Fwd: MUST KNOW FINANCIAL UPDATES -1ST DEC 2015

LUGI CHENNAITEAM

Will your Nominee get the money on your death ?

Did you think that your nominee is the person, who will get all the money legally from your Life Insurance Policy and Mutual funds investments? Ha! That is exactly what you’d think if you aren’t aware of the legal aspects. We assume a lot of things which sounds like they’re obvious, but are not true from the legal point of view. Today, we’ll concentrate on nominations in financial products.

For whom are we earning? For whom are we investing? Who, do we want to leave all our wealth to, in case something happens to us? It might be your children, your spouse, parents, siblings etc., or just a subset of these. You also might want to exclude some people from your list fo beneficiaries!. So you think you will nominate person X in your Insurance policy, and when you are dead and gone, all the money goes to person X and he/she becomes the sole owner? You’re wrong, dude ! It doesn’t work that way. Let’s see how it actually does!

What is a nominee ?

According to law, a nominee is a trustee not the owner of the assets. In other words, he is only a caretaker of your assets. The nominee will only hold your money/asset as a trustee and will be legally bound to transfer it to the legal heirs. For most investments, a legal heir is entitled to the deceased’s assets. For instance, Section 39 of the Insurance Act says the appointed nominee will be paid, though he may not be the legal heir. The nominee, in turn, is supposed to hold the proceeds in trust and the legal heir can claim the money.

A legal heir will be the one whose is mentioned in the will. However, if a will is not made, then the legal heirs of the assets are decided according to the succession laws, where the structure is predefined on who gets how much. For example, if a man during his lifetime executes a will. In the will, he mentions his wife and children as legal heirs, then after his death, his wife and children are the legal owners of his assets. It is essential that one needs to execute a will. It is the ultimate source of truth and replaces the succession law. Nominee can also be one of the legal heirs.

Important

- Mention the Full Name, Address, age, relationship to yourself of the nominee.

- Do not write the nomination in favour of “wife” and “children” as a class. Give their specific names and particulars existing at that moment.

- If the nominee is a minor, appoint a person who is a major as an appointee giving his full name, age, address and relationship to the nominee.

According to law, a nominee is a trustee not the owner of the assets. In other words, he is only a caretaker of your assets. The nominee will only hold your money/asset as a trustee and will be legally bound to transfer it to the legal heirs. For most investments, a legal heir is entitled to the deceased’s assets. For instance, Section 39 of the Insurance Act says the appointed nominee will be paid, though he may not be the legal heir. The nominee, in turn, is supposed to hold the proceeds in trust and the legal heir can claim the money.

A legal heir will be the one whose is mentioned in the will. However, if a will is not made, then the legal heirs of the assets are decided according to the succession laws, where the structure is predefined on who gets how much. For example, if a man during his lifetime executes a will. In the will, he mentions his wife and children as legal heirs, then after his death, his wife and children are the legal owners of his assets. It is essential that one needs to execute a will. It is the ultimate source of truth and replaces the succession law. Nominee can also be one of the legal heirs.

Important

- Mention the Full Name, Address, age, relationship to yourself of the nominee.

- Do not write the nomination in favour of “wife” and “children” as a class. Give their specific names and particulars existing at that moment.

- If the nominee is a minor, appoint a person who is a major as an appointee giving his full name, age, address and relationship to the nominee.

Why is the concept of nominee ?

So you might be wondering, if the nominee does not become the sole owner, why does such a concept of “nominee” exist at all? It’s pretty simple. When you die, you want to make sure that the Insurance company, Mutual fund or your shares should at least get out of the companies and go to someone you trust, and who can further help, in process of passing it to your legal heirs.

Otherwise, if a person dies and hasn’t nominated anyone, your legal heirs will have to go through the process of producing all kind of certificates like death certificates, proof of relation etc., not to mention that the whole process is really cumbersome! (For each legal entity! The insurance company, the mutual funds, for the shares, for the real estate..) . So, to simplify, if a nominee exists, these hassles don’t happen, since the company is bound to transfer all your money or assets to the nominee.The company the goes out of scene & then, it’s between nominee and legal heirs.

So you might be wondering, if the nominee does not become the sole owner, why does such a concept of “nominee” exist at all? It’s pretty simple. When you die, you want to make sure that the Insurance company, Mutual fund or your shares should at least get out of the companies and go to someone you trust, and who can further help, in process of passing it to your legal heirs.

Otherwise, if a person dies and hasn’t nominated anyone, your legal heirs will have to go through the process of producing all kind of certificates like death certificates, proof of relation etc., not to mention that the whole process is really cumbersome! (For each legal entity! The insurance company, the mutual funds, for the shares, for the real estate..) . So, to simplify, if a nominee exists, these hassles don’t happen, since the company is bound to transfer all your money or assets to the nominee.The company the goes out of scene & then, it’s between nominee and legal heirs.

Example of Nomination

Ajay was 58 years old who died recently in an accident. As his children were settled, he wanted to make sure that his wife is the sole owner of all the monetary assets. This includes his insurance policy and mutual funds. So during his lifetime, he nominated his wife as a nominee in his term insurance policy and mutual funds investments. However, after Ajay’s death things didn’t turn up the way he wanted. The reason being Ajay did not leave a will. Though his wife was the nominee in all his movable assets, as per the law, his wife, along with children, were the legal heirs and all of them had equal right to Ajay’s assets.

One simple step which could have saved the situation was that Ajay should have made a will which clearly stated that only his wife was entitled to get all the money and not his children.

Ajay was 58 years old who died recently in an accident. As his children were settled, he wanted to make sure that his wife is the sole owner of all the monetary assets. This includes his insurance policy and mutual funds. So during his lifetime, he nominated his wife as a nominee in his term insurance policy and mutual funds investments. However, after Ajay’s death things didn’t turn up the way he wanted. The reason being Ajay did not leave a will. Though his wife was the nominee in all his movable assets, as per the law, his wife, along with children, were the legal heirs and all of them had equal right to Ajay’s assets.

One simple step which could have saved the situation was that Ajay should have made a will which clearly stated that only his wife was entitled to get all the money and not his children.

Nomination in Life Insurance

A policyholder can appoint multiple nominees and can also specify their shares in the policy proceeds. Nomination in life insurance has one limitation, as insurance policies are bought to secure your financial dependents, your first choice of nominee has to be your family members. In case you want to nominate a non-family member like a friend or third party, you will have to show/PROVE the insurance company that there is some insurable interest for the person. This happens because of a Clause called PRINCIPAL OF INSURABLE INTEREST in insurance. Note that provision of nomination in life insurance is related to Section 39 of the Insurance Act. Note that as per LIC website

Nomination is a right conferred on the holder of a Policy of Life Assurance on his own life to appoint a person/s to receive policy moneys in the event of the policy becoming a claim by the assured’s death. The Nominee does not get any other benefit except to receive the policy moneys on the death of the Life Assured. A nomination may be changed or cancelled by the life assured whenever he likes without the consent of the Nominee.Make sure, you have a nominee for your policy for easy settlement of the claim, if you do not have any nominee mentioned in the policy, it can turn out to be a disaster for your dependents to get a claim.

A policyholder can appoint multiple nominees and can also specify their shares in the policy proceeds. Nomination in life insurance has one limitation, as insurance policies are bought to secure your financial dependents, your first choice of nominee has to be your family members. In case you want to nominate a non-family member like a friend or third party, you will have to show/PROVE the insurance company that there is some insurable interest for the person. This happens because of a Clause called PRINCIPAL OF INSURABLE INTEREST in insurance. Note that provision of nomination in life insurance is related to Section 39 of the Insurance Act. Note that as per LIC website

Nomination is a right conferred on the holder of a Policy of Life Assurance on his own life to appoint a person/s to receive policy moneys in the event of the policy becoming a claim by the assured’s death. The Nominee does not get any other benefit except to receive the policy moneys on the death of the Life Assured. A nomination may be changed or cancelled by the life assured whenever he likes without the consent of the Nominee.Make sure, you have a nominee for your policy for easy settlement of the claim, if you do not have any nominee mentioned in the policy, it can turn out to be a disaster for your dependents to get a claim.

Nomination in Mutual funds

In case of mutual funds, you can nominate up to three people, who can be registered at the time of purchasing the units. While filling in the application form, there is a provision to fill in the nomination details. Even a minor can be a nominee, provided the guardian is specified in the nomination form. You can also change nomination later by filling up a form which is available on the mutual fund company website. Nomination in mutual funds is at folio level and all units in the folio will be transferred to the nominee(s). If an investor makes a further investment in the same folio, the nomination is applicable to the new units also. A non-resident Indian can be a nominee, subject to the exchange control regulations in force from time to time.

In case of mutual funds, you can nominate up to three people, who can be registered at the time of purchasing the units. While filling in the application form, there is a provision to fill in the nomination details. Even a minor can be a nominee, provided the guardian is specified in the nomination form. You can also change nomination later by filling up a form which is available on the mutual fund company website. Nomination in mutual funds is at folio level and all units in the folio will be transferred to the nominee(s). If an investor makes a further investment in the same folio, the nomination is applicable to the new units also. A non-resident Indian can be a nominee, subject to the exchange control regulations in force from time to time.

Nomination in Shares

Quiz for you :). Now you know what a nominee means and who actually gets the money. So if there is a husband H, with wife W and nephew N, and he has nominated his nephew N to be the nominee of his shares in demat account, who will have the legal right to own the shares after husband’s death? If you answer is wife, you are wrong in this case! In case of stocks, it does not work the usual way, if a will does not exist.

In the verdict, Justice Roshan Dalvi struck down a petition filed by Harsha Nitin Kokate, who was seeking permission to sell some shares held by her late husband. The Court noted that as she was not the nominee, she had no ownership rights over the shares. Ms KokaThe’s lawyer had argued that as she was the heir of her husband who had died intestate (without a will), she should have ownership rights of the shares, and be able to do anything with them as she wished. In this case, Ms Kokate’s husband had nominated his nephew in favour of the shares. Justice Dalvi however noted that under the provisions of the Companies Act and the Depositories Act, Acts which govern the transfer of shares, the role of a nominee was different.

“A reading of Section 109(A) of the Companies Act and 9.11 of the Depositories Act makes it abundantly clear that the intent of the nomination is to vest the property in the shares which includes the ownership rights thereunder in the nominee upon nomination validly made as per the procedure prescribed, as has been done in this case.”

Source : Moneylife

It means that if you have not written a will, anyone who has been nominated by you for your shares will be the ultimate owner of those stocks, The succession laws on inheritance will not be applicable but in case, you have made a will, that will be the source of truth.

Quiz for you :). Now you know what a nominee means and who actually gets the money. So if there is a husband H, with wife W and nephew N, and he has nominated his nephew N to be the nominee of his shares in demat account, who will have the legal right to own the shares after husband’s death? If you answer is wife, you are wrong in this case! In case of stocks, it does not work the usual way, if a will does not exist.

In the verdict, Justice Roshan Dalvi struck down a petition filed by Harsha Nitin Kokate, who was seeking permission to sell some shares held by her late husband. The Court noted that as she was not the nominee, she had no ownership rights over the shares. Ms KokaThe’s lawyer had argued that as she was the heir of her husband who had died intestate (without a will), she should have ownership rights of the shares, and be able to do anything with them as she wished. In this case, Ms Kokate’s husband had nominated his nephew in favour of the shares. Justice Dalvi however noted that under the provisions of the Companies Act and the Depositories Act, Acts which govern the transfer of shares, the role of a nominee was different.

“A reading of Section 109(A) of the Companies Act and 9.11 of the Depositories Act makes it abundantly clear that the intent of the nomination is to vest the property in the shares which includes the ownership rights thereunder in the nominee upon nomination validly made as per the procedure prescribed, as has been done in this case.”

Source : Moneylife

It means that if you have not written a will, anyone who has been nominated by you for your shares will be the ultimate owner of those stocks, The succession laws on inheritance will not be applicable but in case, you have made a will, that will be the source of truth.

Nomination in PPF

If the subscriber dies and there is no nomination at the time of death, the balance in the account, if it is upto one lakh, will be paid by the Accounts Office to the legal heirs of the deceased on receipt of application in Form G supported with necessary documents without the production of succession certificate. If the balance is more than one lakh, the production of Succession certificate will be necessary. (source)

If the subscriber dies and there is no nomination at the time of death, the balance in the account, if it is upto one lakh, will be paid by the Accounts Office to the legal heirs of the deceased on receipt of application in Form G supported with necessary documents without the production of succession certificate. If the balance is more than one lakh, the production of Succession certificate will be necessary. (source)

Nomination in Saving/Current/FD/RD Account in Banks

FD’s also come with nomination facility. While opening a new account, there is a column for nomination in the same form and you should fill it. You can nominate two persons with first and second option. Note that in case you have not done any nomination till now, you should request Form No DA-1 from your Bank which is used to assign a nominee in future. (Examples of ICICI Bank , HDFC Bank , Canara Bank) . In the same way to change/cancel the nomination you need to fill up Form no DA-2. Read about Corporate Fixed Deposits

As per a famous case, A Bench of Justices Aftab Alam and R M Lodha in an order said that the money lying deposited in the account of the original depositor should be distributed among the claimants in accordance with the Succession Act of the respective community and the nominee cannot claim any absolute right over it.

Section 45ZA(2)(Banking Regulation Act) merely put the nominee in the shoes of the depositor after his death and clothes him with the exclusive right to receive the money lying in the account.It gives him all the rights of the depositors so far as the depositors’s account is concerned. But it by no stretch of imagination make the nominee the owner of the money lying in the account,” the Bench observed.

FD’s also come with nomination facility. While opening a new account, there is a column for nomination in the same form and you should fill it. You can nominate two persons with first and second option. Note that in case you have not done any nomination till now, you should request Form No DA-1 from your Bank which is used to assign a nominee in future. (Examples of ICICI Bank , HDFC Bank , Canara Bank) . In the same way to change/cancel the nomination you need to fill up Form no DA-2. Read about Corporate Fixed Deposits

As per a famous case, A Bench of Justices Aftab Alam and R M Lodha in an order said that the money lying deposited in the account of the original depositor should be distributed among the claimants in accordance with the Succession Act of the respective community and the nominee cannot claim any absolute right over it.

Section 45ZA(2)(Banking Regulation Act) merely put the nominee in the shoes of the depositor after his death and clothes him with the exclusive right to receive the money lying in the account.It gives him all the rights of the depositors so far as the depositors’s account is concerned. But it by no stretch of imagination make the nominee the owner of the money lying in the account,” the Bench observed.Conclusion

Now you know! Taking Personal finance for granted can be fatal  Just investing knowledge, isn’t enough to have a great financial life. You also need to be well versed with basic legal aspects and make sure you carry out all due arrangement . Nomination is one important aspect you should seriously consider, when checking for the financial products you have bought or plan to buy in future. Mistakes in Personal Finance

Just investing knowledge, isn’t enough to have a great financial life. You also need to be well versed with basic legal aspects and make sure you carry out all due arrangement . Nomination is one important aspect you should seriously consider, when checking for the financial products you have bought or plan to buy in future. Mistakes in Personal Finance

Its important to make sure that your loved one’s do not face legal issues and only say and think lovely thoughts about you when you are not around, rather than crib & grumble . Fix your nominee in all the financial products

Now you know! Taking Personal finance for granted can be fatal Just investing knowledge, isn’t enough to have a great financial life. You also need to be well versed with basic legal aspects and make sure you carry out all due arrangement . Nomination is one important aspect you should seriously consider, when checking for the financial products you have bought or plan to buy in future. Mistakes in Personal Finance

Its important to make sure that your loved one’s do not face legal issues and only say and think lovely thoughts about you when you are not around, rather than crib & grumble . Fix your nominee in all the financial products

Bank Fixed Deposit (FD)-What to do when depositor dies before maturity?

November 30, 2015 by Basavaraj Tonagatti

We all have Bank Fixed Deposit (FD), at least a one. However, have you ever thought of what will happen when depositor dies before maturity? Whether your nominees or family members know the rules?

Recently, one of my blog readers asked this question. His father had some Bank Fixed Deposit (FD). Recently, his father died. Therefore, this reader is in a dilemma of whether to inform the bank now itself and withdraw the money or he has to wait till maturity. Remember, this particular Bank Fixed Deposit (FD) was fixed at a higher interest rate than what it is available now.

Before understanding this common problem. First, let us understand the rights of a nominee in case of Bank Fixed Deposit (FD). It is very much important to appoint nominee in all your financial transactions. Otherwise, you may end up with cases like THIS. In the case of Bank Fixed Deposit (FD), below are the few rights of nominees.

- Nominee acts like trust. He has no rights over the asset. He simply acts as a custodian and makes sure that the deposit must reach to a proper legal heir. However, he can claim the amount only when it is specified under the will or if he inherits the money.

- He is the contact person in case the depositor dies before maturity.

- He has to submit the proof while claiming the amount.

- The nominee must be an individual and one member. HUF, trust or societies can’t appoint nominees.

- If you haven’t appointed nominee during creating Bank Fixed Deposit (FD), you can do so at a later stage too (but before maturity).

In how many ways, we can hold the Bank Fixed Deposit (FD)?

- Joint holding with “Anyone or Survivor” option-This is the best way to deposit. Because, in a case of death of a first holder or joint holder, the survivor may claim the deposit easily. The survivor has to produce the death certificate to the bank. Upon receipt of the same, banks will delete the deceased person’s name and the FD will turn to be in the name of a survivor. In such a situation, the FD is continued as usual and not considered as a death of a depositor.

- Joint holding with “Joint Holding” option-In such types of Bank Fixed Deposit (FD), the holding will be joint. All joint holder’s signature is a must to claim the deposit at maturity. In the event of a death of anyone holder, the surviving holder may claim the rights over deposit by producing the proper documents. In a case of death of both holders, then the money will be payable to a nominee.

- Single holding with “Nomination” option-If depositor dies before maturity, then the maturity proceeds will be payable to a nominee (as a custodian or trust). At a later stage, the amount will be fixed based on the WILL or Succession Certificate.

- Single holding without “Nomination” option-If there is no nomination, then the family members must produce the legal heir proof or a succession certificate to claim the amount. This is the most lengthy process.

The same scenarios are explained in below image when the depositor nominated someone.

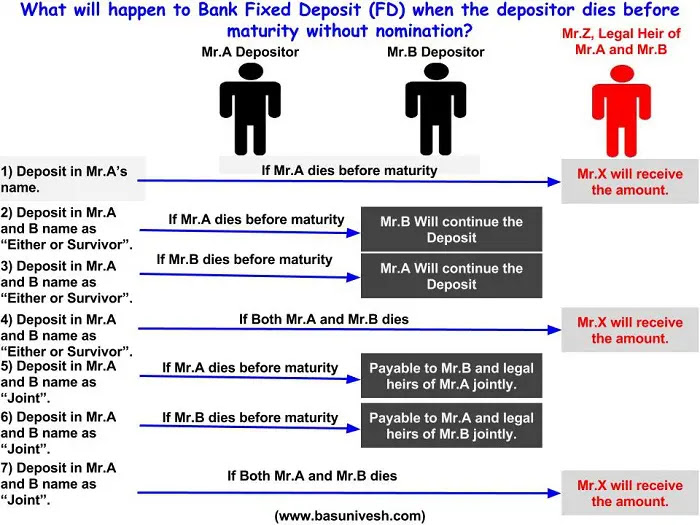

Now what will happen if the depositor not nominated? The process will be difficult to claim for the survivors. The same is explained in below image.

Note-For simplification purpose, I created Mr.Z as legal heir of both Mr.A and Mr.B. However, in reality you may find different. In case of deposit without a nomination, the maturity will be payable to the legal heirs of deceased or any one of them mandated by all the legal heirs.

Documents required to claim the Bank Fixed Deposit (FD) of the deceased person (when the nomination is there)

- Claim Form-This is nothing but a letter to Bank stating that the depositor died and you are being a nominee, claiming the deposit. The format will be available with the Bank.

- Death Certificate-You have to produce the death certificate issued by local authorities.

- Proof of Address and Photo ID-You have to produce the address proof and photo identity of the nominee or the survivor.

Documents required to claim the Bank Fixed Deposit (FD) of the deceased person (when the nomination is not there)

- Succession Certificate from Legal Heirs-You have to produce the succession certificate.

- Indemnity Bond (format will be available with banks).

Whether to continue or withdraw the deposit?

After the death of a depositor, the nominee has two options. One is to continue the FD till maturity. Second is to withdraw it immediately. In the case of withdrawal, banks will not charge any penalty.

You can act according to the current interest rate cycle and the deposit interest rate. Suppose the FD interest rate is around 10% and currently the same bank offering FD at 8%, then it is better to continue the FD till maturity. If there is a reverse situation, then you can withdraw it.

How you receive the maturity amount?

Here RBI had provided two options and are as below.

“a) The bank could be authorized by the survivor(s) / nominee of a deceased account holder to open an account styled as ‘Estate of Shri ________________, the Deceased’ where all the pipeline flows in the name of the deceased account holder could be allowed to be credited, provided no withdrawals are made.OR

- b) The bank could be authorized by the survivor(s) / nominee to return the pipeline flows to the remitter with the remark ‘Account holder deceased’ and to intimate the survivor(s) / nominee accordingly. The survivor(s) / nominee / legal heir(s) could then approach the remitter to effect payment through a negotiable instrument or through ECS transfer in the name of the appropriate beneficiary.“

You notice that claiming deposit when there is no nomination is a hardship. Hence, to avoid this situation, always create FDs with a nomination. Hope this information will be helpful to all.

Power Of Attorney (POA) for Demat and Trading Account-Is it mandatory?

August 6, 2013 by Basavaraj Tonagatti

How many of us read all the lines of the booklet our stock broker give to sign before opening a demat or trading account? Including me very few do in-depth reading and understanding what are the exact clauses and rules. Simply we do sign around 20 signatures and give him all the necessary documents. But do you know what power you are giving him by blindly signing all the documents?

So let us talk one of the power what you are giving your broker i.e. Power of Attorney. Before proceeding further let us understand what is the Power Of Attorney. Simply to say, you are giving in writing the power to another person to do something either specific or generic.

So there are two basic types of Power Of Attorney.

1) General Power Of Attorney-Here the POA holder can perform all activities on behalf of the original holder. Hence, before going for such generic POA you must do take care of the after effect also. It gives more power to POA holder.

2) Specific Power Of Attorney-Here POA holder perform only specific activities on behalf of the original holder which are specified in POA document. This simply restricts POA holder. So this seems to besomewhat secured than General Power Of Attorney.

Within above two basic POAs there are again two more sub categories of POA.

1) Revocable POA-Where you can revoke the rights you have given in POA.

2) Irrevocable POA-Where you can’t revoke the rights you have given in POA.

The two big questions one faces while giving Power Of Attorney to broker for opening demat and trading account are-Whether it is mandatory? If so what type of POA will one can give? After going through the SEBI Circular dated April 23rd 2010 and aftermath clarification about few doubts on the said circular dated Dec 30th 2010 indicates that POA is mandatory only for online accounts but not to offline accounts.

Now what is online and offline account? Online means you login to your account either from your home or office and do trading online by using your stock broker platform. Offline means you specifically instruct your broker to execute the trade by the way of instruction slips for each trade.

So which POA one can give to his broker? Going by SEBI guidelines one must give Specific Power Of Attorney with Revocable Power Of Attorney type. Because it is specifically mentioned that POA you are giving is to act specific transactions on behalf of client and it must be revocable at any time but after clearing your obligations which you owe before cancelling this POA. Stock broker must issue true certified/duplicate copy of POA toclient. In case of merger or demerger of any stock broker or depository participant then one month prior notice should be given to client ask for continue or not with new entity.

Below are the few actions what your broker can do on behalf of you.

1) Securities-

- Transfer of securities towards stock exchange which arise due to trades executed by client on stock exchanges from the same broker.

- To pledge the securities in favor of stock broker for limited period to meet the marginrequirement of the trade executed by client.

- To apply for various products like Mutual Funds, Public Issues, rights, offer of shares etc. based on the client instructions which also includes redemption.

2) Funds-Transfer of funds from client’s bank account in the following cases.

- For meeting settlement obligations and margin requirements for the trade executed by client on stock exchange from the same stock broker.

- For recovering outstanding dues arising out of the client’s trading activity on the stock exchange from the same stock broker.

- For meeting other obligations of client’s subscription to products such as mutual funds, public issues, rights or offer of shares etc.

- For any dues pending as a fee or charges towards maintaining trading account and DP account.

Few important SHALL NOT points to be noted related to POA.

1) Transfer securities for off market trades but other than the parties mentioned in POA.

2) Transfer of the fund from the client’s bank account for the trades executed by client through another stock broker.

3) Opening a trading account with any stock broker or opening depository account with any other depository.

4) Executing trades without client’s consent.

5) Prohibiting issue of delivery instruction slips to beneficial owners.

6) Prohibiting clients from the operating account.

7) Merging balances from other accounts to nullify debit in any other account.

8) Open an email account on behalf of the client to receive statutory transactions.

9) Renouncing from liability arising out of instruction provided by stock broker to block the client’s bank account.

Hope this cleared the doubts of POA related to demat and trading accounts.

There is a huge cry whenever news items appear that LIC profited from equity investment and how much % it is actually holding in a particular company. However, for me as a buyer of Insurance+Investment product this does not

There is a huge cry whenever news items appear that LIC profited from equity investment and how much % it is actually holding in a particular company. However, for me as a buyer of Insurance+Investment product this does not

{kind=link}