If Wage Growth Is Driving Inflation, Why Is Workers’ Share of Income Falling? Dean Baker

0 views

Skip to first unread message

June Zaccone

Apr 24, 2022, 12:02:45 PM4/24/22

to goodjobs list

If Wage Growth Is Driving Inflation, Why Is Workers’ Share of Income Falling? By Dean Baker April 21, 2022

This Isn’t — and Can’t Be — 1970s style inflation

A popular line on our recent surge of

inflation is that an over-tight labor market has led to rapid wage

growth, which in turn forces companies to raise prices. Higher prices in

turn lead workers to demand higher wages, which will give us a

wage-price spiral and soon lead to double-digit inflation.

While this was a story that plausibly fit

the data in the 1970s, it is very hard to make the wage-price spiral fit

the current situation for a simple reason: The wage share of income has

fallen sharply since the pandemic. By wage share I mean total

compensation to workers, including fringe benefits, not just cash wages

and salaries.

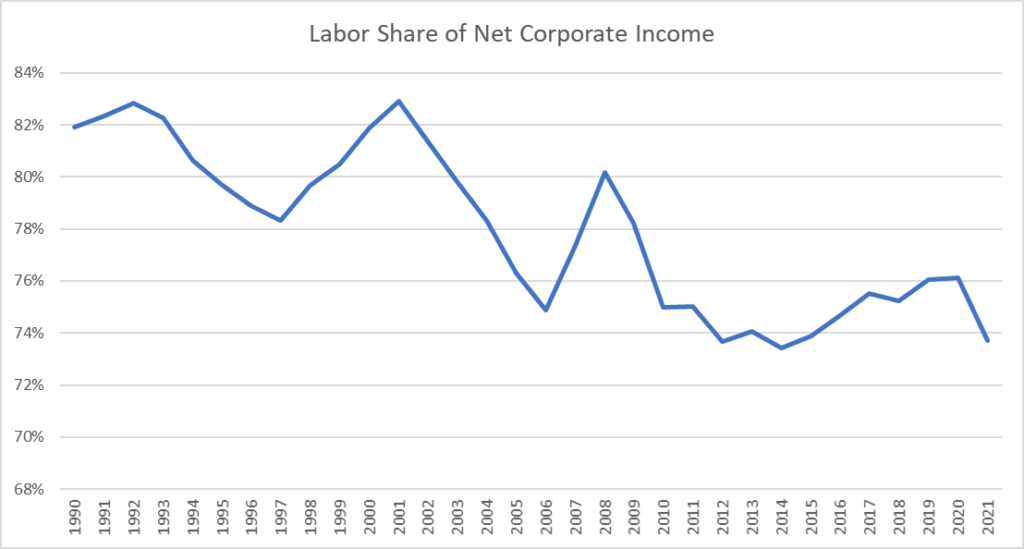

Here’s the picture:

As can be seen, the wage share of corporate

income had been recovering gradually from the troughs it hit in 2014

following the Great Recession. However, we see a sharp reversal in

2021, with the wage share falling from 76.1% to 73.7%, a decline of 2.4

percentage points.

Perhaps some economists can tell a story

where rapid wage growth is driving inflation even as the wage share of

income is falling, but I’m not that good an economist. [Editor’s Note:

“Good” as in dishonest.]

This still looks to me like a case where

supply-side disruptions, associated with the economy reopening from the

pandemic together with the war in Ukraine are driving inflation.

This view is consistent with the fact that

year-over-year inflation in the European Union was 7.5% as of March. The

EU countries did not have as big a stimulus as the United States and by

most measures the EU labor market is not as tight as in the United

States.

--

Reply all

Reply to author

Forward

0 new messages