Humanity’s Demographic Future

Levan Ramishvili

If you are younger than fifty, you will probably witness in three or four decades something that no human being has seen in the last 60,000 years: a prolonged decline in the human population. The decline will not be caused by an epidemic or climate change, but rather by the collapse of fertility around the world.

To glimpse humanity’s demographic future, one can look to South Korea. In 1960, 1,080,535 South Koreans were born. At the time, South Korea had a population of 25,012,374. In 2020, however, South Korea recorded only 272,410 births in a country of 51,829,023 people.

In other words, South Korea’s birthrate fell from 43.2 per 1,000 in 1960 to 5.3 per 1,000 in 2020. In sixty years, the birthrate in the Republic of Korea collapsed by 88 percent.

![Picture1[1].png](https://groups.google.com/group/respublica-literaria/attach/bfd202620830e/Picture1%5B1%5D.png?part=0.1&view=1)

South Korea’s numbers cannot be dismissed as a product of COVID-19. The pandemic only became a major problem for Korea at the end of February 2020. Because human gestation lasts about 40 weeks, all births before the beginning of December 2020 could not have been influenced by the outbreak of COVID-19. The true effects of COVID-19 on the birth rate, whatever they may be, will not become visible until 2021 concludes.

The Republic of Korea also had very restrictive abortion laws before 2021, and there is no indication that women had more illegal abortions in 2020 than in previous years. 2020’s birth numbers are consistent with South Korea’s long-term decline in the birthrate.

What’s in Store for South Korea?

To understand the future of South Korea’s demography, I like to apply the “Rule of 85.” This rule is based on the fact that life expectancy in most advanced countries is approximately 85 years. If 1,000 people are born each year in country A, and this number is constant, the country’s population in the long-term will be 85 times 1,000 (85 years of average life per 1,000 new people per year). Now, let’s apply the “Rule of 85” to South Korea: 85 times 272,410 (the number of births in 2020) = 23,154,850.

The “Rule of 85” is a rough but useful approximation. It overestimates the population when the fertility rate (the average number of children per woman) is less than 2.1, the approximate fertility-replacement rate (this number accounts for infant mortality). Because more boys are born than girls (the natural ratio, without sex-selective abortions, is about 105 boys per 100 girls), out of the 1,000 births only 485 will be girls. When these girls grow up, if they have fewer than 2.1 children on average, they will be mothers of fewer than 1,000 people. Therefore, in the long term, the population will be less than 85,000 people. On the other hand, the “Rule of 85” underestimates the population in the long term when the fertility rate is greater than 2.1.

In the case of South Korea, 2020’s fertility rate was 0.84, far below the replacement rate. Therefore, in a few decades, the population of South Korea (ignoring immigration, natural disasters, etc.) will be far fewer than our prediction of 23 million. At the current birthrate, the number will be closer to 12 million.

I like using South Korea as an example for many reasons. The first is because, when I use the United States, China, or other countries as an example of declining fertility, readers tend to react with ideological prejudgments (“it’s the president’s fault!”). Or readers get bogged down by issues that, when closely examined, are not as important for fertility as they might seem (youth unemployment in Europe, the legacy of China’s one-child policy, etc.). Most westerners have a superficial understanding of South Korean politics and culture (Do you know the name of South Korea’s president? Is the ruling party left- or right-wing?), making it a perfect country to explain what is happening demographically.

The second reason is that South Korea, although somewhat extreme, is representative of what is happening in many other countries. When we discuss birthrates, the country that tends to spring to mind is, of course, China. In 1990, ten years after the introduction of the one-child policy, China recorded 23,910,000 births (meaning a crude birthrate of 21.06 per 1,000). In 2020, with all birth restrictions removed, 12,050,000 people were born (a crude birthrate of 8.54 per 1,000).

The Chinese authorities tell us that some 10,010,000 people died in 2020 (likely an underestimation, but let’s work with it). The data give us a natural population growth of 2 million, a number that might seem massive if it weren’t for the fact that China’s total population is 1.4 billion people. Again, using my “Rule of 85” we determine that, with the number of births, in a few decades, China’s population would decrease by 27 percent, falling to 1.02 billion. In fact, since China’s birthrate is 1.3 per woman, China’s population could drop to around 700 million.

The Two Asian Giants

The other great Asian giant, India, has a higher birthrate than China does, with some 27 million births in 2019 and a fertility rate right around the replacement rate. The “Rule of 85” estimates, in this case, that the population of India in the long term will be around 2.2 billion people. With current figures, the long-term population of India (2.2 billion) is predicted to be more than three times greater than China’s (700 million). That would entail a monumental geostrategic change.

In this case, the “Rule of 85” estimate is likely inflated, as India has a lower life expectancy. Personally, I predict that India will also experience a major drop in births in the next ten years. Already, Indian states with social policies that prioritize education and women’s rights, such as Kerala, have had fertility rates significantly below 2.1 for many years. Experience shows that undeveloped regions tend to adopt their more developed counterparts’ birthrates. Take Turkey as an example: during the 1980s and 1990s, fertility declined only in Istanbul and the westernmost provinces. But in 2020, Turkey’s eastern provinces followed suit—resulting in a nationwide birth rate of 1.76.

The story is the same in the Americas. Latin America and the Caribbean as a whole already have fertility rates below 2.1. Under their current trends, the populations of Argentina, Chile, and Brazil may begin to shrink in about ten years. Mexico and Colombia will suffer the same fate in about twenty years. In North America (the United States, Canada, and Bermuda) the situation is even more dire, with a weighted average fertility rate of 1.68, well below replacement.

![Picture3-860x455[1].png](https://groups.google.com/group/respublica-literaria/attach/bfd202620830e/Picture3-860x455%5B1%5D.png?part=0.2&view=1)

There appears to be a great exception to this worldwide trend of decreasing fertility: Africa. Yet even there, as the standard of living and wages rise, the birthrate decreases. Morocco and Tunisia already have a fertility rate around 2.1. Demographic changes are beginning to emerge in sub-Saharan countries, too. Cape Verde, for example, is a small country, but it has already crossed the 2.1 threshold. Many others will follow in a few years.

However, even if Africa maintains a high birth rate for several decades, it will not be enough to change the global aggregate effect of reduced births. The world fertility rate in 2019 was, according to the World Bank, 2.403. My prediction, based on recent research, is that the global fertility rate will hit the key threshold of 2.1 around 2030. This means that the world population would reach its peak between 2050 and 2060, then start decreasing from that moment on.

Is Population Decline Inevitable?

My predictions are not set in stone. There are many things that even the most sophisticated mathematical operations cannot predict or measure. The composition of the world’s population may change dramatically in the coming decades.

Fifty years ago, there were no major differences in birthrates between Americans who reported attending a religious service at least once a week (the “religious”) and those who did not (the “secular”). Today, those differences are much more pronounced. While the fertility of both groups has fallen, the “secular” birthrate fell from around 2.8 to 1.5, whereas the “religious” fell from 3 to 2.2. Even more surprisingly, the “religious,” on average, earn less income than their secular counterparts.

Real-world evidence of the religious–secular gap in births is plentiful. Go to any traditional Catholic parish and you’ll see legions of young children bursting out of Ford Transit Minivans. A park in a Hasidic neighborhood teems with playing children, but a park in Greenwich Village will only feature thirty-year-olds doing yoga.

In Israel, the high fertility rate of the Arab and Ultra-Orthodox Jewish population has generated changes in the country’s political and budgetary makeup. In India, part of the reason fertility has fallen more slowly is because of the Muslim population’s higher birthrates. Consequently, India’s Muslim population grew from 10 percent in 1947 to 15 percent today.

The second reason my prediction might not come true is that governments are already reacting to this drop in fertility. Many European countries have already begun implementing programs meant to raise fertility rates. In some cases, such as the Czech Republic, there is some evidence that an increase in birth rate was the result of government policies. In 2020, the Czech fertility rate was 1.71, compared to 1.132 in 1999.

The Chinese government, in its typical heavy-handed fashion, has also implemented several policies intended to raise birthrates. So far, the Chinese Communist Party has implemented policies meant to reduce the cost of education, encouraged couples to have more children, “invited” film and television industries to promote traditional family values, and dramatically restricted abortion on demand.

The third unknown factor about my prediction is mortality. As mentioned before, the population of a country depends on its number of births and life expectancy. In the coming years, will life expectancy increase? Will it decrease? Nobody knows. There are signs that life expectancy plateaued in Europe’s richest countries around 2014, well before the outbreak of COVID-19. This plateau could possibly be attributed to a lack of life-extending medical innovations: for example, new cancer treatments help patients’ quality of life, but they offer very little in terms of life expectancy.

Perhaps life-expectancy-boosting innovations have been canceled out because of an increase in life-expectancy-reducing habits (e.g., drug abuse, living alone, depression, etc.). Will, as one of Moderna’s founders claimed in a recent meeting, mRNA technology bring about a medical revolution in dozens of diseases? I can’t say. Public health is not my area of expertise.

Finally, country by country, an additional demographic factor is at play: emigration. Even though deaths outnumbered births, in 2020 the population of South Korea continued to grow because of immigration. With regard to immigration, one must remember that the planet has net zero immigration (for now at least!)—migrants must leave one country to arrive at another. After all, my prediction is about global population decline.

I can’t think of a country that could draw a migratory flood sufficient to halt its falling population. Before I calculated that, at the current rate, South Korea’s population will fall from 53 million to 12 million in a few decades. If South Korea wants to maintain its population, it will have to bring in 39 million foreigners (largely from non-Asian countries—their immediate neighbors’ populations aren’t faring well either). If South Korea manages to attract mass migration, native Koreans would compose only 25 percent of its population. Ask yourself: do you think that Korean voters will agree to become a minority in their own country? Note that I do not judge these decisions as either positive or negative: Koreans must decide their destiny, not I. But it’s difficult to imagine that such a profound demographic change would be widely accepted.

In closing, I hope that I have convinced you that the world’s demographic future is, to put it lightly, unusual. Not only is fertility declining, it is collapsing faster than I would have predicted ten years ago. I never imagined that Thailand would have a negative natural growth rate in 2021, or that Saudi Arabia’s fertility rate would fall below the replacement level. Although a full analysis of this phenomenon is beyond the scope of this article, one thing is clear: the political, social, and economic consequences of such a demographic collapse will be tremendous.

Levan Ramishvili

In my last article, I outlined the unusual demographic future of humanity: it is highly probable that, between 2050 and 2060 our species will reach a population peak close to 9.5 billion, which will then begin to fall. I also pointed out some of the mechanisms that could make this prediction incorrect, such as a rise in average life expectancy, changes in the relative proportions of social groups, government policies, etc. As it happens, China has just announced new and very restrictive regulations on abortion, the purpose of which is to increase fertility.

Still, let us assume that the future approximately resembles the demographic trends we observe from our vantage point in 2021. It is worth spending some time thinking about the consequences of this population change. As is almost always the case, there will be positive and negative consequences, and which of these predominate will depend, in part, on our ability to design policies that manage the transition well.

In this essay, I will focus on the most direct economic consequences. In the third and last essay of this series (coming out in a few weeks), I will review the social consequences of this demographic shift on the structure of the family, and on the distribution of the population in terms of both land and housing.

Positive Consequences of Population Decline

The main positive consequence that comes to mind is less pressure on natural resources. A smaller or slower-growing population makes it easier to decarbonize the global economy and conserve areas of biological wealth, keeping them from being affected by human activity. This consequence reinforces another key transformation of the global economy: the gross domestic product of advanced economies is becoming progressively “weightless,” and therefore requires fewer natural resources to generate.

Let’s think about a simple example. I currently have 1,833 books on my Kindle. Each shelf in my office can hold, on average, about forty books (some bigger, some smaller). In other words, I would need about forty-six shelves to store the books on my Kindle in physical format. That would take up my entire office and a good part of another one. Since I started reading and buying books as a child, until 2010 when I switched to e-books, I progressively accumulated “weight” in paper. From 2010 until today, my paper “weight” first stabilized and then later began to fall. In 2020, I bought only fourteen paper books, but I gave away more than fourteen of the books I already had. There were many books that I had repurchased in electronic version to have them always at hand, so I gave the physical copies to my students. In other words, my book collection, being much larger on January 1, 2021 than it was on January 1, 2020, still “weighed” much less. This observation applies to almost all my possessions: I can’t even remember the last time I bought a CD or a DVD. All my possessions together “weigh” less today than they did five years ago.

Modern economic growth does not, in general, use more resources per capita. We get better and better at recombining ideas in incredibly creative ways to generate much more added value. That’s why the UK was able to emit less carbon dioxide in 2019 (before the pandemic) than it did in 1890, despite having a gross domestic product, in real value, thirteen times larger. For its part, the United States consumed 2 percent less oil in 2019 than in 1978, while its gross domestic product was, in real value, three times larger (and the United States has not been overly concerned with saving energy).

The weakness of the above argument is that it focuses on more advanced economies. Less developed economies still need more resources to grow and reach the level of wealth of the leading countries. But as these economies stabilize in total size, as a result of population decline, even higher per capita resource use will be compatible with stable or declining global resource consumption.

The Negative Consequences

The negative consequences of the fall in world population are more complex. Most importantly, we must get used to the fact that gross domestic product is growing at lower rates, and we must adapt our societies accordingly. Historically, labor productivity has grown by an average of 2 percent per year. If the working population increases at 1 percent per year (as it did during the 1960s in many advanced economies), in a normal business cycle, the economy will grow by 3 percent (2 percent productivity plus 1 percent population). When the economy accelerates above the normal situation (due to demand or supply shocks), it grows at 4 percent or 5 percent. When it slows down, it grows at 1 or 2 percent. Overall, though, it is always fluctuating somewhere around the 3 percent mark.

Now, let’s imagine a situation where the working population falls at 1 percent per year instead of growing at that rate. If labor productivity continues to grow at 2 percent—I’ll come back to this in a moment—the economy will grow on average by 1 percent (2 percent productivity minus 1 percent population decline), not at 3 percent, as it did before. When the economy accelerates above average, it will grow at 2 or 3 percent. When the economy slows, growth will be at -1 or 0 percent.

This is exactly what has happened to Japan. From the outside, its economy has looked stagnant since the mid-1990s. But if we look at it in terms of its gross domestic product divided by working-age adults (ages sixteen to sixty-five), a measure of the economy’s potential workers regardless of whether they are employed or not, Japan has grown at about the same rate as the United States and faster than Germany. The rivers of ink written about the origins of Japan’s “economic ills” over the past few decades are basically useless. It’s not the fault of the Bank of Japan, or China, or anyone else. Japan is growing at the speed one would expect given its demographic changes.

You might be asking: what does it matter that the economy is growing at 1 percent instead of 3 percent in total terms, if in terms of working-age adults we continue to grow at the same rate? Shouldn’t we be concerned about per capita income instead of total income? Yes and no. Yes, because the relevant measure of income to assess the welfare of a society is per capita, but no, because per capita income is not everything. The ability to pay our public debt, for example, depends on total income, not per capita income.

Imagine a country with a public debt to gross domestic product ratio of 100 percent. If that country’s economy grows at 3 percent, public debt stabilizes as a percentage of gross domestic product. If the general government deficit is 3 percent, we add 3 more points of debt to the numerator, but the denominator also grows by 3 points. On the other hand, if the economy grows at 1 percent, we need to bring the general government deficit to 1 percent to stabilize the debt. This takes considerably more fiscal effort.

The same is true of many state obligations, such as pensions and public health care. These social benefits are much more onerous to maintain when, along with the fall in the working-age population, we are faced with a lengthening of life expectancy. While social costs rise rapidly, the economy lags behind. Changes such as raising the retirement age help, but they do not significantly change the basic scenario. By working longer, we can slow down the fall in the active population, but we do not stop it.

In fact, the arguments in the previous paragraphs may be too optimistic. Will labor productivity continue to grow by 2 percent even if the population falls? There are reasons to doubt it.

Knowledge, Creativity, and Innovation

Earlier, I stressed that economic growth is based on recombining new ideas. What do I mean here by ideas? I mean any creation of the human mind that allows us to transform a resource into a good or service. For example, one idea many centuries ago was to use silicon to make concrete. More recently, it occurred to us to use silicon for transistors (like the ones you are using to read these lines). Just a few weeks ago, there were major breakthroughs in using silicon to make better batteries for electric cars. But other ideas include new theorems in mathematics (important, for example, for your credit card to work on the internet) and the development of new forms of business. Founding Amazon or the invention of cost accounting were as much innovations as a new chemical process.

And who creates these ideas? People. Ideas are the result of research effort and creativity. Therefore, all else being equal, the flow of ideas in a society depends on the number of people thinking. It is virtually certain that a society with 200 million people will develop more innovative ideas than a society with two million, provided that the economic institutions are similar. Switzerland produces more ideas than Nigeria because it has better institutions, but Switzerland produces fewer innovative ideas than the United States because it has fewer people. Smaller populations, even in the countries of the world with better innovative institutions (United States, East Asia, Western Europe), are going to be populations with fewer innovative ideas.

This phenomenon may be particularly pressing if we note that the evidence suggests that, as we accumulate knowledge, it is increasingly difficult to create new ideas. Humanity will never have a new Galileo Galilei, Isaac Newton, or Charles Darwin. The foundational ideas in physics, mathematics, and biology that these scientists developed cannot be “reinvented.” Even the relativity theory or quantum mechanics of twentieth-century physics, with all their novelty and dramatic consequences, were more refinements of existing cognitive structures than radical breakthroughs, as was the invention of the experimental method or the development of infinitesimal calculus. Newton was probably not wrong when he argued that he could see further because he stood on the shoulders of giants, but even from up there more and more clouds prevent us from having a clear view.

I notice it a lot in my daily work. Soon, I will start teaching a PhD course on optimal control. This is the field of applied mathematics that analyzes how to control a dynamic system to achieve the best possible results over time. In economics, for example, this theory is applied to study how to manage a portfolio of investments over time to maximize its return, given a certain level of risk. When I was a student in the late nineties, I estimate that it took about twelve months to specialize in the field (once you finished the basic PhD courses) and to be ready to start writing a groundbreaking thesis at a global level. Today, I estimate that it takes at least twenty-four months. The number of things we have learned about optimal control in the last two decades is spectacular. But this also means that coming up with new ideas in this field is more complex than ever, and one has to learn many more things. The fathers of this specialization, Richard Bellman and Lev Pontriaguin, had it much easier: everything was yet to be discovered. This does not detract in any way from their achievements (they were both great geniuses), but it does put the merits of the current generation of young researchers into perspective.

For the last three centuries, humanity has been participating in a race in which, on the one hand, it is increasingly difficult to come up with new ideas, but on the other hand, there are more and more of us engaged in research. These two forces have counteracted each other, and the result of the race, so far, is that we have been able to develop new technologies and scientific advances that have given us that 2 percent average annual growth in labor productivity.

With a falling population, we will start to lose the race. It will be increasingly difficult to increase the total number of academic researchers and business innovators. Many people have no interest or ability to do research, and each additional researcher is one less person working in the production of goods and services. As a society, we can’t all dedicate ourselves to innovation. Someone will have to apply that innovation to produce things we like.

In other words, a shrinking human population can also be a much less dynamic population from the point of view of innovation. Many economists argue that the effects are already being felt in the creation of new businesses and in the poor productivity since 2008.

To return to our calculations: let’s assume that, as a result of decreasing innovation, labor productivity will only grow by 1 percent per year. With a 1 percent fall in the working-age population, the “new normal” will be 0 percent growth in gross domestic product. How are we going to pay for the welfare state and our level of public debt with zero average growth? It doesn’t add up.

Robots Won’t Save Us

I often come across the argument that automation will save us. If we have enough robots and develop artificial intelligence systems, the argument goes, we can continue to grow without a problem. My response is always that this was the idea behind the Soviet Union’s economic strategy; it didn’t work in the twentieth century, and it won’t work now.

In 1928, Stalin embarked on a program of accelerated industrialization based on very high rates of investment. The idea was to accumulate enough physical capital to be able to produce enough consumer goods in a few decades to achieve communism. The problem with this investment strategy is that the accumulation of physical capital is subject to diminishing marginal returns. Building the first blast furnace in Magnitogorsk in 1932 had very high returns: we go from producing no steel at all to producing steel that has a very high marginal value. The second blast furnace in the 1950s had a much lower yield. The last blast furnace, completed in 1987, was almost worthless. Think about it with the televisions in your house. The first television we buy, which we put in the living room, is very useful. The second television, for the bedroom, is fine, but it’s no longer the same. The third television in the kitchen helps, but not much. The fourth television stays in the cupboard. Just by looking at the diminishing marginal returns of physical capital installed in the Soviet Union one can understand, almost exactly, the high Soviet growth rates in the 1930s, the average rates in the 1950s and 1960s, and the stagnation of the 1970s and 1980s.

Robots are another form of physical capital, perhaps more interesting than a blast furnace, but not essentially very different. And as such, they are also subject to diminishing marginal returns. The first robot has high marginal returns, the second somewhat less, the third is of little use.

That is why I never use the word “capitalism” to refer to the economic system we have. Emphasizing the word “capital” makes us believe that the key to modern economic growth is to accumulate physical capital, be it blast furnaces or robots. No, it is not at all. We grow because we have more and better ideas. We accumulate capital to produce those ideas, not the other way around. Britain, and then the rest of the West, led the industrial revolution and modern economic growth because they were the first societies that, around 1650, began to have institutional structures that encouraged the systematic and constant production of new ideas. In short: with a smaller population in 2100, we are likely to have fewer innovative ideas and with them, less productivity growth.

Could I be wrong? Of course! Advances in deep learning in recent years may make it easier to develop new ideas even with fewer researchers. Ten years ago, I would not have ventured to guess that today we would have deep neural networks that can predict protein folding. Returning to the example of optimal control that I mentioned earlier, deep neural networks make it possible to solve problems that were impossible even two years ago. It is also possible that new technologies are not subject to the same diminishing marginal returns as the technologies of past centuries. For example, data are non-rivalrous goods: using data in one line of business of a company does not limit its uses in another line of business. By comparison, using a machine in one line of business does preclude its use in another line of business.

Will these changes be powerful enough to defeat the effect of population decline on the creation of new ideas? I, following Robert Gordon, tend to be pessimistic that these changes will be enough, but I would like nothing better than to be wrong.

Levan Ramishvili

From Facebook to Amazon, Google, and Apple, large corporations increasingly gather huge amounts of data on their users, then use that data to predict behavior, tailor the content to display, or suggest products for purchase. But the use of such complex calculations is not limited to private corporations.

There are increasing calls from prominent individuals to put faith in the power of machine learning to determine national policy. In November 2016, for example, Jack Ma, founder of retail giant Alibaba, stated:

Over the past 100 years, we have come to believe that the market economy is the best system, but in my opinion, there will be a significant change in the next three decades, and the planned economy will become increasingly big. Why? Because with access to all kinds of data, we may be able to find the invisible hand of the market. The planned economy I am talking about is not the same as the one used by the Soviet Union or at the beginning of the founding of the People’s Republic of China. The biggest difference between the market economy and planned economy is that the former has the invisible hand of market forces. In the era of big data, the abilities of human beings in obtaining and processing data are greater than you can imagine. With the help of artificial intelligence or multiple intelligence, our perception of the world will be elevated to a new level. As such, big data will make the market smarter and make it possible to plan and predict market forces so as to allow us to finally achieve a planned economy.

The term “Artificial Intelligence” (AI) describes computer programs that can model the environment of their assigned tasks and act autonomously to maximize their chances of succeeding in those tasks. In particular, “Machine Learning” (ML), a variety of AI using specialized algorithms to enable learning from mistakes and new data, has flourished in the last fifty years. It has recently begun to be employed in the fields of economics, social science, and public policy.

The increasing sophistication and competence of machine learning in these fields has given public policy analysts misguided confidence in the ability of machine learning-aided economic policy to substitute for human decisions. The truth is, these new methods repeat the errors of previous attempts to automate and centralize economies. Although machine learning demonstrates an impressive capacity to solve complex analytical problems, it only finds associations rather than meaningful causal relationships, and it is unable to overcome fundamental information incentive problems that the free market adequately solves. In other words, in spite of Mr. Ma’s optimism, artificial intelligence will simply never be smart enough to replace the free market.

The Power of Machine Learning

Artificial intelligence and machine learning are powerful tools for recognizing patterns with remarkable accuracy. Imagine, for instance, that we try to predict credit card fraud using dozens of data points from credit card transactions (e.g., the time of day and week when the transaction occurred, the item purchased and its price, the use of the credit card in the previous twenty-four hours, etc.).

In this case, ML is helpful, because we don’t need to know which characteristics of transactions are relevant, nor what kind of relationship exists between the datapoints. If we have access to millions of credit card transactions and the knowledge of whether the transactions were fraudulent, we can “train” the model of the relationship, called the “functional form,” to fit past patterns to new data and detect, often with fantastic success, whether a new transaction is fraudulent. At a fundamental level, there is nothing very “intelligent” here: it is an exercise in massive data fitting. What is intelligent is that the process is highly automated and, therefore, easily scalable to multiple environments.

There are three main reasons why machine learning is currently in vogue. First, our computers have become much more powerful, capable of performing the data analysis that, for decades, academics had only theorized about. Secondly, thanks to the internet and cheap computing, we now have access to much larger and comprehensive datasets. In economics, for example, a typical empirical paper had a few hundred observations in the 1970s. Today, it is common to see papers with tens of millions of observations. That is why AI and ML are often associated with expressions such as “big data” or “data analytics.” Finally, computer scientists and applied mathematicians have made huge advances in the efficiency of machine learning techniques that, in concert with growing computational power and datasets, have increased the feasibility of data analysis techniques that were previously only theoretical.

In order to harness the power of machine learning, incredibly large datasets are required. The rule of thumb in the industry is that one needs around a million labeled observations to train a network. These enormous datasets have arisen from two primary situations. First, large firms like Netflix and Amazon gather a lot of information from customer activity, allowing them to predict what else you might want to watch or purchase. Secondly, new techniques generate all possible permutations of data observations and identify relationships within these data that we can compare to data we find in the real world.

Public Policy and the Limits of Machine Learning

Unfortunately, in many areas of public policy, we do not have access to such a wealth of data and, most likely, we never will. Take the example of setting monetary policy, i.e., the regulation of how much money to supply, typically conducted by national central banks, such as the Federal Reserve in the U.S.

Monetary policy is a relatively straightforward topic with fewer moving parts than other kinds of economic policy. Could machine learning ever replace the Federal Market Open Committee (FOMC, the main policy instrument of the Federal Reserve System)? I am skeptical. For one thing, the FOMC usually has a limited amount of data. In the United States, we only have reliable data for output, consumption, and investment after World War II and, even then, only at a quarterly level. If we count them, from 1947:Q1 (the first “good” observation in terms of the accuracy of our measurement) until 2021:Q2 (the last observation as I write this), we have 298 data points. This is far fewer than acceptable for machine learning techniques.

Furthermore, the US economy has radically changed, which limits the relevance of older data. We have moved from an economy dominated by manufacturing into an economy driven by services, and financial innovations have transformed the relationship between financial and real variables. The evolving structure of the economy shifts the relationships between the data points, making it harder for machine learning to find clear patterns. These structural changes mean that econometricians often do not use observations before the early 1980s when they estimate the effects of monetary policy on output. In fact, such estimates change sharply depending on whether we include early observations. Moreover, the economy is bound to continue to change, meaning we will continue to have to deal with newer and newer data.

Employing individual data (such as consumption data of households or financial transactions) can help us get more observations, but we will still encounter similar problems. Ponder, for example: how informative are the consumption patterns of married couples in the 1990s, in their early 40s, with several kids at home, about the consumption patterns of single individuals in the 2020s, also in their early 40s, without kids? Moreover, there are severe limitations on what individual data can teach us in the absence of detailed explanations about the nature of relationships between different data points.

This additional problem with using microdata is an instance of the Lucas critique, named after Robert Lucas, one of the most influential economists of the last century. The essence of the critique is that it is difficult, if not impossible, to distinguish in data how much behavior is attributable to unobserved characteristics or to the impact of particular public policies.

Machine learning faces the same problem that economists have faced for a century: distinguishing causation and correlation. Moreover, the answer that machine learning provides is valid only under a constant set of circumstances: changes in policy may affect different individuals differently, which gives misleading results about the impact of a policy.

If an airline tightens its rules for upgrades in a way that implicitly favors business-class travelers with few but expensive trips, this type of traveler will react differently to the change than business class travelers who make more regular, shorter trips. Machine learning, which operates without a theory of the decision-making that underlies external behavior, will only identify associations between rule changes and purchase activity, rather than true customer preferences. Moreover, experimentation with different policies to observe greater variation in behavior is often infeasible or even immoral. An airline cannot sporadically alter its upgrade rules unless it wants to alienate its customers, just as we cannot perform experiments with national monetary policy without risking wild economic fluctuations.

Secondly, experimenting on a sample will only allow machine learning to give an explanation for individuals in that sample. For example, administering a lottery for applicants to charter schools will only be able to tell us about the impact of charter schools on those who have applied, and not about the general population, many of whom did not apply. Furthermore, firms nevertheless often enjoy greater scope for experimentation than national governments; imperfect even for many firms, machine learning is all but unavailable to national governments.

Free Markets, Not “Digital Socialism”

The fundamental problem with relying on machine learning to recognize economic trends and determine economic policy coincides with the reasons that Friedrich Hayek gave against conventional, socialist central planning. The objections to central planning are not that solving the associated optimization problem is extremely complex, although it is. If that were the only problem, AI and ML could perhaps help us solve the problem. The objections to central planning are that the information planners need is dispersed and, in the absence of a market system, agents will never have the right incentives to reveal it or to create new information through entrepreneurial and innovative activity.

A simple, real-life application of central planning illustrates this point. Every year, the department of economics at the University of Pennsylvania faces the challenge of setting up a teaching distribution for the next academic year. Each member of the faculty submits her preferences in terms of courses to be taught, day of week, time of day, etc. The computational burden of finding the optimal allocation is quite manageable. We have around thirty-two faculty members. Once you consider that certain professors have particular specialties, the permutations to consider are limited. A few hours in front of Excel deliver the answer: it seems a central planner at Penn Economics can do her job.

The real challenge is that, when I submit my teaching requests, I do not have an incentive to reveal the truth about my preferences nor to think too hard about developing a new course that students might enjoy. I might not mind teaching a large undergraduate session on a brand-new hot topic and, if I am a good instructor, the students will be better off. However, I will not be compensated for the extra effort, even if that extra effort is minimal, and thus I will have an incentive to request a small section for advanced undergrads on an old-fashioned topic. This outcome is not optimal. If the Dean could, for instance, pay me an extra stipend, I would teach the large, innovative section, the students would be happier, and I would be wealthier. Even this alternative, however, would be subject to more sophisticated strategic information manipulation as my colleagues and I vie to optimize our course loads according to our personal preferences.

The only reliable method we have found to aggregate those preferences, abilities, and efforts is the free market, because it aligns, through the price system, incentives with information revelation. This method is not perfect, and its outcomes are often unsatisfactory. Nevertheless, like democracy, all the other alternatives, including “digital socialism,” are worse. By and large, we should still rely on markets to allocate resources.

Markets work when we implement simple rules, such as first possession, voluntary exchange, and pacta sunt servanda (“agreements must be kept”). We did not come up with these simple rules thanks to an enlightened legislator or a blue-ribbon committee of academics “with a plan.” On the contrary, these simple rules were the product of an evolutionary process. Roman law, the common law, and the lex mercatoria of medieval merchants were bodies of norms that gradually appeared over centuries, thanks to the decisions of thousands and thousands of agents. The forces of evolution and trial and error produced the optimal solution to what economists call a mechanism design problem. Those who believe machine learning can do the same will be sorely disappointed.

Levan Ramishvili

In the first essay in this series on the demographic future of humanity, I explained how there is a high probability that the human population will peak between 2050 and 2060. Since I wrote the essay, two new facts have reinforced my prediction. First, Chinese authorities announced that there were 10.6 million births in mainland China in 2021 (vs. 12 million in 2020). Given that there were 10.1 million deaths, mainland China’s population grew by a tiny 480,000 inhabitants (before net migration, which was likely to be close to zero). And since births decreased at a roughly constant rate during the year, it is most likely that China’s population peaked in the early summer of 2021 at slightly above 1.4 billion, and that its population is already falling now.

Second, India now estimates that its fertility rate is 2.0 (1.6 in urban areas and 2.1 in rural areas), below replacement rate. The updated estimates predict that India’s population will peak around 2050 at 1.6 billion (my personal forecast is that it will peak earlier and at a lower level). In the second essay, I discussed how population decline will bring some major economic challenges that will jeopardize the maintenance of the welfare state and the growth of economic productivity.

In this final essay, I will outline some foreseeable consequences of these trends that concern matters fundamental to society, such as the family or housing.

The task, however, is a delicate one. As a society, we are venturing into uncharted territory. What ultimately happens will probably surprise us; therefore, the following paragraphs should be understood more as evidence-based speculations than detailed predictions.

Low Fertility and Aging Populations

But before we begin such speculations, it is important to point out that the fall in population will be accompanied by its aging due to increased life expectancy. Although fertility decline and an aging population are often conflated as a joint phenomenon, they are two separate issues. A society can suffer a population decline without aging (as happened during late antiquity in the West), while, conversely, we can have an aging population with stable fertility. However, fertility decline and aging are often mutually reinforcing. Allow me to explain.

In the undergraduate class I teach on the Political Economy of Early America, I always emphasize that grandparents were “invented” in the late eighteenth century in New England. I put the word “invented” in quotes because I am not referring to grandparents as a biological concept (since the dawn of humanity, we have all had grandparents), but as a key social category in family relations. The reason is simple: a combination of high per capita income (New England at the end of the eighteenth century was the richest region on the planet, and it also had relatively equal income distribution) with a climate unfavorable to the era’s most common infectious diseases (it was cold but not excessively so in winter, with moderate heat in summer) made it so that, for the first time in history, a high percentage of people survived long enough to be involved in their grandchildren’s lives. The idea of what a “grandparent” was and how they should interact with their grandchildren spread to the rest of the U.S. and Europe throughout the nineteenth and early twentieth centuries, as life expectancy also increased in those regions.

A simple way of showing how low life expectancy in earlier times prevented grandparenthood is to look at past European monarchs’ age of death. It is useful to note because, being at the top of the social pyramid, kings have always had access to the best doctors, food, and living conditions. And, with a few exceptions, European monarchs of the last five centuries were not burdened (mostly by choice) by an excessive workload or a stressful life.

Since I am originally from Spain, I will pick the Spanish monarchs, from the Catholic monarchs who created modern Spain to Alfonso XIII—the last king to die. Moreover, unlike other European monarchies, no Spanish monarch has ever been assassinated, so we have a fair assessment of “normal” life expectancy without violence. If we eliminated the kings of other countries who were killed (e.g., Charles I of England or Henry IV of France), the results for Spain and other European monarchies would be roughly the same.

Since men and women have different life expectancies, let’s focus on the age of Spanish kings at their death. Ferdinand the Catholic: 63 years; Philip I: 28 years; Charles I: 58 years; Philip II: 71 years; Philip III: 42 years; Philip IV: 60 years; Charles II: 38 years; Philip V: 62 years; Louis I: 17 years; Ferdinand VI: 46 years; Charles III: 72 years; Charles IV: 70 years; Ferdinand VII: 48 years; Amadeo I: 44 years; Alfonso XII: 27 years; and Alfonso XIII: 54 years. The queens’ ages at their deaths were: Isabella the Catholic, 53 years; Joanna I, 75 years; and Isabella II, 73 years. By comparison, Juan Carlos I, who has already enjoyed the advantages of modern medicine, is 84, a ripe old age, but by no means exceptional in advanced countries in 2022. Think of it this way: if you are 76 years old, you have already lived longer than any of the Spanish monarchs from the Catholic monarchs to Alfonso XIII.

In other words, reaching the age of 60 was already an achievement for the vast majority of the population (life expectancy was much lower, around 40 years, but this was weighed down by very high infant mortality). We should add that, in Western Europe, marriage (beyond the aristocratic elites) was relatively late from the late Middle Ages onwards, with grooms around the age of 25 or 26 and brides between 23 and 24 (this is called the European model of marriage).

That is, if a man married at 25 and the first child was born at 26 (the percentage of children born before marriage or less than nine months after marriage was small), the first grandchild could only arrive when the man was close to 52 (assuming the firstborn survived long enough to have a child, which usually did not happen). For a large majority of people, their lives were not long enough to see more than the first pair of grandchildren and to be in contact with them for, at most, a few years. Grandparents were distant figures, with whom people barely interacted, if they got to know them at all.

One Child, Many Adults

Today, when it is common to reach the age of 90, one can have a child at 30, a grandchild at 60, and live to see one’s first great-grandchildren. The consequences of this change in intergenerational relationships, especially in a low-fertility environment, are tremendous. Many children grow up surrounded by a high number of adults, but with very few children in their family environment. In China, for example, it is a cliché to speak of the “little emperors”: four grandparents, two parents, one child. The children enjoy a comfortable life with six adults around them and no “competitors.” They are given a monopoly on the emotional attention due to offspring. I still remember the question I was asked by a fellow PhD student in the United States who grew up in China under the one-child policy. Upon learning that I came from a large family, he asked, “How does it feel to have a sibling?”

The idea of having several siblings seemed so different from his life experience (and from all the people of his generation he had met in China) that the picture of my siblings he saw in my apartment fascinated him. Is it any wonder that today’s teenagers face more socialization problems than past teenagers, especially when they leave home? Or should we be surprised at the difficulty of creating intragenerational support networks?

But let us think of some more concrete consequences of this inverted pyramid of social relations. In many families, having four grandparents also means an inheritance of two homes, and two parents means an additional home. In other words, there is a clear expectation of a large transfer of wealth in the future. But, at the same time, such an inheritance may be delayed by many decades. What effects will these large but delayed inheritances have on the labor supply, savings, and investment of today’s young people? A dangerous combination of greedy expectations and endless waiting that we can call “Charles, Prince of Wales syndrome.”

At the same time, young people will rightly tell me that they find little consolation in having received this attention from adults or in thinking about future inheritances when all the social rungs are “occupied” by previous generations. Again, it is easiest to see this with an example. Think of firms of freelance professionals (law firms, consulting firms, auditing firms) or university teaching—careers that historically have provided opportunity (not perfectly, but not insignificantly) for social advancement. When lawyers or professors retired or died at the age of 60 or so, the doors were opened for the promotion of those who came behind them in the career ladder. Today, one constantly sees lawyers or professors at the age of 75 (in particular in countries like the United States where retirement is not mandatory) who are still at the peak of their careers. And, while society as a whole and these older professionals gain from enjoying many additional years of productivity, it is undeniable that this also causes “bottlenecks” among those who come after them.

If we add to this longevity the fact that positions in freelance professional firms and in university faculties will be reduced as the population falls—we need far fewer professors in a country where one million children are born each year than in a country where two million are born, no matter how much we increase the percentage of university students in each cohort—we can better understand the anxiety of many young people who wonder when they will have the opportunities that their parents and grandparents had. Is it any wonder, then, that many of these young people respond to this uncertainty about their future by delaying family formation and having far fewer children?

Rural Exit

All this becomes much more complicated when, in addition, we realize that these changes will not be evenly distributed throughout the territory, even if we concentrate on a single country.

With current fertility and reasonable immigration assumptions, it is very likely that China will lose around 600 million inhabitants over the next decades. Internal Chinese politics will not allow the arrival of 600 million immigrants, in particular since the only possible “sources” of immigrants are either India or Africa, and most Chinese will not easily accept these immigrants (this prediction is not a reflection of my preferences about the optimal level of immigration across countries). The problem is that those 600 million inhabitants are not only going to disappear from Beijing or Shanghai—they are going to disappear from the rural and interior parts of the country.

These big cities will continue to enjoy two advantages that they share with other large cities around the world. The first is that of urban life, which generates much higher labor productivity gains than in past decades: a phenomenon that economists still do not understand very well, but which is extremely well-documented.

The second reason is that large cities have abundant supplies of leisure goods (restaurants, bars, theaters, sporting events), which are in great demand among the younger generations. Large cities enjoy a tremendous comparative advantage in supplying leisure goods since there aren’t any adequate internet substitutes for them: you can work remotely, but “virtual disco” is not the same as disco in person. Moreover, these leisure goods go hand in hand with having few children: it is much easier to go to a trendy restaurant when you don’t have four boys to take care of at home. Many of my students in college tell me that their dream is to live in Brooklyn or San Francisco. I have yet to meet a student who has told me that their dream is to live in the back country of Pennsylvania (a lovely region in terms of natural beauty).

Also, in countries like the United States., the south and the southwest are going to attract more and more people because, as they grow wealthy or age, people tend to prefer warmer climates. Again, many investment bankers or successful lawyers I know have told me that they are saving up to buy a house in Santa Barbara, but I have yet to meet anyone who is saving up to move to North Dakota (the state with some spectacular national parks that everyone should visit). Maybe there are a few people out there dreaming of North Dakota, but it’s not the norm. The consequences of this accelerated depopulation of many regions will be felt across the board: first, and most immediately, in the political arena.

Consequences of Falling Fertility

Let’s concentrate in the U.S. New York state’s electoral college votes peaked at 47 in 1932. In 2024, the votes will be 28. In the same period, Florida’s electoral college votes have gone from 7 in 1932 to 30 in 2024. Let us think about this for a second. In 1932, New York State’s electoral weight was nearly seven times Florida’s weight. In 2024, it will be smaller. A U.S. president with the electoral map of 2024, or more pointedly, the electoral map of 2040, will be a very different person from the president with the electoral map of 1932. I do not give a lot of weight to the probability that I will ever see again a president from New York state in my lifetime (although politics is always full of surprises!).

The second consequence is that many regions will begin to run into problems in providing basic public goods, such as universities or hospitals, which require certain minimum sizes to operate with reasonable efficiency. There were 11,537 births in Maine in 2020. Let us imagine that 60 percent of those born in Maine in 2020 go to college in 2038 and that the number of students leaving Maine to study in other state or abroad is equal to the number of students arriving from other states or abroad (both assumptions are optimistic, especially when it becomes easier to enter into the universities in large cities as a result of falling fertility). This indicates that in 2038, there will be around 6,900 incoming college students in Maine. How many of the local colleges and universities can survive with that incoming cohort? I do not envy the job of the Maine education administrators in 2038.

But this phenomenon will happen all across the United States. Births have collapsed since 2008, putting US higher education in a delicate position. The big crunch in incoming cohorts will not affect Harvard, Princeton, or Penn that much. With a smaller total population of prospective students, top universities will only need to begin accepting applicants slightly lower in quality. For example, instead of accepting only the top 4 percent of applications, they will accept the top 8 percent of a smaller pool. The crunch will not affect Penn State or UC Santa Barbara that much either. The equivalent of some of their best students will go in 2038 to Ivies, but they can turn around and pick among the next best applications, the ones they are rejecting now just below the waitlist.

This ladder will move down the hierarchy of college selectivity until we get to the least selective level, where a lot of institutions will need to close or dramatically restructure. And no, bringing foreign students will not fix it. Recall my opening paragraph about China and India: because of the fast drop in fertility, it will be much easier for a Chinese student to get into Peking University in 2038 than in 2020. Thus, why bother coming to a second-rate U.S. institution?

Finally, we will see a radical change in housing prices. Let us return to the case of Maine or upstate New York. Who is going to buy all the empty houses left by a reduction in population? Some homes will disappear (demolitions or ruins in smaller towns, and the bad apartments built in the urban boom of the 1950s and 1960s will be abandoned), others will be transformed into second homes and, finally, with smaller families, the average number of people per dwelling will fall. But, even discounting these effects, in 2040 or 2050, we will find ourselves with thousands of dwellings that nobody will want, which will push housing prices to the bottom.

Again, the biggest stress will come not so much from falling house prices, but the unevenness in price changes. Condo prices in Manhattan and houses in Santa Barbara will not fall unless there is a dramatic change in work and leisure patterns, which cannot be ruled out, but which I think is unlikely.

If current trends continue, in 2040 an apartment in Manhattan will be much more attractive than in 2021. But a house in the middle of upstate New York is going to be much cheaper. Families with real estate assets in the first set of locations will enjoy significant capital gains, and families with real estate assets in the second set of locations will suffer.

If this scenario worries you, and you want to propose a solution, ask yourself if this solution will work with a population that’s falling quickly (China) or stagnant (the United States) and whether it’s compatible with young people’s lifestyle preferences.

I shall conclude here. In these three essays I have written almost 10,000 words on humanity’s demographic future. Explaining all the ideas in these essays in detail, or presenting many more figures and justifying the empirical evidence, would easily take me a whole 250-page book. We will leave that for another time. At the same time, I have repeatedly tried to emphasize that society is a complex system that changes in unexpected ways. It may well be that all that I have said will come to nothing in a decade. But it is a fallacy to argue that because the future is uncertain one shouldn’t worry about current trends or do anything about them. Precisely because the future is uncertain, we should be even more careful and consider all scenarios. Unfortunately, most of us are not thinking in any detail about our demographic future.

Levan Ramishvili

For anyone tempted to try to predict humanity’s future, Paul Ehrlich’s 1968 book The Population Bomb is a cautionary tale. Feeding on the then popular Malthusian belief that the world was doomed by high birth rates, Ehrlich predicted: ‘In the 1970s hundreds of millions of people will starve to death.’ He came up with drastic solutions, including adding chemicals to drinking water to sterilise the population.

Ehrlich, like many others, got it wrong. What he needed to worry about was declining birth rates and population collapse. Nearly 60 years on, many predict the world will soon reproduce at less than the replacement rate.

But by my calculations, we’re already there. Largely unnoticed, last year was a landmark one in history. For the first time, humans aren’t producing enough babies to sustain the population. If you’re 55 or younger, you’re likely to witness something humans haven’t seen for 60,000 years, not during wars or pandemics: a sustained decrease in the world population.

A society’s reproduction level is measured by the fertility rate – the average number of children a woman has. The replacement level is accepted as 2.1: any higher and the population grows; any lower and it falls. Like the R number in epidemiology (which we heard so much about during the pandemic), the replacement level is a critical figure. Either side of it leads to dramatically different outcomes. The replacement level is put at a little over 2 to take account of the slight imbalance in male and female births – slightly more of the former are born. Also, not all girls survive until reproductive age.

According to the UN World Population Prospects, the global total fertility rate last year was 2.25 – a little above the replacement rate. But the UN was wrong. It’s not easy to calculate the figure because there’s a lack of statistics in many countries. In others, political constraints bind the organisation. For many places with reliable records, last year’s birth numbers were between 10 per cent and 20 per cent lower than UN estimates. In Colombia, the UN estimate was 705,000 births. Yet its national statistical agency counted 510,000.

There’s another reason to be sceptical of the UN figures – the replacement fertility level of 2.1 is valid for the UK, not universally. We get the 2.1 figure using a calculation: 1.06 boys are born for every girl in Britain. To ensure an average of one girl born, we need 2.06 children overall to be born. We then look at the probability a woman lives to reach her reproductive years, which in Britain is 0.98. To get the reproductive rate, we divide 2.06 by 0.98 – which equals 2.1.

However, in many developing countries fewer women survive to a reproductive age. Globally, the figure drops to 0.94. So the replacement fertility level needed worldwide is more than 2.1.

Many countries also have a higher male-to-female ratio, often due to selective abortion. In China, it’s around 1.15; in India, 1.1. An estimate for the sex ratio globally is 2.08. To estimate a global replacement fertility rate we divide 2.08 by 0.94, which comes out at 2.21 children per woman.

By adjusting the UN’s figures to account for the lower births in many countries, I estimate the global fertility rate last year was 2.18, i.e. below the 2.21 replacement threshold. It could be even lower than that, as it’s likely that the birth rate in many African countries saw a larger fall than the UN estimated.

This doesn’t mean the global population is already falling. ‘Demographic momentum’ means that women born in the 1990s and 2000s are currently having children, while their parents’ generations haven’t yet died. Longevity, meanwhile, is increasing. So although global births are falling, they still exceed deaths. At present rates the human population will peak in around 30 years. Then start plummeting.

Economists have long predicted fertility rates would decline as countries become wealthier. But the fall over the past decade has happened in rich, middle-income and poor countries. It has also been faster than anyone predicted.

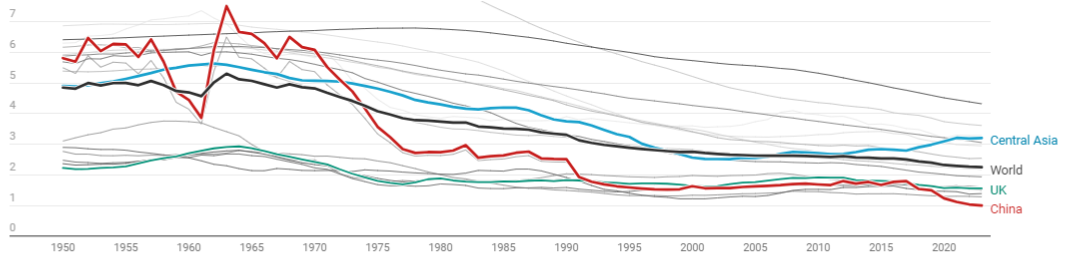

South Korea is the most extreme case. The fertility rate last year was 0.72 – roughly one-third of the replacement rate. In 2015, it was 1.24. In less than a decade, South Korea has transitioned from very low fertility to astonishingly low. And there’s no sign of this decline slowing. The same trend can be seen across Asia (China, Vietnam, Taiwan, Thailand, the Philippines and Japan).

But it isn’t unique to Asia. Turkey’s fertility rate plummeted from 3.11 in 1990 to 1.51 in 2023. The UK’s was 1.83 in 1990, 1.49 in 2022. The situation in Latin America is striking too: Chile and Colombia had rates of 1.2 last year, Argentina and Brazil were at 1.44 – all well below the UK. Each of them had high fertility rates three decades ago.

A non-exhaustive list of countries where the rate isn’t only below replacement but falling quickly includes India, the US, Canada, Mexico, Bangladesh, Iran and all of Europe. We know less about Africa because of poor quality data. The available evidence, however, suggests it’s undergoing a rapid decline: where we do have more reliable information – Egypt, Tunisia and Kenya – it shows fertility rates plummeting at an unprecedented pace. The only countries where fertility isn’t falling are the former Soviet Central Asia republics, and they are too small to make much difference.

👶 Fertility rates

The total number of children a woman might be expected to have in her lifetime, based on contemporary fertility rates. Worldwide, in UN-defined subregions of the world and in selected countries

Source: UN World Population Prospects 2024Get the data

Whenever I raise the issue of falling birth rates during lectures, I’m always met with three questions. The first is: won’t a falling population benefit the environment? This is misguided. A gently falling population could be good for sustainability, but we’re facing population collapse and economic turmoil. Environmental concern is a ‘luxury good’: we do it more when prosperous. Voters in 2050 in a country with acute budgetary problems caused by an ageing population will care a lot less about global warming.

The second question is: can’t we bring in more immigrants? But the falling population is for the planet, not one country. Every Argentinian who moves to Spain alleviates Spain’s demographic woes but aggravates Argentina’s. This argument also ignores the huge number of immigrants needed to keep the population constant in countries such as South Korea. By 2080, 80 per cent of people living there would need to be immigrants or the children of immigrants. Can any society absorb so many without social unrest?

It’s not clear either that immigration fixes pensions or healthcare costs. When immigrants are young, they pay taxes; as they grow old, they draw pensions and use health services. The same is true for first- and second-generation immigrant children.

The third question is: won’t AI make a population collapse immaterial by doing all the work for us? This is wishful thinking. AI’s effect on productivity won’t match the hype. Daron Acemoglu, a leading expert on the macroeconomics of AI, estimates it will increase productivity by 0.66 per cent over the next decade. Even multiplying his estimate by ten, the figure would be much lower than what’s needed to overcome the declining labour force. The gulf between what the McKinseys of the world think and what the real experts think is vast.

Then there’s the fact that AI can’t deliver the services actually needed. It’s easier to teach a machine to read financial statements than to empty bedpans. The problems caused by population collapse, such as empty rural areas and unbalanced family networks, cannot be fixed by AI.

Countries from France to South Korea have introduced policies such as extended parental leaves and generous child tax credits. These have had limited success in reversing the decline. Raising a child is an 18-year commitment; extending parental leave from two to six months offers marginal relief. Ditto tax relief schemes.

Fertility rates have fallen faster in large metropolitan areas than in rural areas, probably because of housing costs. Take Bogota, Colombia. Last year its fertility rate was 0.9, far lower than in rural Colombia. The same is true in Mexico. In Mexico City, the fertility rate last year was 0.95, much lower than in rural Mexico. Both cities are very expensive. Extra-low fertility rates in South Korea are most likely driven more by the astronomical real-estate prices in Seoul than by any other variable. Small, expensive homes deter fertility.

Our societal structures have also become deeply unwelcoming to large families. Child car seats are a good example. In the UK, children must use a child car seat until they’re 12. There’s evidence this lowers birth rates as it makes it harder to fit more than two children in a car. When I was young my parents put four of us in the back seat. This isn’t to argue for repealing car-seat regulations, but it’s an instance of government policies having unintended consequences.

Another issue is that social norms have shifted: raising children isn’t a priority for many, not in the more conservative societies of East Asia or the more progressive ones of northern Europe. In 2016, China abandoned its one-child policy and allowed couples to have two children. The fertility rate increased from 1.57 in 2015 to 1.7 in 2016. By 2018, the effect had disappeared: it fell to 1.55 – lower than before the restriction was lifted.

If the UK government were to devise a strategy to increase the fertility rate from 1.49 to around 1.8 – still below the replacement rate but much closer to a sustainable level – it would need to address a mix of economic factors and societal support for large families.

Societal support could include making it easier for the young to marry. Safer streets would allow children to spend more time unsupervised and travel to school on their own, easing the burden on parents. School holidays could be organised in ways that don’t disrupt parents’ work.

Creating the conditions for large families to flourish is the only way to reverse the trend in fertility rates. If we fail to do so, then the coming demographic winter will be far harsher than anyone cares to admit.

Levan Ramishvili

Humanity has entered a new era of rapid population decline. Globally, the total fertility rate is likely already below replacement—that is, below the level needed to sustain the population in the long run, approximately 2.18 children per woman. In the US, it’s around 1.6 – without immigration, our population would have already begun to decline. If we are unable to address our fertility crisis, the US will face an existential economic crisis driven by a steep decline in fertility rates—one that could have an impact measured in the quadrillions of dollars.

Being “below replacement” does not mean global population will immediately stagnate. Due to a phenomenon known as population momentum, growth will continue for approximately 30 more years. Current world births are temporarily high because large cohorts of women born in the late 1990s and early 2000s are now having children while their parents are still alive. However, all of today’s global population growth is a solely a result of this momentum.

Few countries remain above replacement—except for those in sub-Saharan Africa and Central Asia. Furthermore, fertility rates are declining more significantly and, importantly, at a faster pace than anyone anticipated a few years ago. This trend is evident in both wealthy and poor nations, in religious and secular states, in countries with right-wing governments, as well as those with left-wing governments, and in nations with free abortion access and those with restrictive abortion laws. Pick any country at random from a world map, and the chances are high that its fertility rate is falling rapidly.

In the Americas, from Alaska to Tierra del Fuego, only Haiti, Honduras, Bolivia, Paraguay, and a handful of small Caribbean nations are on pace to exceed replacement levels in 2025—and only slightly. The region’s demographic giants—the US, Brazil, Mexico, Colombia, Argentina, and Canada—are already significantly below replacement. Notably, as of early 2025, the US has a higher fertility rate than Brazil, Mexico, Colombia, Argentina, and Canada.

In Asia, countries like China, India, Japan, Vietnam, Thailand, Turkey, Iran, and South Korea—among many others—are all significantly below replacement levels. In China, Japan, South Korea, and Thailand, deaths currently outnumber births; these countries have exhausted their momentum, resulting in population decline. At the present rate, China could lose as many as 600 million inhabitants by the end of the century.

Sub-Saharan Africa presents a less clear picture, as data quality is poor (many of the UN’s figures are based on estimates). Nevertheless, some signs suggest that fertility is declining there as well. Three weeks ago, an economist from Ghana told me, “Nobody in my village is having kids anymore.” The plural of anecdote is not data, but his observation aligns with other indicators.

Currently, the fertility rate in the US is around 1.6, significantly below the replacement rate of 2.1. (Note that the global replacement rate of 2.18 is slightly higher than that of the US due to selective abortion of girls in Asia and higher female mortality in Africa). This issue is not new; the US has been below the replacement rate since the 1970s, although the recent decline in fertility is unprecedented. In fact, without the influx of immigrants (like yours truly) and their US-born children, the US population would likely have started to decline a decade ago.

The implications of declining fertility in the US are the most crucial economic issue of our time.

Consider the fundamental accounting equation for economic growth. Output growth is equal to the growth rate of output per worker (a measure of productivity) plus the growth rate of the labor force. Since the Civil War, the long-term average growth rate of output per worker in the US has been approximately 1.9% annually. This rate has occasionally been higher (as seen in the 1950s and 1960s) and at other times lower (as observed in the 1970s and 2010s). However, deviations from this historical average have generally not been significant.

Therefore, when the number of workers increased by about 1% annually, US economic growth remained around 2.9% per year. During strong years—particularly during economic expansions when productivity surged—the economy achieved growth rates of 4% or more. In weaker years, when productivity slowed or fell, output grew by only 1% or 2%. Total output only shrank for an entire year on rare occasions.

Fast forward to the 2040s, when the growth rate of workers may be -1% per year. Even if we maintain the output per worker growth rate at 1.9% (a big if), the economy will grow at a meager 0.9% annually. In prosperous years, we could reach 2%; in downturns, the economy will contract, not just grow more slowly.

Is this an unlikely scenario? Unfortunately, no. We have already witnessed it—it’s called Japan.

The implications of declining fertility in the US are the most crucial economic issue of our time.

Between 1991 and 2019, Japan’s GDP grew at an annual rate of 0.83%, significantly lower than the US rate of 2.53%. The main driver of their weak economic performance? Japan’s dramatic demographic collapse.

Between 1991 and 2019, a combination of past low fertility and population aging led to a 0.54% annual decline in the number of working-age adults. Total hours worked fell at a similar rate of 0.43% per year; the gap between these figures reflects increased labor force participation among older workers and women.

In contrast, the US, bolstered by higher fertility rates and significant immigration, experienced an annual growth of 0.91% in its working-age population, with total hours worked increasing by 1.04%. Consequently, Japan’s GDP per working-age adult grew at a rate of 1.39% per year, compared to 1.65% in the US—a relatively minor gap. When measured by output per hour worked, Japan’s growth was at 1.26% per year, while the US recorded 1.53%.

Excluding the early and middle 1990s, when Japan was engulfed in the aftermath of its real estate bubble, Japan’s growth per working-age adult from 1998 to 2019 outpaced that of the US

Japan’s weak economic performance over the past 25 years is not a mystery; it is merely the result of a declining population. Demographics shape destiny, even in terms of economic growth. In other words, Japan’s current economic situation (good performance of growth per working-age adult but poor total output growth) foreshadows the future of the US economy.

The consequences of significantly slower output growth will be severe for the US economy. While we consider output growth per capita when assessing welfare (and output per capita growth will not decline as sharply as total output growth), total output growth is crucial for addressing the funding of Social Security, Medicare, Medicaid, servicing our public debt, and financing our armed forces in the face of increasing international competition. Once we begin to contemplate the fiscal implications of a declining population, it becomes difficult to focus on anything else.

When I reach this point in seminars, lectures, or media interviews, I invariably receive three questions: climate change, immigration, and artificial intelligence.