Recursive step

Aaron MacNeil

# Lognormal distribution of P's

Pmean0 = 0.

P_0 = Lognormal('P_0', mu=Pmean0, tau=isigma2, trace=False, value=P_inits[0])

P = [P_0]

# Recursive step

for i in range(1,nyears):

Pmean = Lambda("Pmean", lambda P=P[i-1], k=k, r=r: log(max(P+r*P*(1-P)-k*catch[i-1],0.01)))

Pi = Lognormal('P_%i'%i, mu=Pmean, tau=isigma2, value=P_inits[i], trace=False)

P.append(Pi)

I've wanted to speed this up for a while as this looping is tremendously slow, but I'm having difficulty thinking how it might be done. Ideas?

Thanks much,

Aaron.

Flavio Coelho

One possibility is to look into the multiprocessing module. As most CPUs nowadays are at least dual core, you can cut you time in (at least) half, by creating a pool of processes, turning you loop into a function which you call using map, and passing range(1,nyears) as argument. The documentation has examples that you can easily adapt to your code.

it would look somewhat like this:

P=Pool()

def your_loop_core(i):

....

P.map(your_loop_core, range(1,nyears))

P.join()

P.close()

regards,

Flávio Codeço Coelho

================

--

You received this message because you are subscribed to the Google Groups "PyMC" group.

To post to this group, send email to py...@googlegroups.com.

To unsubscribe from this group, send email to pymc+uns...@googlegroups.com.

For more options, visit this group at http://groups.google.com/group/pymc?hl=en.

Chris Fonnesbeck

M. Aaron MacNeil

Thanks,

A.

David Huard

> It is distinctly faster, but also distinctly bad at converging - in fact it spirals out of control. The Metropolis steps converge on the known values. This is in line with my general experience with AdaptiveMetropolis - often if something isn't converging well, a forced Metropolis will solve the problem. Why might this be?

>

The AdaptiveMetropolis sampler performance hinges on a lot of

parameters being set correctly. We tried to make it as simple to use

as possible by setting a lot of parameters by defaults, but those

defaults regularly lead to convergence problems. Maybe one solution

would be to never assign AdaptiveMetropolis as the default sampler and

remove its default parameters. Users would need to work out by

themselves what parameter settings work best.

More fundamentally, the main issue with AM is finding the jump

covariance matrix. This covariance is computed from the last N steps,

hence the "adaptive". If for one reason or another this covariance is

problematic, chances are the next samples won't be good, leading to an

equally problematic update of the covariance. Conclusion is, you need

to start the AM sampler in the right track and make sure it stays in

the right track all along. I don't know if its possible to find a set

of parameters that provide those conditions for all problems. Maybe

not.

One thing that is already implemented and could help is using a past

trace to compute the initial covariance matrix. The strategy is to use

Metropolis on individual parameters for a while, then switch to AM to

speed things up, using the first trace to get a good initial

covariance. Maybe the AM sampler should do this by default.

David

Seth Flaxman

Roban Hultman Kramer

I don't have any insight into setting up initial covariance matrices,

but I've written some code to help graphically diagnose

AdaptiveMetropolis runs that you might find useful.

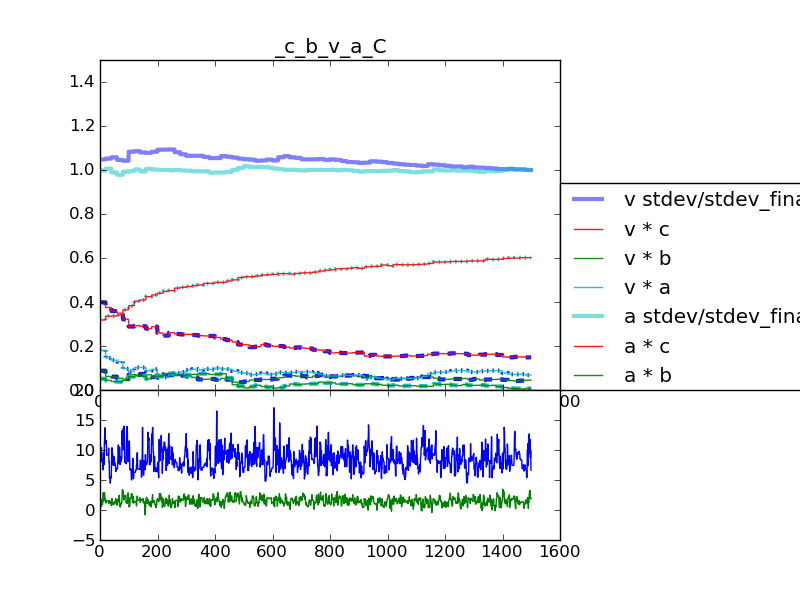

It's the plot_AM_correlation function in this module:

https://gist.github.com/793136

Direct link to the module file:

https://gist.github.com/raw/793136/0213c54789ae30c84b7e13947e3921c50ee9c632/plot2Ddist.py

Direct link to example script:

https://gist.github.com/raw/793136/7b6168ca4beb50e5d7f6a4100b580a5ea3eb38e9/plot2Ddist_example.py

Running the example script will produce a few plots (on screen). The

last plot is an example of plot_AM_correlation, showing the

correlations between variables calculated from the trace of the

Adaptive Metropolis proposal covariance matrix. Attached is an example

plot.

What you want to see: The variances (square root of the variance is

shown by the thick lines in the top panel) and covariances (or rather

correlations, shown by the other lines in the top panel) should look

like they converged to their final values early on. Any large

oscillations indicate unstable behavior in the algorithm. For

instance, if you have set shrink_if_necessary=True, and you continue

to see large drops in the variance, it indicates that few jumps are

getting accepted for some reason, and the algorithm keeps shrinking

the variance to try to increase the acceptance ratio.

Let me know if you have trouble running the example or applying it to

your own code, and feel free to email plots for help interpreting the

results.

-Roban

David Huard

This looks like a neat tool. Thanks for sharing it.

Seth,

Certainly others can chime in on this, but the acceptability of the

acceptance rate will depend on the dimension of the space you are

sampling from. In 1D, we usually target a 30%, 40% acceptance rate. As

you increase the dimensionality of the problem, that figure will

usually become lower. In my experience, problems occur when there are

less than ~3% jumps accepted during one update iteration of the

covariance.

As for the initial covariance matrix, certainly you can make a guess

about the expected value of the parameters you are sampling and a

rough estimate of their variance. Use the AM method `cov_from_scales`

to transform these guesses into a covariance matrix.

If users continue to share their experience about what works and what

doesn't, I'm hopeful we'll eventually find a strategy that works most

of the time and can be set as the default.

David

Chris Fonnesbeck

current development branch, so PyMC should not be selecting this step

method automatically for any model; it needs to be chosen manually.

It would certainly be useful for this sort of feedback to be formally

incorporated into the StepMethod. It shouldn't be too hard, for

example, to automate the switch from Metropolis to AdaptiveMetropolis

during the course of an MCMC run. The key will be coming up with

intelligent rules about when to pull the trigger.

In the meantime, to help Amac get some results (which was the initial

question in this thread), I am going to try to work up the surplus

example using the TWalk algorithm, which should improve the

performance significantly. Its in the sandbox now, and just needs to

be set up to work with containers properly.

cf

A. Flaxman

I was inspired by this discussion to do some experiments (and make some movies!) about when AM works and don't work. You can see the results here: http://healthyalgorithms.wordpress.com/2011/01/28/mcmc-in-python-pymc-step-methods-and-their-pitfalls

--Abie

cf

{kind=link}

Thomas Wiecki

these look great and are really helpful! It would also be interesting

to read _why_ these samplers have these problems and show this type of

behavior in the scenarios you give. But maybe that's beyond the scope

of your post and requires more background knowledge on Metropolis.

-Thomas