CA GROUPS

WELCOME TO CA GROUPS

CA GROUPS |

- CA Final Result Declared NOV 16 Exams Rank holders & Pass Percentage

- CA Exams Centre Wise Result Nov 16 Exams

- CA Final Nov 16 Topper Girl Who Repeats her Success: Eti Agarwal

|

CA Final Result Declared NOV 16 Exams Rank holders & Pass Percentage Posted: 18 Jan 2017 03:39 AM PST CA Final Result Declared NOV 16 Exams Rank holders & Pass Percentage.  CA Final Result Declared. Hey guys ICAI has declared Result of CA Final Students as well as of CA CPT Students on their official website on 17 January 2017. It was the day for which most of the CA students were waiting for about 2 months after their exams held in Nov 2016 . CHECK YOUR RESULT HERE. Team CA_GROUPS gives their Heartiest congratulations to all the CA Final students who have cleared their exams today. Further we give our Warm wishes to new CA Aspirants who have cleared their CA CPT and entered into real CA Course today. . Here we would like to inform all the students who had cleared their CA Final today that ICAI had already declared the dates for Campus Placements in the month of August September for different cities. You can see all the dates and other essential information from here:- CA Campus Placement Programme . But Some students (or we can say most after knowing the pass percentage) who were not able to clear the exams due to Low pass percentage by the ICAI or some other students we would like to quote famous line for Ca Students . “Where there is a will, there is a way – but for a CA Student After November there is a May” . Students who are not satisfied with their result may go for Revaluation/Rectification of their Exam Papers. The full procedure to do the same is elaborated by the Team CA_GROUPS here :- Procedure of Revaluation and verification of CA IPCC Final Exams . . If you are not able to find the correct answers of question asked in the Nov 2016 exams then you can find the same from here :- CA Final Solved Papers Nov 2016 . CA Final Pass Percentage of Nov 2017 ExamsThe pass percentage of students passed in the exams are given as below for your kind reference

CPT Result – 46.44%Rank Holders of CA Final Nov 2016 Exams

. CA Final Nov 16 Rank holders Mark Sheets

.

.

. The pass percentage of students passed in the previous exams are given as below for your kind reference.CA Final Pass Percentage of May 2016 ExamsThe pass percentage of students passed in the exams are given as below for your kind reference.

CPT Result – 38.98%Rank Holders of CA Final May 2016 Exams

. CA Final Pass Percentage of NOV 2015 Exams The pass percentage of students passed in the exams are given as below for your kind reference.

CPT Result – 34.45%Rank Holders of CA Final NOV 2015 Exams

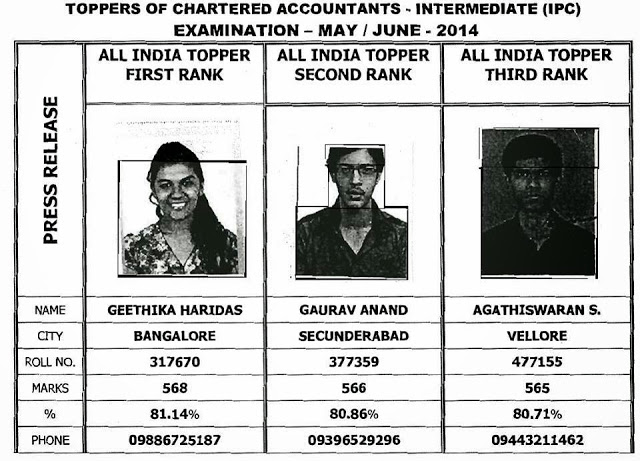

. CA Final Pass Percentage of MAY 2015 Exams The pass percentage of students passed in the exams are given as below for your kind reference.

Rank Holders of CA Final MAY 2015 Exams

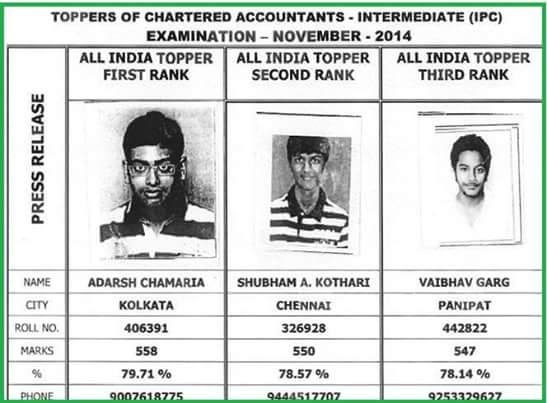

. CA Final Pass Percentage of November 2014 Exams

Rank Holders of CA November 2014 Exams

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

CA Exams Centre Wise Result Nov 16 Exams Posted: 18 Jan 2017 02:50 AM PST CA Exams Centre Wise Result Nov 16 Exams. ICAI has released CA CPT/ Final result Nov 2016 of centre wise all over India.All efforts are being made to rectify the same and restore normalcy shortly. We regret the inconvenience caused to the candidates and other stakeholders. we are sharing with you PDF’s of each region for both CA Final NOV 2016 and CA CPT DEC 2016. Download the region in which you or your friends fall and simply search there name or roll no. to check their result  CA Final Exams CENTERWISE RESULT Nov 16 :below is the region wise CA Final result for nov 2016 exams . Click below the list for each region and get the lsit of students who passed there CA Final exams today CA CPT Exams CENTERWISE RESULT Dec 16 :CPT Centre Wise Result June 16CENTRAL http://resource.cdn.icai.org/40754cpt-central-jan2016.pdf EASTERN http://resource.cdn.icai.org/40755cpt-eastern-jan2016.pdf NORTHERN http://resource.cdn.icai.org/40756cpt-northern-jan2016.pdf . CA FINAL Centre Wise Result May 16Hope this will help you to check your result of each region just simply search the name or roll no. of the person you want know. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

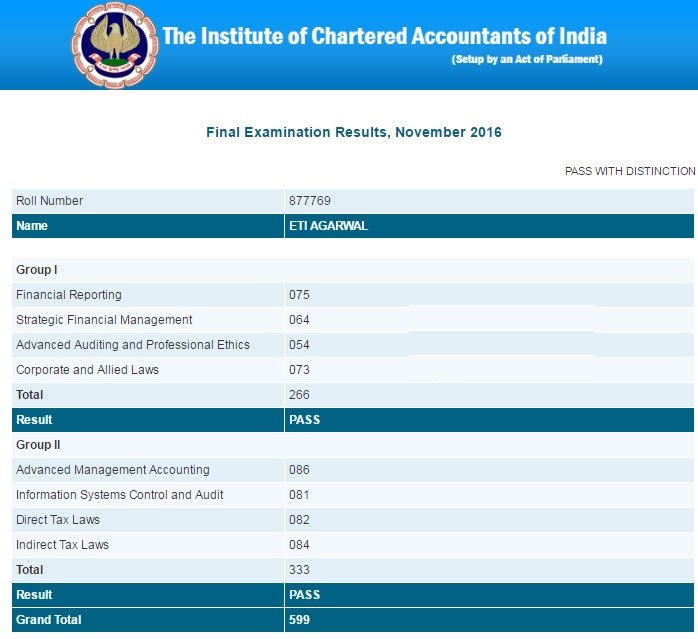

CA Final Nov 16 Topper Girl Who Repeats her Success: Eti Agarwal Posted: 18 Jan 2017 02:32 AM PST CA Final Nov 16 Topper Girl Who Repeats her Success: Eti Agarwal.

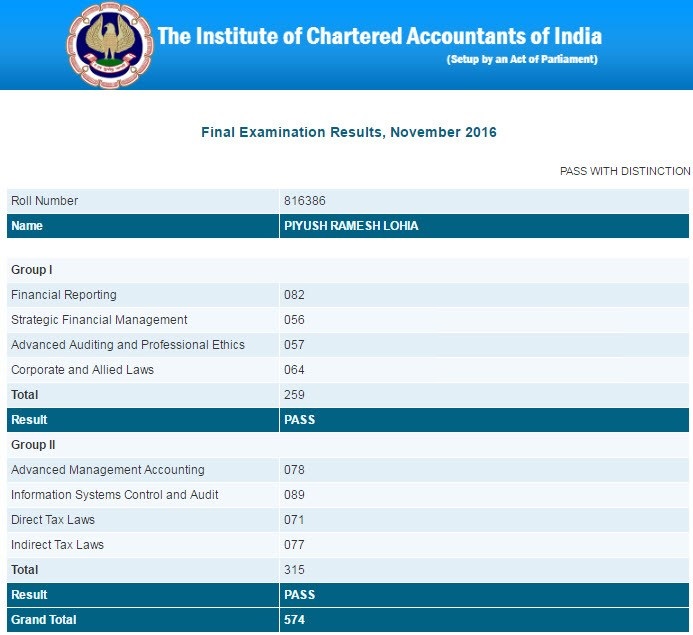

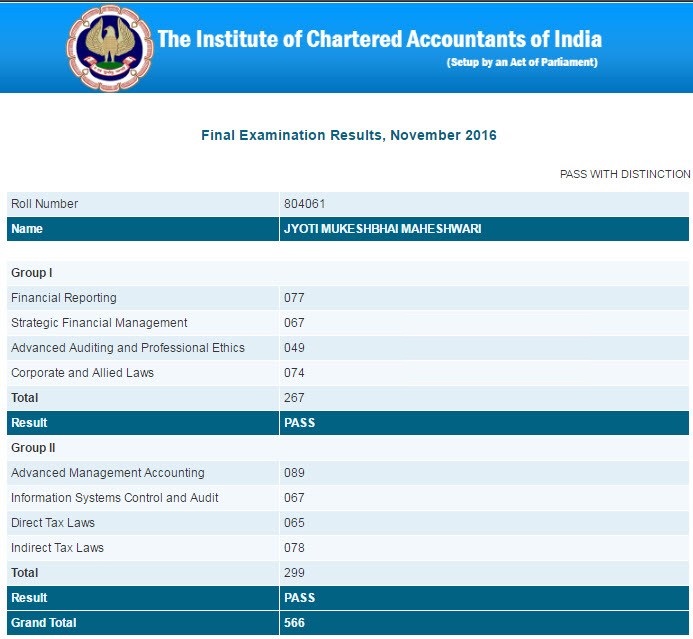

Eti Agarwal, CA Final Nov 16 exam topper. Yes the Girl who repeather success that she achieved in her IPCC Exams around 3 Years Back On 17th Jan 2017 as soon as Rankholders name announced by ICAI, a familiar name just stuck in my mind and that name is Eti Agarwal, I still remember that we posted on our Facebook page ( CA GROUPS ). A Bharatnatyam dancer, Eti Agarwal had also secured the All India Rank 1 at the IPCC Exams in November 2013 This is What we posted on 31st January 2014 when she got Rank 1 in CA IPCC :-  . “Ever since the results were announced, my cell phone has been keep on buzzing with calls from friends and wellwishers. It is so heartening to score the number one position in the exam,” said Eti in an interview CA Surbhi Bansal who teaches her Audit was delighted and shared this Pic of her on Facebook.  This is what she posted about Eti Agarwal : You nailed it again… AIR-1. So proud of you dear Eti Agarwal. Now, you are among the rarest of those who have been AIR-1 in CA IPCC and AIR-1 in CA final too. All Credit goes to your hard work and dedication during all these years. I am fortunate to have you as my student turned friend, to know you as a wonderful person you are… God bless!!! . CA Raj Kumar also show his happiness through his FB Post :-  . Currently Eti Agarwal is working with KPMG . Her father is also a Chartered Account. She has also given her CS Exams whose result was expected in Feb 2016 . We wish her all the best for her CS Result as well. We also have marksheet of Eti agarwal which we are sharing with you all , She Scored 599 out of 800 in her CA Final nov 2016 Exam to clinch the top spot.  . Second spot clinched by Piyush Ramesh Lohia and Jyothi Mukeshbhai Maheshwari comes third in the list. . Here below is the complete list of CA Final Rank holders of Nov 16 Exams

Share if you like it and must comment your views about her success and keep visiting for more updates |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| You are subscribed to email updates from WELCOME TO CA GROUPS. To stop receiving these emails, you may unsubscribe now. |

Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

WELCOME TO CA GROUPS

CA GROUPS |

- Article on COMPANY SECRETARIES: THE GOLDEN PEOPLES

- CA Eti Agarwal CA Rankholder Interview by- CA Surbhi bansal , CA Parveen Sharma and CA Raj kumar

- Taxable event under GST- Supply and its scope

- Job work under Revised GST Law if Job worker add his own material

- TAX DEDUCTED AT SOURCE As per Revised Model GST Law

|

Article on COMPANY SECRETARIES: THE GOLDEN PEOPLES Posted: 22 Jan 2017 12:26 AM PST Article on COMPANY SECRETARIES : THE GOLDEN PEOPLES. As being a member or a student of ICSI (company secretary course it always comes in our mind that what is a company secretary course how is started? How do we initiate? What is the scope of this Course? So here through our article all the question which comes in our mind as being a member or the student of the company secretary course . . so possibly we tried to answer the entire question through our this article.

Around 56 years back when our nation tries to uplift itself or on a path of development and growth pace and a number of companies registered itself as a corporate entity in India then there is a need arises for the compliances in the company and to carry on a companies in a systematic manner and as well a need of person who will be abide by rules and regulations able to help to the business entities to comply the rules and regulations and take a burden on their shoulder for the proper compliances of rules and regulation of the corporate entities . to fulfill this emptiness in the corporate field a course framed that is company secretary .now again the question is here why the word company secretary has been used for this profession so the answer is here, Secretary means a person a person employed by an individual or in an office to assist with correspondence, make appointments, and carry out administrative tasks, and same work the company secretary will do for the corporate entity to

So the word company secretary came into picture and our profession names as Define Company Secretary:

.

So here the answer is the in the year of 1960 the company law board started a course in company secretary ship leading to the award of government diploma in company secretary ship course grew the government promoted on 4 the October 1968 institute of company secretaries of India under section 25 of the companies act 1956for taking over from the government the conduct of company secretary ship examination the institute of company secretararies of India have ever since been converted into a statutory body w.e.f 1st of January 1981under the company secretary act 1980. Presently the institute of company secretaries of India divided into five regional council:

.

So the act itself answer the question that (a) Any person who immediately before the commencement of this Act was an Associate or a Fellow (including an Honorary Fellow) of the dissolved company; (b) Any person who is a holder of the Diploma in Company Secretary Ship awarded by the Government of India; (c) any person who has passed the examinations conducted by the institute and has completed training either as specified by the institute or as prescribed by the Council, except any such person who is not a permanent resident of India; (d) Any person who has passed such examination and completed such training, as may be prescribed for membership of the Institute; (e) any person who has passed such other examination and completed such other training without India as is recognised by the Central Government or the Council as being equivalent to the examination and training prescribed under this Act for membership of the Institute : Provided that in the case of any person belonging to any of the classes mentioned in this above who is not permanently residing in India, the Central Government or the Council may impose such further conditions as it may deem to be necessary or expedient in the public interest. So a person who is mentioned above can be company secretary. The first person who became company secretary in India was Mr. SH NARAYAN SWAMI with a membership number “A1” from Chennai. After that so many came and now the membership number reached near about 48000+. So this was the golden history of our valuable profession called COMPANY SECRETARIES (THE COMPLIANCE HEADS OF THE COMPANY) .

So the institute of company secretaries of India gave brief guidelines to grace his or her name with the initial called (CS) Stages to become a Company Secretary: The student who would like to join the Course after 10+2 pass or equivalent has to undergo three stages to pursue the Company Secretaries Course i.e.

The Student who would like to join the Course after passing the Graduation has to undergo two stages of the Company Secretary ship i.e. Executive Programme Professional Programme Foundation Programme which is of eight months duration can be pursued by 10+2 pass or equivalent students of Arts, Science or Commerce stream (Excluding Fine Arts) Executive Programme can be pursued by a Graduate of all streams except Fine Arts. Professional Programme can be pursued only after clearing the Executive Programme of CS Course (Time To Time Institute Do Efforts to Make This Profession Abreast) So after going through all the stages and after completing the necessary training of two years under a professional a person can grace his name with such dignified degree i.e. Company Secretaries (The Corporate Personality ) After successful completion of the examination and the completion of the training a person have to apply for the membership number and after due verification the institute will provide a membership no to the person and register a person MEMBER OF THE INSTITUTE THERE IS TWO PHASES OF MEMBERSHIP:

AS soon as the person qualifies all the level of examination and complete all the necessary training and applied for the membership number the INSTITUTE provide a membership number to the candidate termed as ASSOCIATE MEMBERSHIP NO. And after successful completion of 5 year a person who is holding an associate membership will be eligible to become a FELLOW MEMBER of the institute. .

After getting a membership number a company secretary can do a work in two ways:

The company secretary who according to: Section 2(2) of the Company Secretaries Act, 1980 (hereinafter called the Act) provides that a member of the Institute shall be deemed to be in practice when, individually or in partnership with one or more members of the Institute in practice or in partnership with members of such other recognised professions as may be prescribed, does any of the following in consideration of remuneration received or to be received: engages himself in the practice of the profession of company secretaries to, or in relation to, any company; or (b) Offers to perform or performs services in relation to the promotion, formation, incorporation, amalgamation, reconstruction, reorganisation or winding up of companies; or (c) Offers to perform or performs such services as may be performed by: (i) An authorised representative of a company with respect to filing, registering, presenting, attesting or verifying any documents (including forms, applications and returns) by or on behalf of the company, (ii) A share transfer agent, (iii) An issue house, (iv) A share and stock broker, a secretarial auditor or consultant, an advisor to a company on management including any legal or procedural matter falling under the Capital Issues (Control) Act, 1947 ** the Industries (Development and Regulation) Act, 1951, the Companies Act, 1956, the Securities Contracts (Regulation) Act, 1956, any of the rules or bye-laws made by a recognised stock exchange, the Monopolies and Restrictive Trade Practices Act, 1969, the Foreign Exchange Regulation Act, 1973*, or under any other law for the time being in force, (vii) Issuing certificates on behalf of or for the purposes of, a company; or (d) Holds himself out to the public as a company secretary in practice; or (e) Renders professional services or assistance with respect to matters of principle or detail relating to the practice of the profession of company secretaries; or renders such other services as, in the opinion of the Council, are or may be rendered by a company secretary in practice A person is called in whole time employment when a member of the institute of company secretaries of India is appointed by the company an employee of itself and provides a salary for their work done then that member is called as a member whole time in employment. Then what is the criterion of appointment of a company secretary in companies? So according to the companies act 2013 Section 203 of Companies Act 2013 read with Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014, necessitated that every listed company and every other public company having paid-up share capital of Rs 5 crores or more to appoint the Company Secretary in whole-time employment. .

A company secretary whether in employment or in whole time practice have vast avenue of working like:

A company secretary should perform the various roles mentioned below

It’s not enough now more avenues are ready to open for the company secretary:

Company secretary within the meaning of company secretaries’ act, 1980.

, NCLT, NCALT. So there is a different opportunities are available for the profession company secretary THE INSTITUE OF COMPANY SECRETATIES OF INDIA HAVE A MEMORENDUM OF UNDERSTANDING WITH DIFFERENT INSTITUTES TO.

NO, the profession company secretaries are not only restricted up to the territorial limits of the country the institute of company secretaries of India comply their responsibility time to time and give a very precious mou with the different nations and open the ways in the another nation too. There are some MOU which THE INSTITUTE OF COMPANY SECRETARIES OF INDIA MADE MOU WITH THE ICSA LANDON A Memorandum of Understanding between the ICSI and ICSA was signed on November 11, 1995 at Jaipur, India which recognized the common interest both the Institutes have in promoting best practice in `Company Secretary ship’ and professional administration and it was agreed to explore positive ways of ensuing a close relationship between them. OTHER BODIES ALL OVER THE GLOBE OF COMPANY SECRETARY

So the profession of company secretary is not restricted up to one nation it spread all over the globe the only need is to open your feathers and grab the opportunities it only upon the capabilities how much a member is able to grab it . Sometimes we also here that company secretary profession do not have any scope of working But I hope I well elaborated all the avenues of working of company secretary in India as well in abroad. So this is rightly said by some eminent authors that “Difficulties mastered are opportunities won”. So in each and every path of success there is difficulties and the warrior is he who over come such difficulties “Mrs. SMRITI IRANI (member of parliament ) said in her speech in NATIONAL CONVENTION Of the institute of company secretaries of India the all over the number of company secretaries are near about 75000 in which 50000 are from India “ And the person on whom the responsibilities lies on their shoulder are the person who is responsible enough and the company secretary is a designation on which whole building of the company stands and it is rightly said that “MAY HIGHER RESPONSIBILITIES WITH HIGHER DEGRAA OF POWER AND WIDE RANGE OF COMFORTS” And for such a valuable profession members of the company secretary should take a pledge that all the work which they done will be in the ambit of the rules and regulation because they are the regulators of the rules and regulation as well. . Written By: CS RAVISHANKAR PERIWAL CS SHEFALI BHARTI . The Author can be Reached at csravi...@gmail.com and csshefa...@gmail.com |

||||||||||||||||||||||||||||||||||||||||||||||

|

CA Eti Agarwal CA Rankholder Interview by- CA Surbhi bansal , CA Parveen Sharma and CA Raj kumar Posted: 21 Jan 2017 11:44 PM PST CA Eti Agarwal CA Rankholder Interview by- CA Surbhi bansal , CA Parveen Sharma and CA Raj kumar. So after huge success of Eti agarwal every one wants to know how she achieved this success and in series of interview given to aldine and Stargate CA Coaching institute she revealed her Success recipe for CA Exams. Interview at ALDINE was taken by one and only Parveen sharma sir ( Her accounts teacher) and Raj kumar sir ( her IDT Teacher) . which you can view here below. In this 35 Minute interview Eti told us every secret strategies that she opted in her CA Exams. most of this interview is in hindi so please Watch and share : . Second interview was conducted by Stargate CA . This interview was taken by CA Surbhi bansal who taught her Audit in CA Final and CA IPCC as well. Must watch this as well and share with your friends : . Do share with others if you like this and keep visiting cagroups4all.blogspot.com for more updates in future as well |

||||||||||||||||||||||||||||||||||||||||||||||

|

Taxable event under GST- Supply and its scope Posted: 22 Jan 2017 01:00 AM PST Taxable event under GST- Supply and its scope.  . Taxable event: Taxable event is very important matter in every tax law. Its determination is most crucial for the proper implementation of any tax law. Taxable event is that on the happening of which the charge is fixed. It is that event which on its occurrence creates or attracts the liability to tax. In the history of indirect taxation in India we have seen different taxable events in different indirect taxes. Sales, purchase, removal of goods, services, luxury, entertainment and so on, the list goes on. GST i.e. goods and service tax which we are going to witness will not only reform the whole of indirec taxes but also will reform the way of doing business in India. Taxable event under GST: One of the very important feature of the regime of GST is the complete change in the taxable event different altogether from the taxable events witnessed in the indirect taxes as yet. The taxable event in the GST would be supply of goods and/or services. As per Article 366(1A) of Constitution of India Goods and Services Tax means a tax on supply of goods or services or both except taxes on supply of alcoholic liquor for human consumption. It is worth noting here that the word used is supply and not sales, hence consideration is not required for supply. Definition of supply:The term supply has been defined in an inclusive manner under clause 3 of the revised Model GST Law. The definition goes as follows: (1) Supply includes— (a) all forms of supply of goods and/or services such as sale, transfer, barter, exchange, license, rental, lease or disposal made or agreed to be made for a consideration by a person in the course or furtherance of business, (b) importation of services, for a consideration whether or not in the course or furtherance of business, and (c) a supply specified in Schedule I, made or agreed to be made without a consideration. (2) Schedule II, in respect of matters mentioned therein, shall apply for determining what is, or is to be treated as a supply of goods or a supply of services. (3) Notwithstanding anything contained in sub-section (1), (a) activities or transactions specified in schedule III; or (b) activities or transactions undertaken by the Central Government, a State Government or any local authority in which they are engaged as public authorities as specified in Schedule IV, shall be treated neither as a supply of goods nor a supply of services. (4) Subject to sub-section (2) and sub-section (3), the Central or a State Government may, upon recommendation of the Council, specify, by notification, the transactions that are to be treated as— (a) a supply of goods and not as a supply of services; or (b) a supply of services and not as a supply of goods; or (c) neither a supply of goods nor a supply of services. (5) The tax liability on a composite or a mixed supply shall be determined in the following manner — (a) a composite supply comprising two or more supplies, one of which is a principal supply, shall be treated as a supply of such principal supply; (b) a mixed supply comprising two or more supplies shall be treated as supply of that particular supply which attracts the highest rate of tax. Inclusive defintion of supply: From the above clause 3 it is clear that the term supply has not been defined exhaustively rather it has been defined in an inclusive manner. It must be remembered that when the word “includes” is used in the definition, the legislature does not intend to restrict the definition. it makes the definition enumerative but not exhaustive. That is to say, the term defined will retain its ordinary meaning but its scope would be extended to bring within it matters, which in its ordinary meaning may or may not comprise. Thus the term supply would include within its ambit not only the matters covered under clause 3 but also other matters which may be included by natural import. Supply includes all forms of supply of goods and/or services such as sale, transfer, barter, exchange, licence, rental , lease or disposal made or agreed to be made for a consideration by a person in the cource or furtherance of business. The important thing to be noted here is the use of word consideration and in the cource or furtherance of business. However, certain matters have also been termed as supply even without consideration as mentioned under schedule I of the Revised Model GST law. Such transactions are: (a) permanent transfer/disposal of business assets where input tax credit has been availed on such assets. (b) Supply of goods or services between related persons, or between distinct persons as specified in section 10, when made in the cource or furtherance of business. (c) Supply of goods by principal to agent(Branch Transfers). Supply of goods by agent to principal (cases of inter-state purchases covered), Scope of SC judgement in Bakhtawar Lal Kailash Chand Areti curtailed. Import of service: Supply also includes specifically the import of service for a consideration whether or not in the cource or furtherance of business. However, Import of services by a taxable person from related person or from any of his other establishments outside India, in the cource or furtherance of business has been made taxable even without consideration. Supply of goods vs Supply of services: Further certain matters have been seperately explained to be treated as supply of goods and certain to be supply of services under schedule II of the Model GST Law. This has been done considering the past litigations on the issue of double taxation like in works contract AC restaurants, intangible goods, transfer of right to use goods etc. . Matters to be treated as goods: (a) Any transfer of title in goods (b) Any transfer of title in future goods undre an agreement (hire purchase) (c) Transfer of goods forming part of assets on the directions of a person carrying on business, in such a way so as not to form part of business assets with or without consideration (d) Goods forming part of business assets on ceasing to be a taxble person except when business is transferred as going concern to another person or business is carried on by a personal representative deemned to be a taxable person. (e) Supply of goods by any unincorporated association to a member thereof for cash, deferred payment or other valuable consideration(Concept of mutuality seem to be covered as well). . Matters to be treated as supply of services: (a) Any transfer of right in goods or undivided share in goods(transfer of right to use is a service) (b) Any lease, tenancy, easement, licence to occupy land, lease or letting out of building including commercial, industrial or residential complex (renting of immovable property is supply of service) (c) Job work on other’s goods (d) Business goods put to private use or making available to any person for non-commercial purpose (e) Renting of immovable property (f) Construction of a commercial complex, building, civil structure or a part thereof, including a complex or building intended for sale to a buyer, wholly or partly, except where the entire consideration has been received after issuance of completion certificate, where required, by the competent authority or before its first occupation, whichever is earlier (g) Transfer of IPRs (h) development, design, programming, customisation, adaptation, upgradation, enhancement, implementation of information technology software; (i) agreeing to the obligation to refrain from an act, or to tolerate an act or a situation, or to do an act; (j) works contract including transfer of property in goods (whether as goods or in some other form) involved in the execution of a works contract; (k) transfer of the right to use any goods for any purpose (whether or not for a specified period) for cash, deferred payment or other valuable consideration; (l) supply, by way of or as part of any service or in any other manner whatsoever, of goods, being food or any other article for human consumption or any drink (other than alcoholic liquor for human consumption), where such supply or service is for cash, deferred payment or other valuable consideration.(restaurant service). . There are certain activities which shall be neither service of goods nor supply of services, such transactions are mentioned under schedule III.

(b) The duties performed by any person who holds any post in pursuance of the provisions of the Constitution in that capacity; or (c) The duties performed by any person as a Chairperson or a Member or a Director in a body established by the Central Government or a State Government or local authority and who is not deemed as an employee before the commencement of this clause.

. Similarly certain activites undertaken by Central or State Government or any local authority as specified in schedule IV shall be neither supply of services nor of goods. Schedule IV provides exhaustive list of activities such as issuance of passport, visa, driving licence, birth and death certificates etc. Apart from abovce section 3(4) provides that the central or state government may on recommendation of GST Council, specify by notification, the transactions that are to be treated as- (a) a supply of goods and not as a supply of services; or (b) a supply of services and not as a supply of goods; or (c) neither a supply of goods nor a supply of services. . Taxability of Mixed and composite supplies: Revised Model GST Law has also provided under clause 3(5) provisions for taxability of composite and mixed supplies as follows: (a) a composite supply comprising two or more supplies, one of which is a principal sully, shall be treated as a supply of such principal supply. Example Supply of food during the course of transportation of passengers by air services shall be treated as supply of transportation of passengers by air. (b) a mixed supply two or more supplies shall be treated as supply of that particular supply which attracts the highest rate of tax. |

||||||||||||||||||||||||||||||||||||||||||||||

|

Job work under Revised GST Law if Job worker add his own material Posted: 22 Jan 2017 01:10 AM PST Job work under Revised GST Law if Job worker add his own material.  . Sec.55 of Revised GST Act lays down the procedure for removal of goods for job work. It states that a registered taxable person may, under intimation and subject to conditions as may be prescribed, send any inputs and/or capital goods, without payment of tax, to a job worker for job-work. Thus essential conditions to be satisfied to be covered under provisions of Sec.55 are:

As far as understanding / complying with condition no 1 is concerned it is a simple proposition. However, ones need to understand the meaning of job – work & Job worker respectively. Sec.2(61) defines the term “ Job Work” to mean undertaking any treatment or process by a person on goods belonging to another registered taxable person and the expression “ job worker “ will be construed accordingly. This definition raises following questions which are required to be answered before we conclude that activity of sending inputs/capital goods amounts to job work:

In a majority of job work transactions, job worker adds his own material – content of such usage differing in case to case within & across industries. In the case of Prestige Engineering India Ltd. v CCE, Meerut – 1994(9) TMI 66, Supreme Court stated that where job worker contributed his own material to the goods supplied by the customer and was engaged manufacturing, the activity was not one of job work. Minor additions would not take away the fact that the activity was one of job work. Thus one needs to carefully analyse the factual matrix under which the transactions are undertaken before a conclusion can be drawn. If based on facts of the case if one comes to the conclusion that the proposed activity cannot be covered under job work, the benefit of Sec.55 will not be available. The transaction would be considered as supply and attract relevant tax. |

||||||||||||||||||||||||||||||||||||||||||||||

|

TAX DEDUCTED AT SOURCE As per Revised Model GST Law Posted: 22 Jan 2017 12:56 AM PST TAX DEDUCTED AT SOURCE As per Revised Model GST Law.  . Synopsis

. 1.1 Deductor Sec. 46(1) Notwithstanding anything contained to the contrary in this Act, the Central or a State Government MAY mandate, – [Deductor] (a) A department or establishment of the Central or State Government, or (b) Local authority, or (c) Governmental agencies, or (d) Such persons or category of persons as may be notified, by the Central or a State Government on the recommendations of the Council, 1.2 Rate of TDS? Tax should be deducted at the rate of 1% from the payment made or credited to the supplier [hereinafter referred to in this section as “the deductee” of taxable goods and/or services,notified by the Central or a State Government on the recommendations of the Council. 1.3 When TDS is required to be made? Where the total value of such supply, under a contract, exceeds five lakh rupees. Explanation. – For the purpose of deduction of tax specified above, the value of supply shall be taken as the amount excluding the tax indicated in the invoice. Q.1 Mr. A enters into the following contract with Mr. B in the month of April, Nov. and Dec. of Rs. 5 Lacs, Rs. 5 Lacs and Rs. 5 Lacs in total aggregating Rs. 15 Lacs. Whether A is liable for TDS? Ans: Section 46 of the proposed model GST Law if read along with the Sec. 194C of the Income Tax Act, then it is clear that aggregate of the amount of contract will be considered if entered with a single person. Since in the given case aggregate amount in a financial year exceeds Rs. 5 Lacs i.e. 15 Lacs. TDS provisions will be applicable on entire 15 Lacs i.e. 15*1%=Rs. 15000/-. Q.2 In the above case if Mr. A enters into a contract with Mr. B of Rs. 5 Lacs, Mr. C of Rs. 5 Lacs and with Mr. C of Rs. 5 lacs in total aggregating to Rs. 15 Lacs? Whether A is liable for TDS? Ans: In the given since Mr. A enters individual contract with different persons, hence limit is to be seen for each contract separately. Since the amount in each contract do not exceeds Rs. 5 Lacs hence no liability of TDS would arrive in the given case. Q.3 Mr. A total value of supply under a contract including tax of Rs. 10,000/- is Rs. 5,10,000/-? Whether TDS Liability in such case will arise? Ans: TDS Liability will arise only if total value of a supply excluding the Tax under a contract exceeds Rs. 5 Lacs. Since in the given case excluding the tax element total value of supply is only Rs. 5 lacs hence no liability of TDS will arise in the given case. Q.4 Mr. A total value of supply under a contract excluding tax of Rs. 10,000/- is Rs. 5,10,000/-? Whether TDS Liability in such case will arise? Ans: TDS Liability will arise only if total value of a supply excluding the Tax under a contract exceeds Rs. 5 Lacs. Since in the given case excluding the tax element total value of supply exceeds Rs. 5 lacs i.e. Rs. 5,10,000/- hence liability of TDS will arise in the given case. . 1.4 When TDS should be paid to the account of appropriate government? As per sub section (2) of section 46 the amount deducted as tax under this section shall be paid to the account of the appropriate Government by the deductor within ten days after the end of the month in which such deduction is made, in the manner prescribed. 1.5 Details to be furnished in TDS Certificate? As per sub section (3) of section 46, the deductor shall, in the manner prescribed, furnish to the deductee a certificate mentioning therein the contract value, rate of deduction, amount deducted, amount paid to the appropriate Government and such particulars as may be prescribed in this behalf. 1.6 When TDS certificate to be furnished by deductor? As per sub section (4) of section 46, the deductor should furnish to the deductee the certificate, after deducting the tax at source, within five days of crediting the amount so deducted to the appropriate Government. 1.7 Failure to furnish TDS certificate within due date and penal provisions? As per sub section (4) of section 46, if any deductor fails to furnish to the deductee the certificate, after deducting the tax at source, within five days of crediting the amount so deducted to the appropriate Government, the deductor shall be liable to pay, by way of a late fee, a sum of one hundred rupees per day from the day after the expiry of the five day period until the failure is rectified: PROVIDED that the amount of fee payable under this sub-section shall not exceed five thousand rupees. . Q.5 Mr.A, deductor have deducted TDS for the month of June and deposited to the credit of government on 15th July? He issued the TDS certificate on 18th July? Whether he liable for to pay late fees or interest or both? Ans: TDS certificate should be issued within 5 days of crediting the amount so deducted to the appropriate government, since in the given case the amount is credited on 15th July and the certificate is issued on 18th July hence no Liability of late fees is going to arise,but since the amount is not deposited within the due date i.e 10th July Hence the liability of interest will arise.( Interest rate not yet specified). Q.6 Mr.A, deductor have deducted TDS for the month of June and deposited to the credit of government on 15th July? He issued the TDS certificate on 21st July? Whether he liable for to pay late fees or interest or both? Ans: TDS certificate should be issued within 5 days of crediting the amount so deducted to the appropriate government, since in the given case the amount is credited on 15th July and the certificate is issued on 28th July hence Liability of late fees is going to arise i.e. Rs. 100/- since the delay is by one day only, but since the amount is not deposited within the due date i.e 10th July Hence the liability of interest will arise.( Interest rate not yet specified). . 1.8 When deductee can claim TDS credit? As per sub section (5) of section 46, the deductee shall claim credit, in his electronic cash ledger, of the tax deducted and reflected in the return of the deductor furnished under sub-section (3) of section 34, in the manner prescribed. 1.9 What if the deductor fails to deposit the tax deducted within due date? As per sub section (6) of section 46, if any deductor fails to pay to the account of the appropriate Government the amount deducted as tax under sub-section (1), he shall be liable to pay interest in accordance with the provisions of sub-section (1) of section 45, in addition to the amount of tax deducted. 1.10 How to determine the amount in default under this section? As per sub section (7) of section 46, determination of the amount in default under this section shall be made in the manner specified in section 66 or 67, as the case may be. 1.11 Refund to the deductor or deductee on account of excess or erroneous deduction? As per sub section (8) of section 46,refund to the deductor or the deductee, as the case may be, arising on account of excess or erroneous deduction shall be dealt with in accordance with the provisions of section 48. Provided that no refund to deductor shall be granted if the amount deducted has been credited to the electronic cash ledger of the deductee. . Disclaimer: The contents of this document are solely for informational purpose. While due care has been taken in preparing the above article, possibility of any errors and omissions cannot be ruled out. Moreover, the views expressed herein above are solely author’s personal views. No part of it should be copied or reproduced without written or express permission of the Author. |

||||||||||||||||||||||||||||||||||||||||||||||

WELCOME TO CA GROUPS

CA GROUPS |

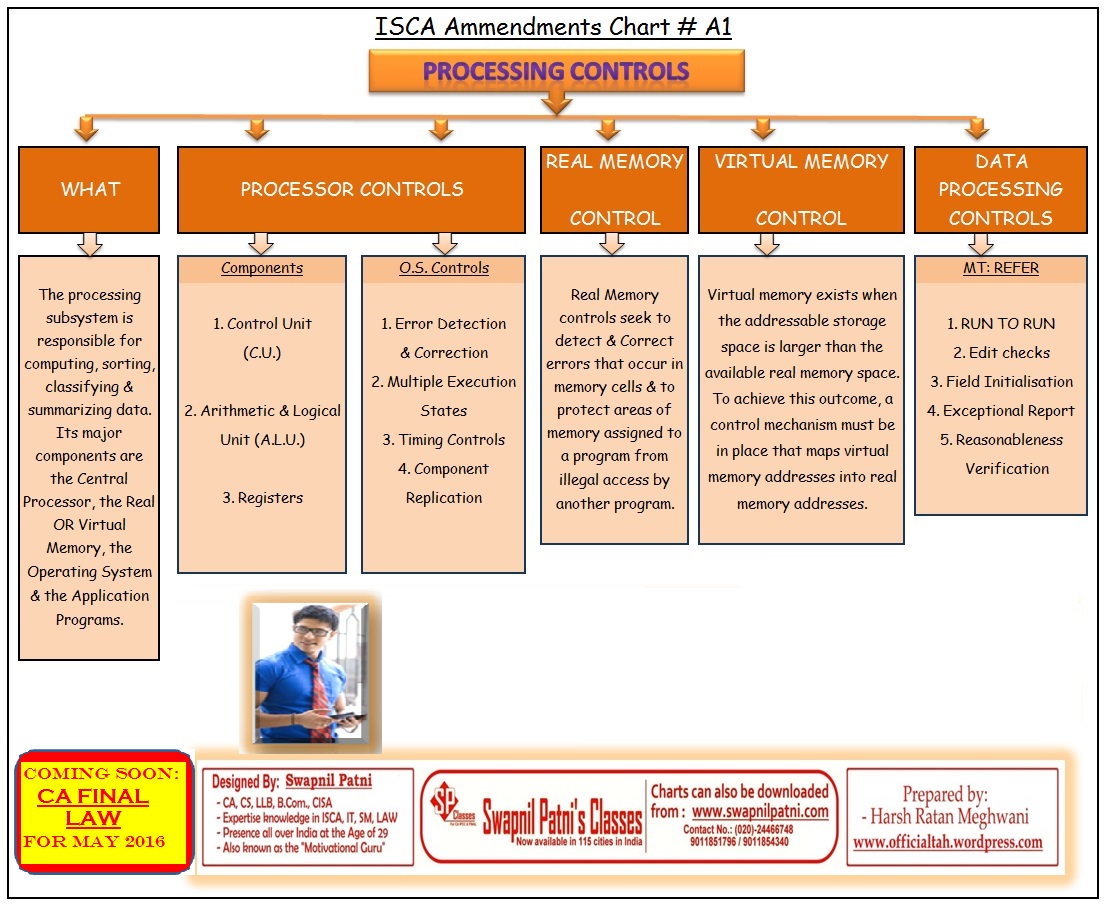

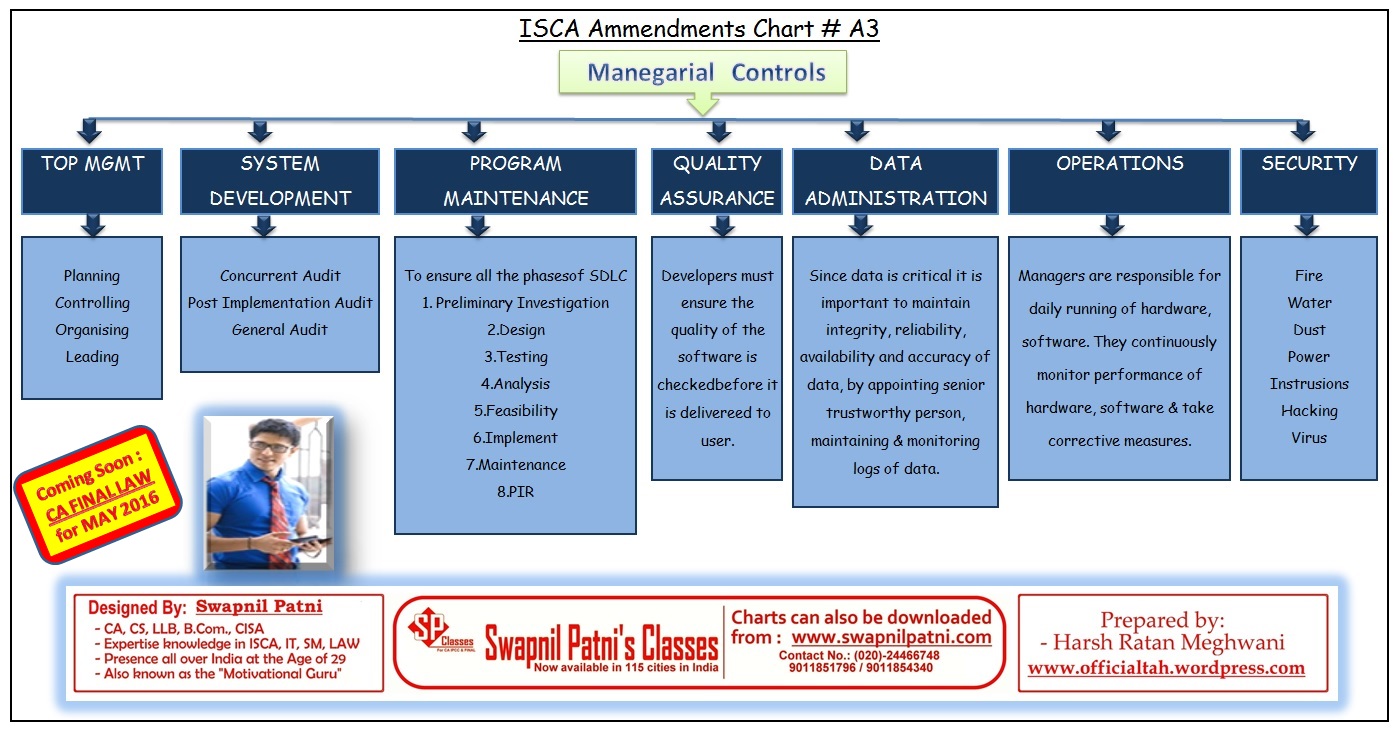

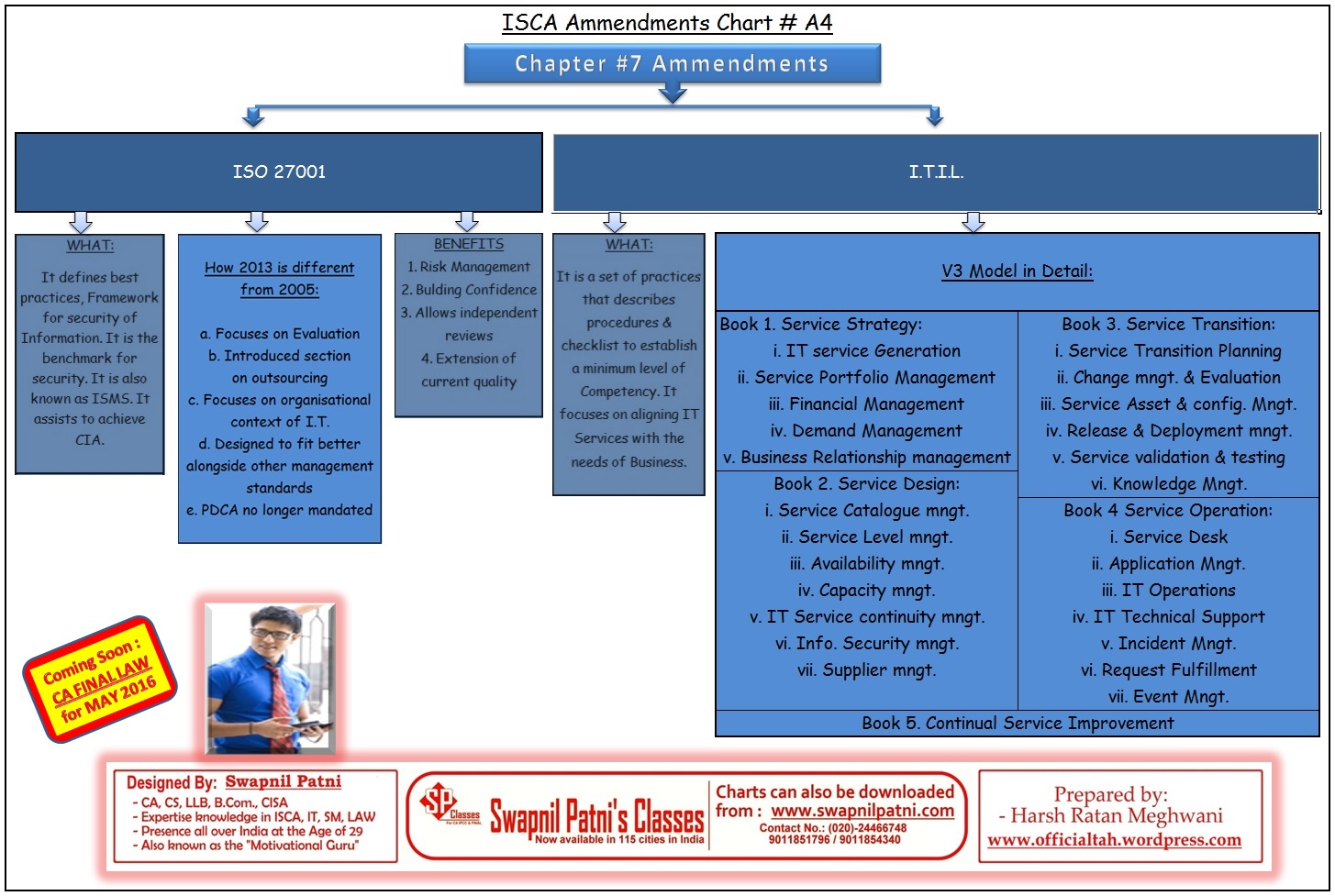

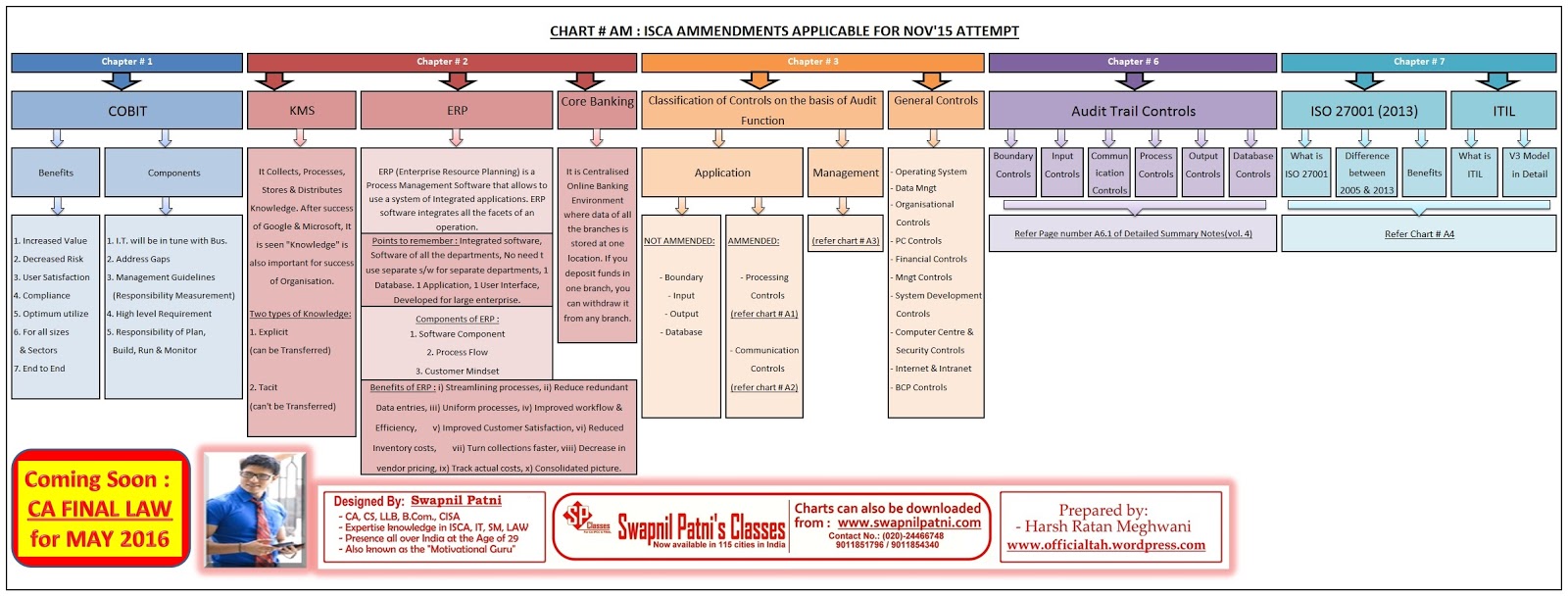

- CA Final ISCA Amendment charts by Swapnil Patni

- Increase In CA IPCC and CA Final Examination Fees

- CS EXECUTIVE PROFESSIONAL DEC 16 RESULT DATE

- ISCA/ITSM me Pass Hone ki Keemat Tum Kya Jaano Ramesh Babu

|

CA Final ISCA Amendment charts by Swapnil Patni Posted: 27 Jan 2017 08:11 AM PST CA Final ISCA Amendment charts by Swapnil Patni. So with every passing days CA Exams comes nearer and most difficult to pass exams in CA Final is ISCA. If you don’t agree with us then must read once this article on our Website ISCA/ITSM me Pass Hone ki Keemat Tum Kya Jaano Ramesh Babu, Coming back to this post today we brings you Amendment charts for CA Final ISCA which are provided by one and only renowned teacher Swapnil Patni who taught more than 15000 students in a very short span of 5 yrs and produced many rankholder till now you can simply download these charts by clicking on below links Recommended read :- TIPS TO STUDY CA Final ISCA     Also Read :-Hope you will like them and share with your friends, we will share more such notes with you in future as well so keep visiting CA GROUPS for all the latest updates and notes on CA Course |

||||||||||||||||

|

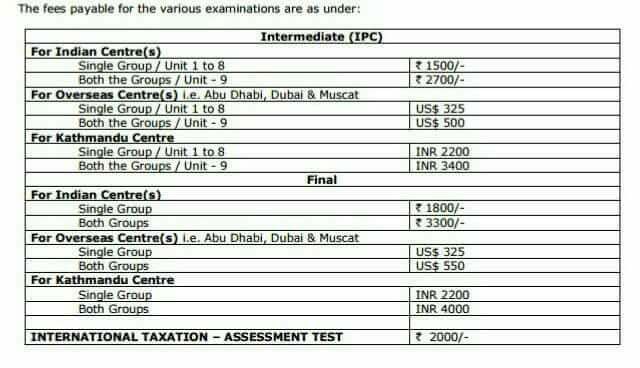

Increase In CA IPCC and CA Final Examination Fees Posted: 27 Jan 2017 06:46 AM PST Increase In CA IPCC and CA Final Examination Fees. Just after CA Final Results ICAI announced date from when ICAI Exam forms for may 17 Exams will be available and to the surprise ICAI has increased the examination fees from May 17 exams. Applications for admission to CA IPCC and CA Final examinations are required to apply online at http://icaiexam.icai.org which begins from 6th February, 2017 to 27th February, 2017 and submit the examination fee online by using either VISA or MASTER Credit / Debit Card( Amex cards will not be accepted) . They can by paying additional ` INR 600/- towards late fee (for Domestic & Kathmandu centres) and US$ 10 (for Overseas centres) if application made online after 27th February, 2017 and before 6th March, 2017. Student Please note that sale & submission examination application form at ICAI branches has been discontinued w.e.f. May 2017 examinations onwards. Now Again to Increase In CA IPCC and CA Final Examination Fees below are the revised rates of CA IPCC and Final Examination fees from May 17 CA Exams Must Read :-CA Eti Agarwal CA rankholder Interview by CA Surbhi bansal , CA Parveen Sharma and CA Raj kumar . Increase In CA IPCC and CA Final Examination Fees

In CA IPCC and CA Final Examination Fees You can clearly see a rise of approx. 25% Fees in fees. One reason of increase in fees could be the increase in cost to organise CA Exams as fees has been not revised for almost 7-8 years. Fees for Centres outside india has also been Increased in same proportion. Please comment your views regarding this rise in CA IPCC and CA Final Examination Fees. Are you ok with it or not ? do comment below your views on this and keep visiting CA GROUPS for more updates and notes on CA Exams |

||||||||||||||||

|

CS EXECUTIVE PROFESSIONAL DEC 16 RESULT DATE Posted: 27 Jan 2017 07:02 AM PST CS EXECUTIVE PROFESSIONAL DEC 16 RESULT DATE . Hey guys CS exams has been completed in DEC 2016 and its time to see the results of all of your hard work and passion regarding your profession. Team CA GROUPS hearty wishes for your better result and your better result. In this post we are gonna provide you the Result date for declaration of result of CS Foundation, CS Executive and CS Professional. Recommended:- Download All Company Forms at one place ICSI has a specialty of declaring result on the same day each year for June and December Examination. So there is no doubt on the expectation of result date other than the below mentioned. CS EXECUTIVE PROFESSIONAL DEC 16 RESULT DATE

To check the result you have to go on http://icsi.examresults.net CS EXECUTIVE PROFESSIONAL DEC 16 RESULT GET YOUR CS EXAMINATION RESULTS ON MOBILE – SMS! Foundation ICSIFOUN<space>ROLL NUMBER – Send it to 56263 Executive ICSIEXEC<space>ROLL NUMBER – Send it to 56263 Professional ICSIPROF<space>ROLL NUMBER – Send it to 56263 . You may also read this:- |

||||||||||||||||

|

ISCA/ITSM me Pass Hone ki Keemat Tum Kya Jaano Ramesh Babu Posted: 27 Jan 2017 08:00 AM PST ISCA/ITSM me Pass Hone ki Keemat Tum Kya Jaano Ramesh Babu Most of the CA Students has faced difficulty in passing examination in ITSM in CA IPCC & ISCA in CA Final. This is the paper which can decide the fate of the students for Rank Holders. Here is the most unfortunate student of all time in the history of the chartered accountancy course. In May 2016 examination a student named Amrit Vadhan has scored more than 70 marks in all the subjects except in case of ITSM. He has scored exemption in all the exams but in case of ITSM he did not score good marks and failed 6 marks. The detailed marks Mark Sheet of the Amrit Vadhan is as follows:

IT SM is considered as the most difficult subject of CA IPCC. To make this easy piizy we have some articles just for you. You must have a look on the below mentioned articles. |

WELCOME TO CA GROUPS

CA GROUPS |

|

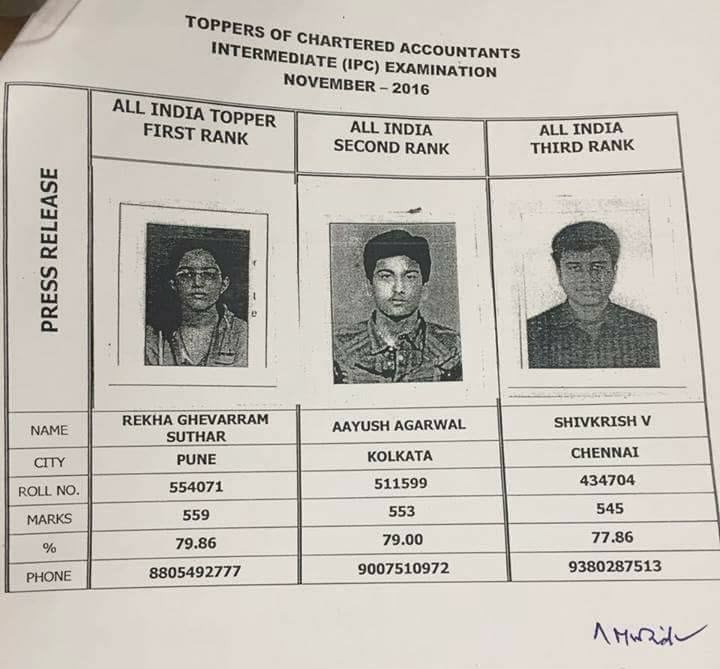

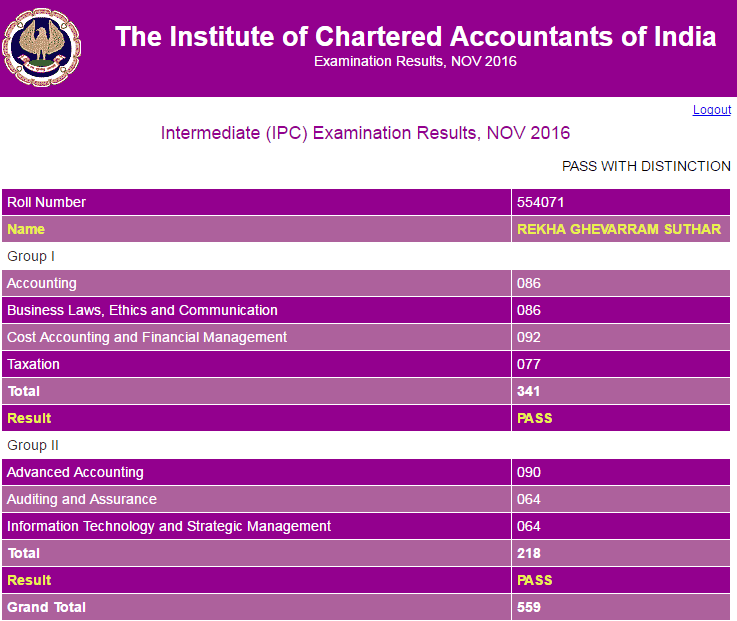

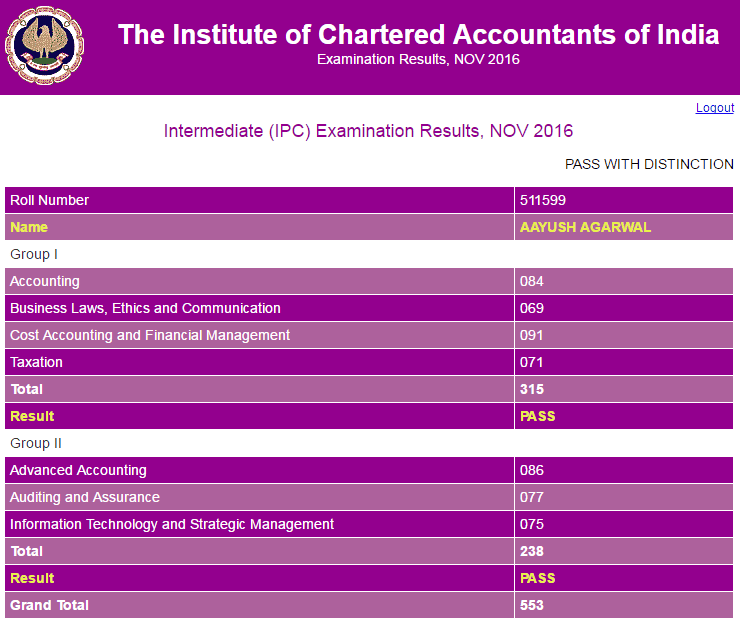

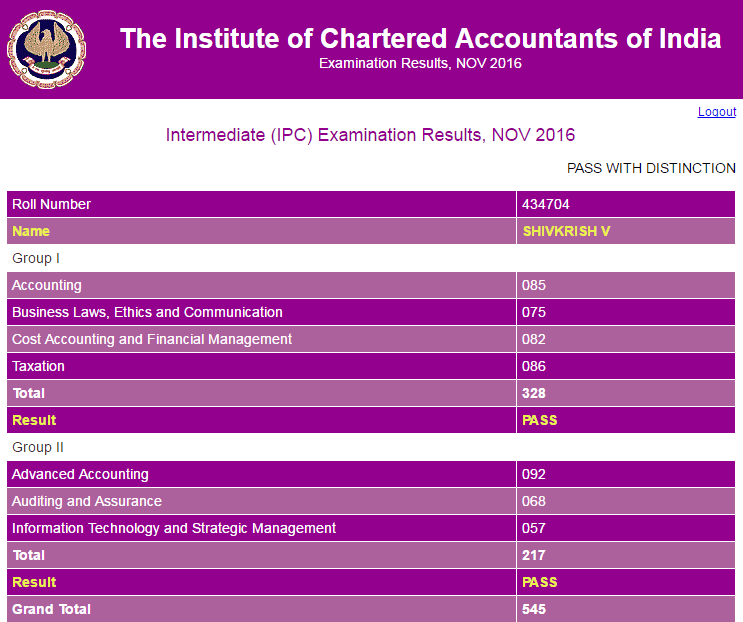

CA IPCC Topper Nov 2016 – Mark sheet, Interview, photos Posted: 31 Jan 2017 08:43 AM PST CA IPCC Topper Nov 2016 – Mark sheet, Interview, photos. CA IPCC Nov 16 exams result has just announced and we have arranged you the details regarding the CA IPCC topper Nov 16 , their mark sheets, interview, photos and many more. Just after declaring the result of CA IPCC Nov 16 ICAI has issued the name of CA IPCC Topper Nov 16. The best thing about the CA IPCC Result is that we have 3 more inspirations for our next attempt. These three inspiration are three rank holders of Nov 16. . The name, mark sheet, Interview and photos of CA IPCC Topper Nov 2016 are as follows: – Pass percentage of CA IPCC Nov 2016 EXAM

Rank Holder of CA IPCC Nov 2016 EXAM

|

|

.  . Now below are the IPCC Topper Mark Sheet for Nov 2016

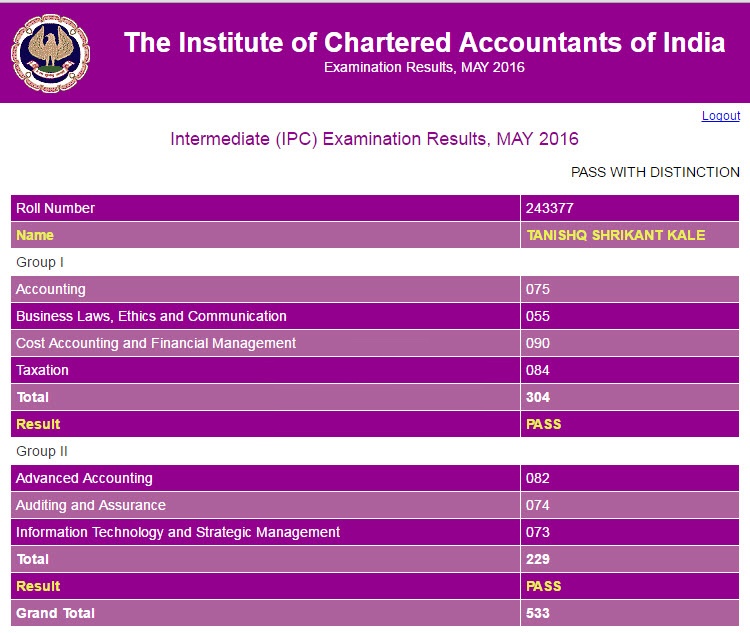

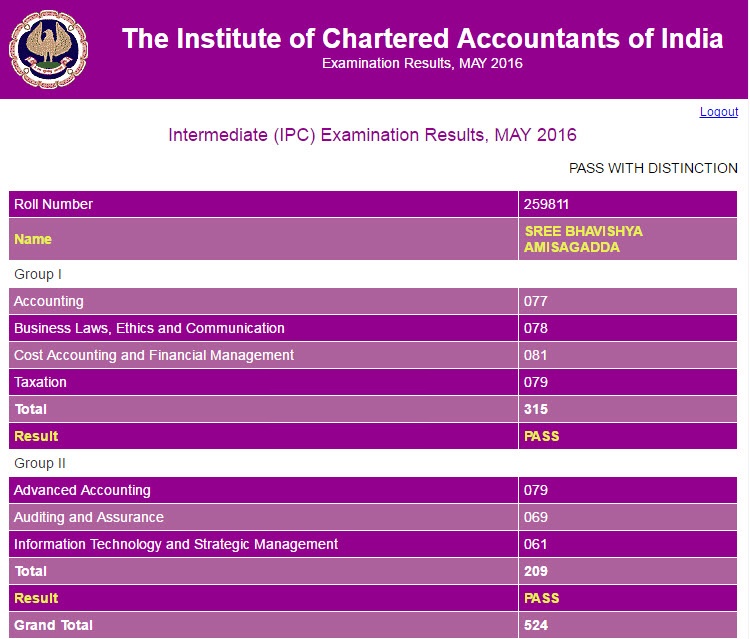

The name, mark sheet, Interview and photos of IPCC Topper May 2016 are as follows: – Pass percentage of IPCC May 2016 EXAM Both group —— 4.78% Group I —- 9.18% Group II —- 7.06%  Now below are the IPCC Topper Mark Sheet for May 2016

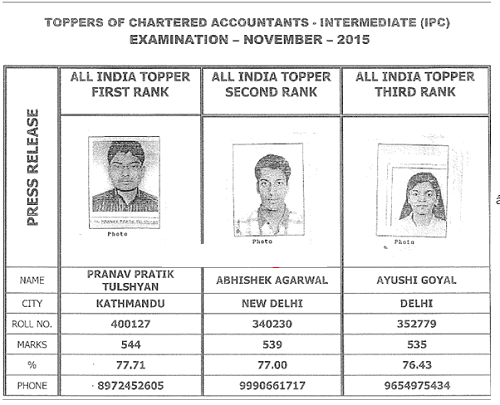

The name, mark sheet, Interview and photos of CA IPCC Topper Nov 2015 are as follows: – Pass percentage of IPCC NOV 2015 EXAM Both group 4.14% Group I 12.72% Group II 10/69%  .

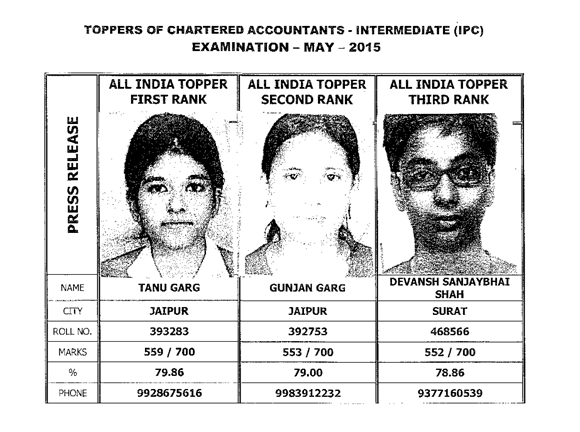

. CA IPCC Topper For May 2015 are given below for kind reference  . CA IPCC Topper For NOV 2014 are given below for kind reference  . CA IPCC Topper For May 2014 are given below for kind reference  . CA IPCC Topper For NOV 2013 are given below for kind reference  . The most common things between CA IPCC Topper interview are given below: –

|

WELCOME TO CA GROUPS

CA GROUPS |

- Clarification Regarding Income Tax Slab Rate: Budget 2017

- Union Budget 2017: Highlights

- Income Tax Rate Chart for Financial Year 2017-18

- Union Budget 2017 Live Updates

|

Clarification Regarding Income Tax Slab Rate: Budget 2017 Posted: 01 Feb 2017 06:07 AM PST Clarification Regarding Income Tax Slab Rate: Budget 2017. Many People are getting Confused that Individual Income Tax Slab Rate is Changed to 3L from 2.5L. I would like to clarify on this Point that there is No change in Slab Rates. Only Rate of Tax is Changed from 10% to 5% from those people whose Taxable Income is less than 5L. Considering the Benefit of Rebate u/s 87A (upto Rs 2500) Also; If Anyone Earning Income Upto 3L then his Total Tax Liability will be Zero. *For Example* Taxable Income : 3L/- Tax @5% Above 2.5L 2500/- Less : Rebate u/s 87A 2500/- Net Tax Payable - 0/- Please Create Awareness and Don't believe on Rumours. RegardsSOURAV BAGARIA |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Posted: 01 Feb 2017 06:02 AM PST Union Budget 2017: Highlights.

Highlights of UNION BUDGET 2017 Given Below-- |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Income Tax Rate Chart for Financial Year 2017-18 Posted: 01 Feb 2017 05:50 AM PST Income Tax Rate Chart for Financial Year 2017-18 .

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Union Budget 2017 Live Updates Posted: 01 Feb 2017 05:02 AM PST Union Budget 2017 Live Updates.  Finance Minister to Announce Finance Budget from 11:00 AM. Get Live Updates from Here. Finance minister Arun Jaitley is likely to boost spending and ease back on cutting the deficit with the Union budget on Wednesday, as he seeks to lift growth hit by the government’s drive to scrap high-value banknotes in November last year. The finance minister was expected to present the annual federal budget despite the death of a sitting member of parliament, E Ahamed, an official said on condition of anonymity. Parliament typically adjourns for a day after the death of a member, although TV channels cited a precedent where the budget presentation had still gone ahead in a previous year. Press F5 to refresh the page & get Live Updates.Here are live updates on the Union Budget 2017/18: 13:10 (IST) Lok Sabha adjourned after Finance Minister Arun Jaitley concludes his Budget 2017 speech. ‘MSME corporate tax cut a big boost to entrepreneurship’ Reduction in corporate tax for SMEs and increased exemption of profits to 3/7 yrs a big boost to the small and 1st gen businessmen of the nation. 12.58 pm: No scrutiny on first-time taxpayers. 12.54 pm: — No tax on annual income of Rs 4.5 lakh who use rebates. — Net revenue foregone on income tax changes is Rs 12,800 crore. — Surcharge of 10% on annual income of Rs 50 lakh and above. —New Rate for 44Ad – 6% Government has finally moved one step forward in cleaning a corrupt and non-transparent system of political funding. This was a long-pending demand from the public at large. Though Prime Minister Modi had been talking about it for some time and Election Commission had made certain suggestions to the government, there was a great deal of scepticism on whether or when the Government would actually make a move in this regard. The popular pressure had grown after demonetisation. It was heartening to hear FM Jaitley talking of brining some amendments to take small but significant steps to cleanse political funding with the admission that political parties continue to accept through anonymous sources and donors fear to entail adverse consequences. The limit for anonymous cash donation has been brought down from Rs 20,000 to Rs 2,000. NO CHNAGE IN SERVICE TAX & EXCISE DUTY RATES DUE TO UPCOMING GST 5% TDS on Insurance Agents Removed 12:56 (IST) “No significant loss or gain due to budgetary proposals in the indirect taxation,” says Jaitley 12:52 (IST) Reduction of the existing rate of tax for low tax bracket individuals “Reduce existing rate for income from Rs 2.5 lakh to 5 lakh to 5 % from 10%. 50% saving in income tax if a person is earning up to Rs 5 lakh,” says Jaitley. Income Tax limit for individuals – 2.5 Lacs – 5 lacs – Now 5% from earlier 10% 12:49 (IST) NO TRANSACTION OVER RS. 3 LAKH WILL BE PERMITTED IN CASH 12:48 (IST) Donation to political parties, no more than Rs 2,000 in cash “Up to Rs 2,000 can be donated in cash by anyone source to a political party. Political parties can receive donations through digital methods and cheques. Donors can buy RBI bonds and would be able to donate to a political party which can redeem within a specified time. The bond can be bought through cheque or by employing any digital method. Every political party has to file its returns as per Income Tax Act,” says Jaitley. — Limit of Rs 2000 on cash donations to charities. SIT suggests and government has accepted that cash transaction not to be allowed above Rs 3 lakh. — Basic customs reduced from 5% to 2.5% on LNG terminals. — Rs 7,200 crore revenue will be foregone on account of tax rebate to MSME. — Income tax for small companies with an annual turn over of 50 crore, now to pay 25%, a 5% reduction. –To make MSME companies more viable to pay 25% tax if turnover is up to Rs 50 crore. –Startups to pay tax on profits for three out of seven years, increased from three out of five years. –-Carry forward of MAT allowed for 15 years 12:42 (IST) Capital gains tax for housing “Propose to make changes in capital gains tax for housing. Holding period for land and building will be reduced to 2 years from 3 years. Instead of build-up area, carpet area will be counted for affordable housing,” says Jailtley. 12:40 (IST) PM Fasal Bima Yojana: Who is the government insuring exactly — farmers or companies? Government expenditure has increased substantially from Rs 5,500 crore proposed last year to Rs 13,200. But it seems to have gone in the pocket of private insurance companies. Share of farmers covered has increased from 21% to only 24%. Sum assured has gone up, not the numbers of farmers covered, nor the claim amount. Who is the government insuring exactly: farmers or companies? 12:39 Tax cut for smaller firms “Propose to cut 5% tax for those firms whose turnovers are below Rs 50 crore. 96% firms of the country would be benefitted,” says Jaitley. 12:36 (IST) ‘New law to confiscate absconders’ overseas properties; need to see the details’ A new law proposed to enable lenders to confiscate assets of absconders living overseas. But existing laws permitted this. Remains to be seen how this new law is drafted and implemented. Funds for banks at Rs 10,000 cr: Another year of disappointment? Arun Jaitley said government will infuse Rs 10,000 crore this year in public sector banks, which constitute 70 percent of the industry. This is part of the ‘Indradhanush’ plan to infuse Rs 70,000 crore in PSU banks over five years. Given the mess the banking sector is in, the kind of bad loan problems, analysts were expecting much bigger capital infusion to equip public sector banks, beyond what is already planned. Though the FM has assured that government will make sure banks get additional capital, past evidence shows that capital is yet again going to be a major problem for the sarakari banks. Consider this: Presently, state-run banks are severely undercapitalised. At least seven of the PSU banks have less than 8.5 percent Tier-I capital adequacy and one bank less than 8 percent. The problem is worsened with their non-performing assets (NPAs) hitting the roof (nearly Rs 6 lakh crore as on September, 2016 or nearly 8 percent of the total bank credit), and total chunk of stressed assets (bad loans and restructured loans together) jumping to 12-13 percent of the total bank credit. Jaitley should have allocated much more for weak state-run banks. Here, there is a bit of disappointment. 12:36 (IST) Post demonetisation deposits go up “Demonetisation deposits between Rs 2-80 lakh made In 1.09 crore accounts. Post demonetisation deposits above Rs 80 lakh in 1.48 lakh accounts,” says Jaitley. –Analysis after demonetisation present revealing picture. — We are largely a tax non-compliant country. Burden of those who evade taxes falls on the honest. — 24 lakh people show income above Rs 10 lakh. 12:33 (IST) Phasing out of FIPB and the extra push for FDI clears the murk and sends positive signal to foreign companies to invest in India: Mehul Turakhia, Director Finance, Directi 12:32 (IST) The push towards e-transactions through BHIM and Aadhar enabled payments puts India at the cusp of a digital revolution. 12:32 (IST) Revenue deficit pegged at 1.9% of GDP 12:31 (IST) Tax proposal to help middle class “The thrust of my tax proposal in this Budget is to bring relief to the middle class, boost affordable housing, transparent political funding,” says Jaitley. 12:31 (IST) ‘Fiscal deficit roadmap consistent with promise; but need great effort’ With regard to fiscal deficit roadmap of 3 years, a long-term view has been maintained. This is consistent with promises made. However, it would require great effort to achieve it. ‘Banking recap funds short of expectations’ Rs 10,000 crores for banks recapitalisation is in line, but short of expectations. 1.7 crore people file returns of 4.2 crore salaried people. Tax-GDP ratio “Tax-to-GDP ratio very low in India. We are largely a tax non-compliant society. When too many evades tax, the burden falls on those who are honest,” says Jaitley. 12:24 (IST) Fiscal deficit for 2017 at 3.2% “Total resources to be transferred to states and UTs estimated at Rs 4.11 lakh crore. Allocation of capital expenditure up 25% YoY. Peg fiscal deficit for 2017 at 3.2%,” says Jaitley. 12:21 (IST) Defence expenditure excluding pension at Rs 2.74 lakh crore. 12:20 (IST) Listing PSUs “Propose revised mechanism for time-bound listing of PSUs. Shift to digital platforms to benefit the common man,” says Jaitley. 12:18 New law to confiscate assets of those who flee country after crimes “New law to come up to confiscate the assets of those who flee the country including those who commit financial crimes to escape the reach of law. The law will have constitutional safeguards and the assets in India would stand confiscated until the person submits himself or herself to the law,” says Jaitley. 12:15 (IST) Centralised ticket booking system for defence personnel A centralised ticket booking system for defence personnel. They no longer have to stand in queues with warrants,” Jaitley said. 12:13 (IST) Payment Board to come up in RBI 12:12 (IST) IRCON, IRFC to be listed “IRCON and IRFC to be listed on stock exchanges. There is a proposal to create an integrated PSU oil major. Listing of CPSE will increase accountability,” says Jaitley. 12:09 (IST) The government to set-up new crude oil reserves. 12:08 (IST) Solar power gets more power “The government to take up second phase of solar power development for additional 20,000 MW. Over 250 proposals for electronics mfg received in last 2 yrs for Rs 1.26 lakh crore,” says Jaitley. 12:04 (IST) FDI policy “New FDI policy under consideration,” says Jaitley. 12:02 (IST) FIPB to be abolished. 12:00 Metro policy and highway allocation “New Metro Rail Policy to be announced. It will open up new job possibilities.National Highway Allocation fixed at Rs 64,000 Crore. Airports Authority of India Act to be amended to enable monetisation of land,” says Jaitley. 12 :00 Housing shares surge up to 11% after rise in housing allocation The finance minister said the government proposes to complete 1,00,00,000 houses by 2019 for houseless and those living in kaccha houses. Towards this, he increased allocation for PM Awas Yojana to Rs 23,000 crore.The shares of Ashiana Housing rose 11%, LIC Housing Fin 1.5%, Ganesh Housing 1.38% and Ansal Housing 10%. 12:00 (IST) Re-emphasis on cashless economy would boost digital transactions leading to greater financial inclusion, transparency and economic growth: Mehul Turakhia, Director Finance, Directi 11:57 (IST) Aadhaar card to have health details of senior citizens “A pilot project with Aadhaar cards containing the health details of senior citizens will be started in 15 districts,”says Jaitley. 11:56 Rail passenger safety gets importance “A Rail Raksha Sanraksha Koch with a corpus of Rs 1 lakh cr in the course of five years. Unmanned railway crossings to disappear by 2020. Railway lines of 3,500 km will be commissioned in 2017-18,” says Jaitley. “500 stations to be made differently-abled with lifts, escalators. Solar power to lit up more stations,” he said. “Coach Mitra facility to come up. All trains to have bio-toilets,” Jaitley said. “Service charge for tickets booked through IRCTC to be withdrawn. Tariffs to be fixed as per competition and quality of service,” said Jaitley. 11:55 (IST) Modi govt addresses its core social constituency Modi government has used the first half of the budget to address its core social constituency — farmers, rural poor, Dalits, women, youth. Remember, this is the third budget of the Modi government and thus most significant to send out a message to those who looked up to this government with certain hopes and aspirations. Farmers, rural poor, youth, girls and women, artisans, unprivileged and their concerns of education, infrastructure, loan, jobs and social security were dwelt at length. PM Modi and FM Jaitley realise the burden of expectation that is there on them and it was good to see that FM addressed to that in the beginning. 11:49 (IST) Two new AIIMS announced Gujarat, Jharkhand to get an AIIMS each 11:47 (IST) Affordable housing injected with more money “Allocation increased to Rs 23,000 crore. Banking loan rates coming down in the wake of demonetisation. Affordable housing to get infra status,” says Jaitley. 11:44 (IST) Special effort for farmers to double income to be focused on Eastern States. A hint for UP elections? MNREGA funds for asset creation, moving out of the old Dole regime. Housing allocation for rural housing grows 50 percent. The focus is on rural income and demand, and formalising rural economy. 11:43 (IST) New fund for secondary education: Jaitley “Innovation fund for secondary education to be created,” says Jaitley. 11:43 (IST) Modi govt’s political thrust apparent The political thrust of Modi government in union budget 2017 is clearly apparent from repeated reference to schemes beneficial to farmers, rural poor, infrastructure, dailts women, youth. Rs 10 lakh crore has been earmarked for credit to farmers in eastern Indian and Jammu and Kashmir. Mudra Yojna gets special mention. Funds for housing to rural poor under Prime Minister Rural Poor Housing scheme, allocation for MGNREGA has been increased to highest ever with the rider that it will be used to create productive assets. Mark the word eastern India, it had loaded political connotation without Uttar Pradesh word used. 11:42 (IST) Roads now made quicker “Pace of construction of roads has increased to Rs 133 km/day in 2017,” Says Jaitley. 11:37 (IST) Irrigation gets a boost “NABARD to set up dedicated micro irrigation fund worth Rs 5,000 cr. Focus will be on creating jobs.Long-term Irrigation Fund Set Up In NABARD, Additional Corpus Rs 20,000 crore,” says Jaitley. 11:34 (IST) Agriculture credit increase a good step: Aneja Increase in agriculture credit and its disbursal along with more coverage of crop insurance scheme is a good step and will be helpful to the farm sector hit by the demonetisation of Rs 500 and Rs 1,000 notes. 11:32 (IST) Policy moves from favouritism to transparency Use of Spring festival signals hope. Policy moves from favouritism to transparency and informal to formal. The finance minister is sending a macro message for foreign investors. 11:32 (IST) No demonestisation spill over next year: Jaitley Not seeing effects of the demonetisation spill over to next year, The effects of demonetisation not expected to spill over to the next year, says the finance minister. However, this goes against the indication in the Economic Survey that was released yesterday. The survey had given a GDP growth projection of 6.75-7.5 pecent for the next year. Experts have been of the opinion that the wide range could be an indication that there could be a spill over effect next year too. 11:30 (IST) Not seeing effects of the demonetisation spill over to next year The effects of demonetisation are not expected to spill over to the next year, says the finance minister. However, this goes against the indication in the Economic Survey that was released yesterday. The survey had given a GDP growth projection of 6.75-7.5 pecent for the next year. Experts have been of the opinion that the wide range could be an indication that there could be a spill over effect next year too. 11:30 (IST) Farmers to benefit from interest waiver: Jaitley “Farmers will benefit from 60-day interest waiver announced by the PM. Farm sector to grow 4.1% in the current fiscal. Fasal Bima Yojana to cover 40% of crop area,” said Jaitley. “Ä dedicated irrigation fund by NABARD for per drop more crop,” he said. 11:27 (IST) “A corpus of Rs 10 lakh cr has been fixed for farmers,” says Jaitley. 11:24 (IST) Surplus cash in the banking system will minimise borrowing: Jaitley “Surplus cash in the banking system will minimise borrowing,” says Jaitley. “Discontinued the 1924 British era policy. Brought railways to the fore. Done away with planned and non-planned allocations,”he said. 11:22 (IST) Spending more for underprivileged a target: Jaitley “My overall approach while preparing this Budget has been to spend more in rural areas, poverty alleviation through fiscal prudence,” says Jaitley. 11:20 (IST) Jaitley resorts to poetry, asks all to embrace the new. This of course celebrates the new thrust towards a cashless economy. 11:19 (IST) Lok Sabha Speaker Sumitra Mahajan’s summary dismissal of Congress parliamentary party leader in Lok Sabha Mallikarjun Kharge’s appeal to defer the budget session as mark of respect for death of Congress E Ahmed gave enough indication of the belligerence in the treasury benches in the budget session. Right from the word go, the government gave clear indication that it would not change the schedule of the budget in face of the Congress’s attempt to politicise the death of Ahmed. Given the established principle that the House is the master of its own business, Mahajan made it clear that the norms and precedents set in Parliament could be amended. In the government circles, the Congress’s persistence to defer the session was seen as continuum of their demand to postpone budget in view of the state assembly elections in Uttar Pradesh, Uttarakhand, Punjab and Manipur. 11:18 (IST) Demonetisation is the new normal: Jaitley “Demonetisation is the new normal. Demonetisation seeks to make our GDP bigger, cleaner.” says Jaitley. 11:17 (IST) India seen as an engine of global growth: Jaitley “According to the IMF, India is going to be the one of the fastest growing economies. Inflation has been controlled. The government has launched a massive war on black money. India seen as an engine of global growth,” says Jaitley. 11:15 (IST) CAD going going down: Jaitley “Growth in a number of emerging economies is likely to recover in 2017 after a poor performance in 2016. Uncertain crude oil prices have had its implication on the emerging economies,” says Jaitley. “India’s macroeconomic stability continues to be its fountainhead of its growth. CAD has declined by 1%,” says Jaitley. 11:12 (IST) Markets flat ahead of the start of parliament session At 11 am, the BSE Sensex was at 27691.65, up just 36.69 or 0.13%, and the Nifty 8568.15, up 6.85 points or 0.08%. Will the Budget be markets neutral? 11:11 (IST) Sluggish growth arrested: Jaitley Sluggish growth has been controlled.The government is seen as the trusted custodian of government money: Jaitley 11:10 (IST) Will textile, leather sectors get sops to push job creation? The Economic Survey may have dropped borad hints at how the governmenet may be planning to push job creation. “Apparel and Leather & Footwear sectors are eminently suitable for generating jobs that are formal and productive, providing bang-for-buck in terms of jobs created relative to investment and generating exports and growth,” said the survey released yesterday. The Survey adds that these sectors provide immense opportunities for creation of jobs for the weaker sections, especially for women, and can become vehicles for broader social transformation in the country. This could be a broad hint at the government’s plans for these sectors, which have large unorganised constituency. Though labour laws have been a major impediment in increasing investment in the sector and it is for the states to breing in reforms in this area now, the Centre could announce sops to boost the sectors. It is also to be remembered that textile was one of the sectors that was hit hard by the demonetisation of the Rs 500 and Rs 1,000 notes. 11:10 (IST) Finance Minister Arun Jaitley begins his fourth Union Budget speech. Wishes the country on the occasion of Vasant Panchami. 11:09 (IST) Uproar in Lok Sabha Opposition leaders are now shouting in the House even as Arun Jaitley begins to speak. 11.08 am: Finance minister Arun Jaitley begins budget speech. 11.07 am: Congress leader Mallikarjun Kharge says the House should be adjourned today and budget should be presented tomorrow. Speaker overrules him. 11.06 am: House will not sit tomorrow, says Lok Sabha Speaker Sumitra Mahajan. 11.03 am: Lok Sabha Speaker Sumitra Mahajan pays obituary to E Ahamed. 10.52 am: Budget has a sanctity, we are already in the eleventh hour. There should be no controversy over it. It’s a constitutional obligation: Union minister Venkaiah Naidu. 10.44 am: Saddened by E Ahamed ji’s death but budget will be presented: Sumitra Mahajan. 10.36 am: The budget will be presented today; it will be formally announced shortly. 10.32 am: Postponement of budget will be no big deal. It’s not as if the secrecy will break: HD Deve Gowda. 10.25 am: It’s neither possible nor correct: Subhash Kashyap, Constitution expert on postponement of budget after papers reach Parliament. 10.19 am: Finance minister Arun Jaitley tweets: “Watch me live presenting the Union Budget 2017 at 11 am, February 1, 2017 http://www.loksabhatv.nic.in/” 10.16 am: Prime Minister Narendra Modi arrives at E Ahamed ‘s residence. 10.14 am: It’s not March 31, there is a lot of time to present the budget. The government can postpone it: Congress leader Mallikarjun Kharge. 10.07 am: I think the government already knew that he (Ahamed) had passed away, but they were trying to maybe delay the announcement (of his death): Congress leader Mallikarjun Kharge. 10.07 am: In our opinion, including JDU leaders and former PM Deve Gowda, the budget should be postponed: Congress leader Mallikarjun Khadge. 10.03 am: Finance minister Arun Jaitley in Parliament. 10.02 am: Cabinet meeting to be held shortly in Parliament. 9.49 am: Lok Sabha Speaker Sumitra Mahajan to visit E Ahamed ‘s residence at 10 am. 9.47 am: Finance minister Arun Jaitley reaches Parliament. 9.28 am: Budget will be presented and Ahamed’s obituary may happen before or after it. The government has spoken to all parties and arrived at a consensus, an official source has told ANI. 9.10 am: Budget 2017 copies reach Parliament. Finance Minister Arun Jaitley is meeting President Pranab Mukherjee. 9.01 am: Final decision on Budget to be taken by Lok Sabha Speaker Sumitra Mahajan; decision expected by 10 am. 8.22 am: Normally, House is adjourned on death of a sitting MP, so chances are the Budget can be postponed for a day. But Speaker will decide: Santosh Gangwar. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

WELCOME TO CA GROUPS

CA GROUPS |

- Changes in Budget 2017 as Compared to Budget 2016

- Important Amendment in Income Tax, which FM did not cover in Budget Speech

- New Section 234F: Fee for Late filing of return of Income

- New section 271J: Penalty on professionals for furnishing incorrect information in statutory report or certificate

- Highlights of Finance Budget 2017 in Simple Language

|

Changes in Budget 2017 as Compared to Budget 2016 Posted: 02 Feb 2017 08:45 AM PST Changes in Budget 2017 as Compared to Budget 2016.  . 1-Turnover of companies upto 50 crore - tax will be 25% instead of 30% 2-MAT credit carry forward for 15 instead of 10 years 3-Long term capital gains on Property period reduced from 3 to 2 years 4- Base Year for indexation now 2001 instead of 1981 5- Presumptive tax for small traders with turnover upto 2 crore under 44Ad now 6% instead of 8 % for full non cash turnover 6- Cash expenditure now allowed only 10000 instead of 20000 per transaction 7- No transaction above 3 lac will be allowed in cash 8- Trust cash donations max allowed only 2000 instead of 10000 9- Political parties - max cash donations from 1 person Rs 2000. 10- Domestic transfer pricing - only if 1 party enjoys tax benefits 11- 44AD - turnover limit increased to 2 crores for business. 12- Professionals can pay advance tax in 1 installments if below 50 lac 13-Time for revising income tax return now reduced. 14- Scrutiny time limit reduced to 18 months 15- Individual tax reduced for income 2.5 to 5 lac tax rate now reduced to 5% 16- Surcharge of 10% on those who earn income from 50 lac to 1 crore 17- TDS - no Tds on insurance agents if 15 h filed 18- Simple 1 page income tax return for persons having non business income . 19- Deemed sale value for sale of unquoted shares introduced. To be taxed at fair value. Sec 50CA 20- In absence of PAN,the rate of TCS will be twice of the extent rate or 5%, whichever is higher. Sec.206CC. 21- If Return not filed as per Sec. 139 (1), concept of late fee introduced. Rs. 5000 for delay up to 31st Dec. and Rs. 10000 thereafter. Late fee to be paid before filing the Return. Sec 234F 22- CA issuing wrong certificate would be penalised with Rs. 10000 23- Capital gain on shares will be exempt only if STT was paid while purchasing the shares. 24- HP loss can be setoff against other head of income only to the extent of 200000 in same year. Balance loss can be c/f to 8 A.Ys. 25- Indl and HUF to deduct tds even if unaudited @ 5% if rent is paid 50000 pm 26- Tds in 194J amended, now 2 percent tds instead of 10 27- The scope of section 56 will be widened and will also cover any kind of gifts in cash or kind or for no consideration with few exemptions and exception 28- Disallowance of expenditure from income from other sources if tds is not deducted 29- Self employed can also claim 20% contribution to NPS as deduction. Regards SOURAV BAGARIA |

|

Important Amendment in Income Tax, which FM did not cover in Budget Speech Posted: 02 Feb 2017 08:39 AM PST Important Amendment in Income Tax, which FM did not cover in Budget Speech. 1) Deemed sale value for sale of unquoted shares introduced. To be taxed at fair value. Sec 50CA 2) In absence of PAN,the rate of TCS will be twice of the extent rate or 5%, whichever is higher. Sec.206CC. 3) New Section 269ST introduced whereby Rs three lakh in cash cannot be received on a single day or inrespect of single transaction. 4) If Return not filed as per Sec. 139 (1), concept of late fee introduced. Rs. 5000 for delay up to 31st Dec. and Rs. 10000 thereafter. Late fee to be paid before filing the Return. Sec 234F 5) CA issuing wrong certificate would be penalised with Rs. 10000 6) Capital gain on shares will be exempt only if STT was paid while purchasing the shares. 7) HP loss can be setoff against other head of income only to the extent of 200000 in same year. Balance loss can be c/f to 8 A.Ys.  Indl and HUF to deduct tds even if unaudited @ 5% if rent is paid 50000 Indl and HUF to deduct tds even if unaudited @ 5% if rent is paid 500009) Tds in 194J amended, now 2 percent tds instead of 10 10) The scope of section 56 will be widened and will also cover any kind of gifts in cash or kind or for no consideration with few exemptions and exception 11) MAT book profit calculation aslo ammended 12) Disallowance of expenditure from income from other sources if tds is not deducted 13) Self employed can also claim 20% contribution to NPS as deduction. Regards SOURAV BAGARIA |

|

New Section 234F: Fee for Late filing of return of Income Posted: 02 Feb 2017 08:36 AM PST New Section 234F: Fee for Late filing of return of Income. Returns filed after due dates specified for filing of return under sub-section (1) of section 139. The proposed fee structure is as follows:— (i) Rs. 5,000 if the return is furnished after the due date but on or before the 31st day of December of the assessment year; (ii) Rs.10,000 in any other case. Note: However, in a case where the total income does not exceed five lakh rupees, it is proposed that the fee amount shall not exceed Rs.1000 |

|

Posted: 02 Feb 2017 08:34 AM PST New section 271J: Penalty on professionals for furnishing incorrect information in statutory report or certificate. In order to ensure that the person furnishing report or certificate undertakes due diligence before making such certification, it is proposed to insert a new section 271J so as to provide that if an accountant or a merchant banker or a registered valuer, furnishes incorrect information in a report or certificate under any provisions of the Act or the rules made thereunder, the Assessing Officer or the Commissioner (Appeals) may direct him to pay a sum of Ten thousand rupees for each such report or certificate by way of penalty. NOTE: This amendment will take effect from 1st April, 2017. |

|