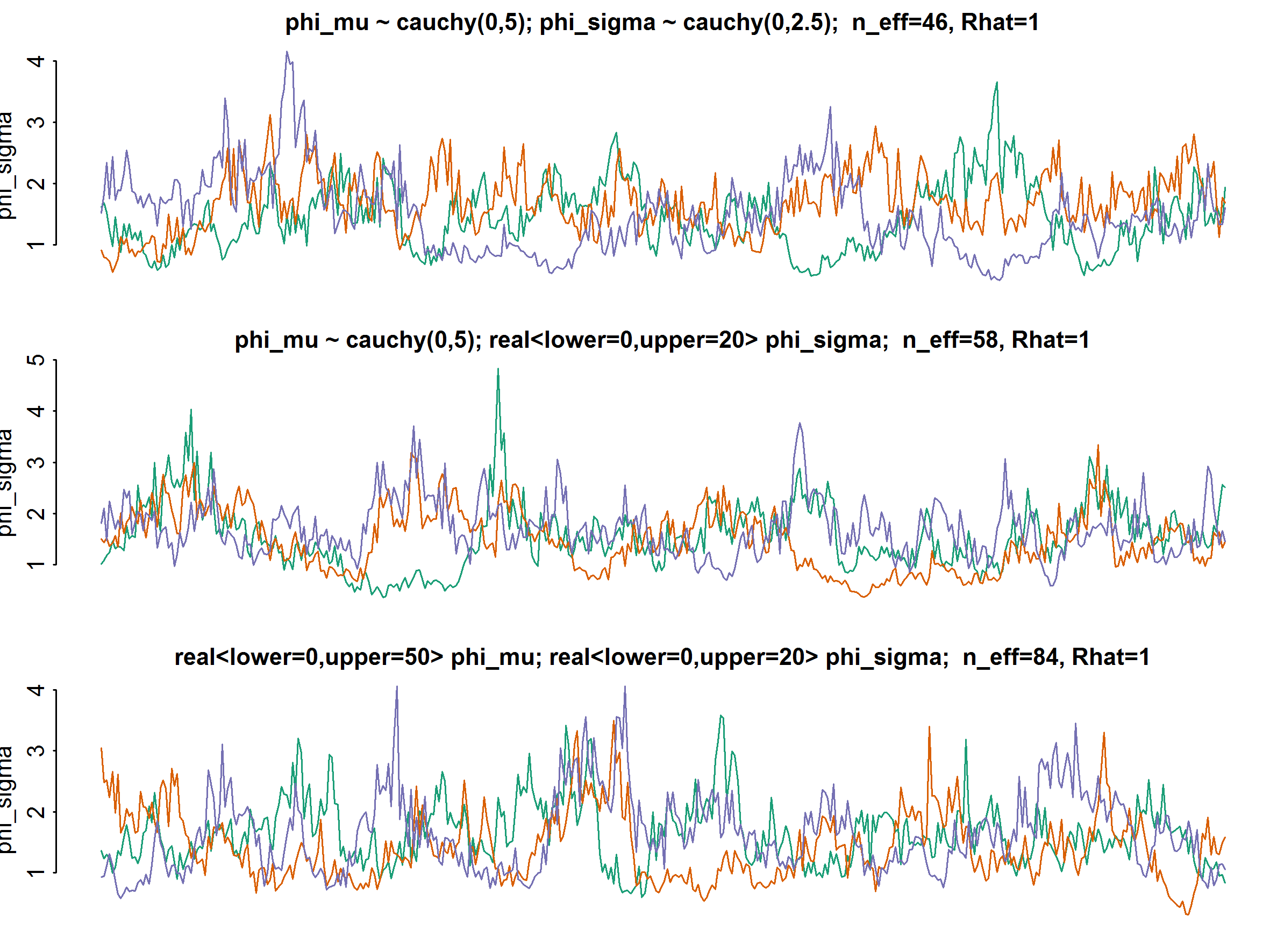

of the gamma distribution (see attachments). I'd welcome

any suggestion to reduce this auto-correlation (of course

i can always run the chain longer).

here are the relevant snippets of how i am currently modeling

hierarchical priors for phi:

parameters {

...

// overdispersion of negative binomial

real<lower=0, upper=pi()/2> phi_mu_unif;

real<lower=0, upper=pi()/2> phi_sigma_unif;

real<lower=0> phi[M]; // M = number of groups

}

transformed parameters {

...

phi_mu <- 5 * tan(phi_mu_unif);

phi_sigma <- 2.5 * tan(phi_sigma_unif);

}

model {

...

phi ~ gamma(phi_mu^2/phi_sigma^2, phi_mu/phi_sigma^2);

// could also calculate alpha and beta in the transformed parameters block ...

...

}

Some more observations:

It looks as if I can stick to the default adapt_delta when using

uniform priors for the variance of the gamma, whereas I have

to increase adapt_delta when using cauchy priors in order to avoid

divergent iterations (I only tried .95, which worked)

I find the re-parameterization of the cauchy described in the manual

very useful.This seems especially useful for the prior scale tau of

the hierarchical regression model. Maybe it would be useful for

other users to include a version of the model on page 75 of the

manual (version 2.9.0) into the manual that also uses a

re-parameterization for the prior scale tau.

Cheers - Guido

{kind=link}

Bob Carpenter

Feb 24, 2016, 6:06:59 PM2/24/16

to stan-...@googlegroups.com

> On Feb 24, 2016, at 8:00 AM, Guido Biele <guido...@gmail.com> wrote:

>

> ...

> I find the re-parameterization of the cauchy described in the manual

> very useful.This seems especially useful for the prior scale tau of

> the hierarchical regression model. Maybe it would be useful for

> other users to include a version of the model on page 75 of the

> manual (version 2.9.0) into the manual that also uses a

> re-parameterization for the prior scale tau.

as well as the code.

And thanks much for the detailed report.

- Bob

Guido Biele

Feb 26, 2016, 6:36:10 AM2/26/16

to stan-...@googlegroups.com

--

You received this message because you are subscribed to a topic in the Google Groups "Stan users mailing list" group.

To unsubscribe from this topic, visit https://groups.google.com/d/topic/stan-users/AqBZT2h5Jyw/unsubscribe.

To unsubscribe from this group and all its topics, send an email to stan-users+...@googlegroups.com.

Bob Carpenter

Feb 26, 2016, 3:40:56 PM2/26/16

to stan-...@googlegroups.com

Awesome. Thanks. I'll try to review it in the next

few days --- I'm a bit backed up right now.

- Bob

few days --- I'm a bit backed up right now.

- Bob

> You received this message because you are subscribed to the Google Groups "Stan users mailing list" group.

> To unsubscribe from this group and stop receiving emails from it, send an email to stan-users+...@googlegroups.com.

Reply all

Reply to author

Forward

0 new messages