Mallinckrodt Pharma, which owns Athcar, gets headlines for the multi-billion indication for Amytoophic Lateral Sclerosis thru the melanocortin receptors

Uhohinc

Mallinckrodt: Acthar's Next Multi-Billion-Dollar Indication

Summary

Mallinckrodt's Acthar Gel has been shown to benefit ALS symptoms in a pre-clinical study.

A Phase 2 trial was completed last year, and data analysis is underway.

Mallinckrodt's sales could more than double with success in treating ALS.

Mallinckrodt (NYSE:MNK) is investigating its Acthar Gel as a potential treatment for ALS (amyotrophic lateral sclerosis), also known as Lou Gehrig's disease. An ability to treat ALS would be a huge win for MNK, as it could provide access to a blockbuster-level market with little competition.

MNK is a global specialty biopharmaceutical company, developing a diverse portfolio of products. MNK's sales are 60% specialty brands, 30% specialty generics, and 10% nuclear imaging products.

Acthar is an FDA-approved specialty pharmaceutical used to treat several disorders, including infantile spasms, multiple sclerosis, rheumatoid arthritis, and lupus, among others. It accounts for about half of MNK's specialty brands sales and 30% of its total sales.

MNK supports Acthar clinical studies to develop new efficacy data for a variety of on-label indications and is supporting the ALS study as a potential new indication.

Here's why Acthar is believed to be a useful medication for the treatment of ALS and its investment implications.

ALS

ALS is a relatively rare CNS (central nervous system) disease in which the neurons that control voluntary muscles die. There are 10,000-15,000 cases in the U.S., of which 5-10% are inherited. Typical survivability is 2-5 years after the onset of symptoms. It is a grim disease in which the quality of life rapidly degrades owing to the deterioration of muscle control.

ALS has no cure and only one minimally helpful treatment, Sanofi's (NYSE:SNY) Rilutek, that lengthens survival by up to several months. The expectation is that Acthar will reduce the severity of ALS or slow its progression. Owing to the lack of medical options, there is a low bar for a new drug to show benefit and even a minor one would be welcomed.

Pre-Clinical Evidence

A mouse model using a genetic modification to the SOD1 (superoxide dismutase) gene, which is associated with a subtype of ALS, is currently the best test for pre-clinical drug treatments. SOD1 is an antioxidant enzyme that protects the body from free radicals produced during normal metabolism. A defect in the SOD1 gene can be toxic if either too little or too much gene function occurs. With too much, as in the ALS case, the accumulation of SOD1 may damage proteins and disrupt cellular functions.

In mid-2015, the results from such a study were published showing Acthar reduced this key protein. Acthar treatment accomplished the following:

- "...(Acthar) significantly reduced the levels of soluble SOD1 in the spinal cord and CNS tissue..."; and it

- "...significantly postponed the disease onset and paralysis in the mouse model."

These are very encouraging results. While they could be limited in this case to treatment of effects caused by the SOD1 mutation, there is not enough known about the complex origins and physiology of ALS to determine this.

Another recent mouse study showed that the SOD1 defect leads to a melanocortin (such as ACTH) deficit. This study also extended the results from not only the SOD1 mutation, but also to other mutations, indicating broader physiological relevance and potential for treatment by MCR (melanocortin receptor) activation. In particular, MC3R and MC4R have been implicated in the metabolic signaling of that study.

There are also other physiological reasons to expect a benefit from Acthar, including ACTH's role in reducing inflammation, ameliorating impaired functionality, enhancing motor neurons, and supporting neuron and muscle formation. Hence, multiple ALS pathophysiological pathways could be impacted by Acthar.

This isn't a shot in the dark. It is instead a very promising approach to mitigating some of the terrible effects of ALS.

Phase 2 Trial

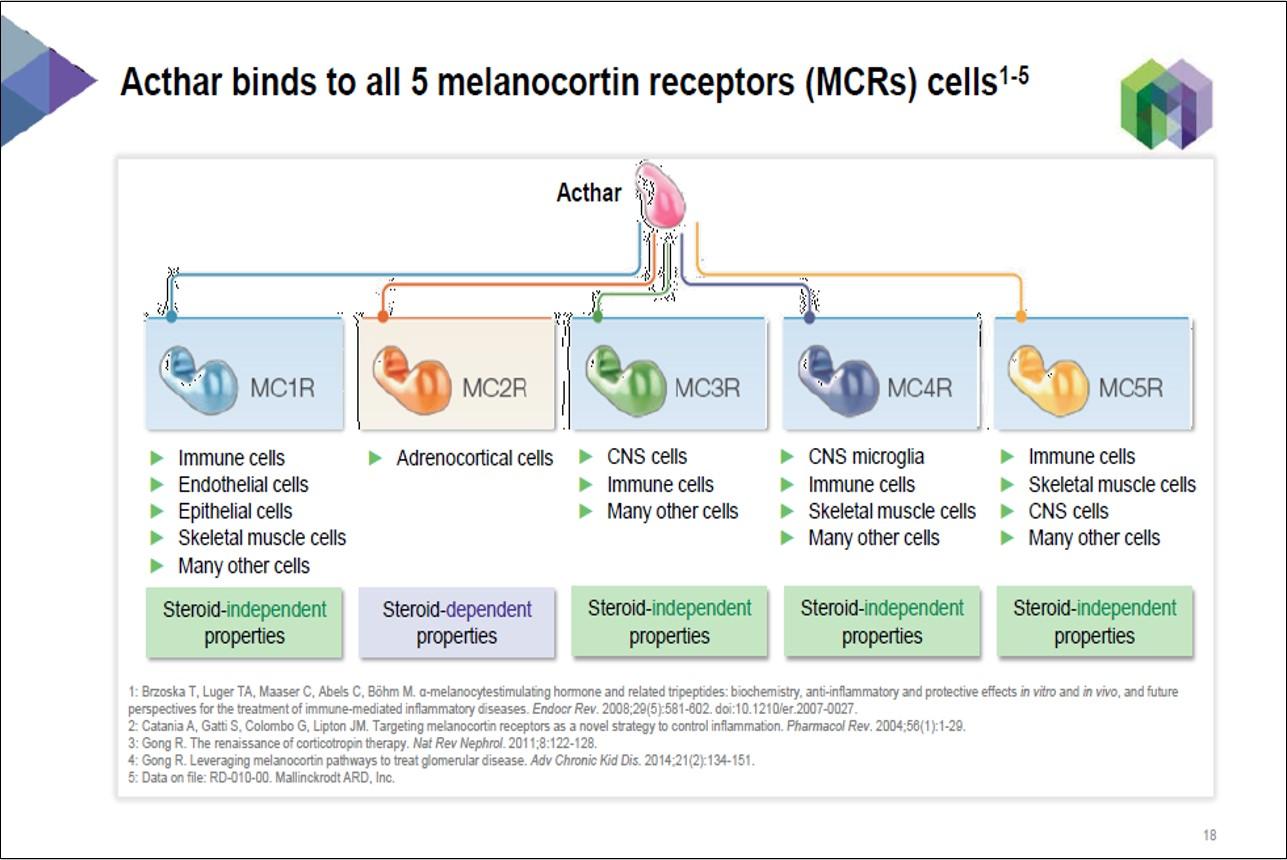

In humans, Acthar binds to multiple CNS relevant MCRs: MC3R, MC4R and MC5R. This links Acthar directly to the pre-clinical studies. Acthar also binds to multiple skeletal muscle cell relevant MCRs, including MC1R and the others just listed.

Note that the melanocortin functionality is in addition to the MC2R steroid-dependent property, which affects only adrenocortical cells. Acthar has different and additional physiological effects in comparison to corticosteroids, which are sometimes used prior to Acthar as a first-line treatment for its other indications.

Click to enlarge

Click to enlarge

MNK's Phase 2 trial explored the safety and tolerability of the use of Acthar in 40 ALS patients over an eight-week period with an option for an extended open-label treatment course for 28 weeks. Four different treatment regimens were explored.

The study included measurements of ALS functional changes through ALSFRS-R (ALS Functional Rating Scale-Revised) test scores. This is a physician-generated estimate of the patient's degree of functional impairment that correlates significantly with the quality of life of ALS patients.

The secondary endpoints included changes in routine clinical lab tests: complete blood count, hemoglobin A1c, chemistry (including serum glucose and lipid panel), serum cortisol, and routine urinalysis; and changes in vital signs: blood pressure, heart rate, and body temperature.

The Phase 2 trial, and any following Phase 3 trial, will seek to determine if the activation of the relevant MCRs impacts ALS patient quality of life by either physician assessment or direct laboratory measurement. It could be an effect as simple as helping patients maintain or gain weight or as complex as extending the ability to speak normally.

According to Mark Trudeau, CEO of MNK, the trial will "...potentially give us some insight as to whether or not we should consider a developmental program for Acthar and ALS." The Phase 2 trial will be used to determine whether or not a Phase 3 trial should be run.

The Phase 2 data analysis was expected to be completed by the end of last year so results could be released any time now.

Investment Implications

Delays in the timing of data releases are negatively correlated with positive results. Generally, the longer it takes, the less likely the results will be positive, but I don't read too much into it at this point. The function doesn't decrease quickly, and MNK may be exceedingly cautious because of the complex nature of ALS and the importance of a treatment benefit to the ALS community.

I estimate the current clinical ALS-treatment success and approval probability at 40% given Acthar is an already approved medication for other indications. But there is a possibility that ALS sub-type sample sizes are too small in the current study to produce meaningful results. On the other hand, if the trial shows efficacy and safety in Phase 2, there is a very high probability, maybe as high as 80%, it would be approved.

What's the value of the ALS market to MNK? Assuming only SOD1 cases and treatment is two vials of Acthar gel weekly at $34k/vial: (2%*10,000)*(2*$34,000)*52 = $700M/year. This is nearly as much as Acthar's current annual sales, indicating the tremendous opportunity ALS treatment represents for MNK.

If Acthar benefits multiple ALS subtypes and reaches just 10% of all patients, that rises to $3.5B/year. Such sales would double MNK's current total revenue, and presumably, its market cap.

Furthermore, if any CNS benefit is observed, MNK could choose to investigate Acthar for the treatment of other melanocortin-signaling related issues, including certain weight disorders and sexual dysfunction.

Conclusion

Pre-clinical data indicates MNK has a good shot at developing a new ALS treatment with Acthar. It's remarkable that Acthar has such broad pharmacological qualities that it's even in the discussion of a potential ALS treatment.

MNK's stock price is currently pretty beaten down, so positive news from the Phase 2 trial could boost the stock price, providing significant upside, while bolstering Acthar's reputation and MNK as a good long-term investment. I view MNK as a buy here around or under $60/share, even if just to speculatively capture the potential price spike that should occur on positive Phase 2 results.

Disclosure: I am/we are long MNK.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Uhohinc

michael jones

MNK are stating that Acthar binds to all 5 MC receptors. I don't think binding to MC2R conveys any benefit over a $10 prednisone tablet. So afamelanotide binds to the 4 other MC receptors with greater efficacy, particularly MC1R. We know this because Acthar does not produce a tan. The weak effects of Acthar can mostly be attributed to its MC1R binding.

Uhohinc

ALS (Amyotrophic lateral sclerosis)

When Dr. Neil Cashman was a resident neurologist back in the mid 1980s, he served in the ALS (amyotrophic lateral sclerosis) clinic at the University of Chicago. It changed his career path.

“I had one year where I had three patients under my care, three teenage women, who died of ALS — and that just drove me up a wall. After that, I wanted more than anything, to do something that could help people with ALS.”

Today, there is still no effective treatment for what Cashman calls “the dreadful disease” which now afflicts approximately 3,000 Canadians and is invariably fatal.

However, as UBC Canada Research Chair in Neurodegeneration and Protein Misfolding, Cashman and his colleagues at the Djavad Mowafaghian Centre for Brain Health (DMCBH) are closing in on an immunotherapy and a possible cure. As Cashman quietly understates: “It would be huge.”

It’s now understood that amyotrophic lateral sclerosis (ALS) is transmitted through the nervous system by misfolded SOD1 (superoxide dismutase 1) protein molecules, which don’t ‘fold up’ in their normal 3-D shape. Instead, they basically turn inside out to display their ‘sticky’ innards, creating what Cashman calls “chaos” within the nerve cell. This chaos is also propagated to adjacent healthy cells in a stealthy cascade of neuron degeneration and death.

Misfolded or distorted proteins or ‘prions’ are also the principal factors in Creutzfeldt-Jakob disease (CJD), Alzheimer’s and Parkinson’s disease and other major human and animal brain and nerve-wasting killers.

In SOD1 deformation, Cashman wondered if a specific drifting fragment of exposed amino acids could be targeted in ALS propagation. He zeroed in on regions that are exposed in misfolded SOD1, and buried in the normally folded form.

The next step was to develop an antibody to specifically chase down and neutralize the SOD1 “bad guys” while ignoring the healthy form, effectively jam up the sticky, exposed innards of the malformed SOD1 protein and thus block ALS propagation at its molecular source.

Cashman and his colleagues have now developed such an antibody. The antibody has been tested in mouse models of ALS, and it works. Cashman says this research has applications for similar brain and nerve diseases. “It’s the same thing for Alzheimer’s, and a preventative vaccine for prion diseases.”

More than two decades on, Cashman can’t forget the awful year at the Chicago ALS clinic that still serves him as a compelling reason to find a cure. Today, at the DMCBH, he’s helping forge possible new futures for those suffering from brain diseases of all types.

For more information on research and ongoing clinical activities at the Djavad Mowafaghian Centre for Brain Health (DMCBH) visit their website.

Thank you to the faculty and researchers from the Djavad Mowafaghian Centre for Brain

Uhohinc

Zero tolerance

Some of us rely heavily upon your tireless research.

Could you explain a bit more thoroughly what risks you see to Clinuvel with regards to Athcar?

Thank you.

Uhohinc

As I recently became acquainted with a person with a tumor on or adjacent to the left anterior lobe of the pituitery and a Cushing's diagnosis I was looking into the effects this disorder creates because of excessive Pomc and therefore adrenocortotropin hormone and melanocyte stimulating hormone and therefore excessive adrenaline above kidneys. I deduct that any patient taking AThcar the drug by Mallinkrodts for the myriad of therapys does receive benefits of ALL melanocortin receptors. But a big but here is the simulation of Cushings Disease. And this disease and effects are very detrimental and lead to early death. Only the positive affects of Athcar at the same time may alleviate, but this is not known and not probable.

Athcar is a dangerous drug the longer one is on it. And any melanocyte stimulating hormone such as Scenesse is going to do a lot of the good of Athcar and more, just no mcr2. And mcr2 is mainly another big unknown of steroidgenisis.

So, it is Athcar and anyone with Cushings that has negatives. All even more positive for Clinuvel and Scenesse.

Uhohinc

Cushings is listed as to watch for with Athcar.

Interesting is the atrophy of the pituitery axis. Could the endocrine parracrine or autocrine signal that normally instigates the production of msh atrophy or the cells in pituitery atrophy after continual long term use.

Uhohinc

Uhohinc

It appears Mallinkrodts is watching and using Clinuvel research in referencing

Uhohinc

Medicare spending on Mallinckrodt drug tops $500 million

Dec 27, 2016, 7:19am CST

Angela Mueller

Reporter

St. Louis Business Journal

Email Twitter LinkedIn Facebook SMS Order Reprints Save Article

Enlarge

IMAGE PROVIDED BY GETTY IMAGES

Get St. Louis Newsletters and Alerts

Morning Edition >> Afternoon Edition >> Breaking News

Enter your email address

Sign Up

A drug produced by Mallinckrodt PLC was the single most expensive drug, per patient, paid for by Medicare last year, according to Medicare data.

Medicare spent an average of $162,371 for the 3,100 beneficiaries using Mallinckrodt's H.P. Acthar Gel, according to New York Times' reporting on the 2015 Medicare Drug Spending Dashboard. Medicare spent a total of $514 million on Acthar in 2015, up 29 percent from 2014. Medicare spending on the drug was $49.5 million in 2011.

H.P. Acthar is used to treat a variety of conditions, including acute cases of multiple sclerosis and rheumatic disorders. Acthar is Mallinckrodt's top-selling drug, accounting for $327 million of the company's fourth-quarter sales of $886.2 million.

PEOPLE ON THE MOVE

Scott Underwood

Scott Underwood

Northwestern Mutual-St.Louis

Ashley Jones

Ashley Jones

Garcia Properties

Tara Hacker

Tara Hacker

Garcia Properties

See More People on the Move

The cost for Acthar has increased from $40 a vial in 2001 to $38,000 today, the New York Times reports. This price increase comes at a time when the U.S. Senate's Special Committee on Aging is taking a close look at price gouging among prescription drug companies, releasing a recent report focused on four companies — Retrophin, Rodelis Therapeutics, Turing Pharmaceuticals and Valeant Pharmaceuticals International.

Mallinckrodt spokesman Daniel Yunger told the Times that Mallinckrodt does not have any of the characteristics that concerned the Aging Committee about those four companies. He pointed out that Acthar is not a drug with no immediate competition and Mallinckrodt does not control access to it through a closed distribution system.

Yunger also noted that Acthar's largest price increases occurred before Mallinckrodt acquired the drug from Questcor in 2014, and since the acquisition, the drug's price increases have averaged in the low single digits, the Times reports.

While Medicare continues to cover Acthar, private insurers such as Aetna, Cigna and UnitedHealthcare have restricted reimbursement for the drug in recent years, the Times reports.

Angela Mueller covers health care.

Uhohinc

Note the 4th quarter sales over last year. Athcar is skyrocketing in sales. $327m would make the next 4 quarters or yearly sales over $1.3billion for just Athcar.

And I think in so many ways Clinuvel's melanocortin is a tremendous improvement on Athcars.

Athcar has no patent protection and no generic. Yet from $40 to $40,000 is an unconsciosable and un fair price increase with no facts to back it up.

These guys did worse than Skhreli but have averted the negative press. Maybe because Turing messed with AIDS activists and their drug.

The small context about no immediate competitive drug by Mallinckrodt spokesperson is of interest. It is now in Mallinckrodts interest to stop or slow down Clinuvel in USA. Everyday Clinuvel is not on market is a net of about $4 million dollars to Mallincrodt.

If I were Mallincrodt I would attempt a takeover of Clinuvel and I would think it worth two years of perceptioned revenues, or in this case to protect my Mallnkot market.

This is also a very good card in Clinuvel's hand when playing poker with FDA and opens options for Clinuvel if and when to use.

And Athcar is in trials to expand into other melanocortin therapies. And an Italian version called Scynthactin is what was used on the Ebola patient.

Uhohinc

I think Mallinkrodt would easily offer Clinuvel up to two years of the Athcar revenues for present Clinuvel. The lesser the better for Mallinkrodt befor a few more years and Clinuvel is a bigger Melanocortin therapy to cannibalize the athcar market.

Mallinkrodt management can deal with Clinuvel now or later when it will cost more.Two years of the growing as of now Athcar sales is about $2.5billion. Mallinkrodt must think Clinuvel has years to go to compete. But Mallincrodt may also fully target the melanocortins and disorders.

Uhohinc

Mallinckrodt Rebounds After FTC Probe; Doubts Rival Will Get FDA Nod

Mallinckrodt on Thursday explained why it settled with the FTC, and shares rebounded. (Shutterstock)

Mallinckrodt on Thursday explained why it settled with the FTC, and shares rebounded. (Shutterstock)

ALLISON GATLIN1/19/2017

Marathon Pharmaceuticals faces an uphill battle developing Mallinckrodt's (MNK) Synacthen in the U.S., analysts said Thursday, after Mallinckrodt agreed to pay $100 million and license the drug in two indications to end an FTC antitrust probe.

In the stock market today, Mallinckrodt stock rose 3.4% to 48.10, after falling as much as 13.7% Wednesday on news of the FTC investigation. Shares closed down 5.9% on Wednesday after earlier touching their lowest price since November 2013.

Per the settlement, Mallinckrodt will pay $90 million within 10 days, an additional $10 million within 90 days and $2 million to reimburse four states' fees. It will also license Synacthen, a synthetic ACTH, to Marathon for treating infantile spasms and nephrotic syndrome.

Mallinckrodt didn't admit to any wrongdoing, but said settling removes "the distraction of litigation." The company can still market Synacthen for other indications across the globe, and it's working to develop the drug as a potential treatment for Duchenne muscular dystrophy.

IBD'S TAKE: Donald Trump has accused drugmakers of "getting away with murder" in how they price their products. Last week, stocks tanked on additional pledges from Trump to ease the prices of pharmaceuticals. See IBD's Industry Themes for the deeper dive.

Are you getting the most out of IBD? Our Getting Started Guide can help!

Ironically, the FTC investigation stems from a 2014 suit by former Turing Pharmaceuticals CEO Martin Shkreli, who alleged that Questcor acquired competing drug Synacthen from Novartis (NVS) in 2013, only to shut it down and then jack up the price on its own drug. Acthar. Mallinckrodt now owns Questcor.

Synacthen has been on the market outside the U.S. for decades. Questcor came under fire in 2008 for bumping the price of a vial of Acthar to north of $29,000 from $1,235. Last year, a vial cost $35,000. The FTC was investigating whether the Synacthen acquisition was to keep Acthar prices high.

Shkreli, though, has been the poster boy for the drug-pricing debate. As Turing's CEO, he acquired Daraprim, an anti-parasitic, and spiked the price to $750 per pill from $13.50. Mylan (MYL), too, has drawn ire from its price boost on EpiPens to $600 for a pair from about $100 when it acquired the product in 2007.

Analysts seemed unconcerned Thursday that Mallinckrodt would have to license the competitive drug in two indications. IS and NS aren't key areas for Mallinckrodt outside the U.S. and it will be difficult, if not impossible, for Marathon to gain FDA approval for use of the drug on babies, Mallinckrodt said.

"This would entail convincing patients or the parents of infant patients in fragile, high-risk populations to forgo existing approved, effective treatments and enroll in an experimental protocol where they risk receiving less effective treatment or no treatment at all," Mallinckrodt said in a statement.

In a conference call with analysts early Thursday, Mallinckrodt executives said they ascribed zero value to IS and NS when they acquired Questcor, according to Mizuho analyst Irina Koffler. The settlement isn't expected to have an impact on Acthar sales.

Koffler kept her buy rating and 85 price target on Mallinckrodt stock. But the stock remains a "conspiracy theory," despite its attractive valuation, until Mallinckrodt can diversify outside Acthar, she said. The firm said at a recent investor gathering it plans to pursue accretive acquisitions to that end.

Uhohinc

Doctoral on its page 12 and 13 indicates in some animal models loss of Pomc neurons affiliation to als

Uhohinc

Mallinckrodt forced to ax ALS study testing its controversial Acthar gel

Mallinckrodt, the current maker of Acthar — a drug first developed in the 1950s — said on Tuesday said it was abandoning its quest to market the gel in patients with Lou Gehrig’s disease.

The company was testing the drug in a phase II study designed to enroll 213 patients — when an independent data and safety monitoring board recommended axing the trial due to the lack of an efficacy signal, and pneumonia occurring at a higher rate in Acthar-treated patients.

The disease, whose cause is largely unknown, garnered international attention after the New York Yankees’ Lou Gehrig abruptly retired from baseball in 1939, after being diagnosed with Amyotrophic lateral sclerosis (ALS), an invariably fatal neurological disorder that attacks nerve cells located in the brain and the spinal cord responsible for controlling voluntary muscles.

advertisement

advertisement

Steven Romano

“It is critical to stress, however, that these findings do not impact the current positive benefit/risk profile of Acthar for use in current on-label indications,” reiterated Mallinckrodt’s chief scientific officer Steven Romano in a prepared statement. Achtar is used to treat infantile spasms in very young children.

Acthar’s list price has been hiked from $40 per vial in 2001 to a whopping $38,892 as of April 2019 — according to a recent Reuters report. Extracted from the pituitary glands of slaughtered pigs, it’s manufactured essentially the same way as it was in the 1950s.

Mallinckrodt $MNK acquired the drug in 2001 with its takeover of Questcor. It’s approved for 19 indications altogether — and accounts for a little over a third of the specialty biopharmaceutical company’s roughly $3.2 billion in net sales last year.

Endpoints News has contacted Mallinckrodt for comment.

The UK-based drugmaker has long elicited the ire of regulatory agencies for its marketing practices, particularly in relation to Acthar. After the Federal Trade Commission — along with the states of Alaska, Maryland, New York, Texas and Washington — alleged Mallinckrodt had taken advantage of its monopoly to repeatedly raise the price of Acthar and acquired the rights to its greatest competitive threat to keep competition at bay, the company agreed in 2017 to part with $100 million to settle those charges. This June, the US Department of Justice joined two whistleblower lawsuits in alleging that the company used a foundation as a conduit to pay illegal kickbacks in the form of copay subsidies for Acthar so it could market the drug as “free” to doctors and patients while increasing its price between 2010 and 2014.

Social image: Mallinckrodt

AUTHOR

Natalie Grover

REPORTER

nat...@endpointsnews.com

Uhohinc

PR Newswire PR NewswireJuly 16, 2019

STAINES-UPON-THAMES, United Kingdom, July 16, 2019 /PRNewswire/ -- Mallinckrodt plc (MNK), a leading global specialty biopharmaceutical company, today announced that it is permanently discontinuing its Phase 2B study designed to assess the efficacy and safety of Acthar® Gel (repository corticotropin injection) as an investigational treatment for amyotrophic lateral sclerosis (ALS). The drug is not U.S. Food and Drug Administration (FDA)-approved for the ALS indication. Please see Important Safety Information for Acthar Gel below.

Mallinckrodt logo

Mallinckrodt logo

More

Mallinckrodt made the decision to halt the trial after careful consideration of a recent recommendation by the study's independent Data and Safety Monitoring Board (DSMB). The DSMB was created by the company following industry best practice to ensure the safety of patients participating in a clinical study. This oversight is accomplished through ongoing review of semi-blinded information as the study is being conducted, and is typically done when there is limited information available in the patient population being studied.

The recommendation was based on the specific concern for pneumonia, which occurred at a higher rate in the ALS patients receiving Acthar Gel compared to those on placebo; the board also mentioned other adverse events specific to this patient population. The DSMB noted the proportion of patients who have completed Week 36 – the primary endpoint target – precludes a definitive determination of a treatment effect. The lack of a clear efficacy signal for this ALS patient population combined with the potential risk of pneumonia led to the board's recommendation.

After careful analysis, Mallinckrodt agreed that the study should be permanently halted in the interest of patient safety for this fragile population, one for which pneumonia is a particularly serious condition. Enrollment in the study will cease immediately, and those patients already enrolled will be tapered off the drug before discontinuing use.

"Mallinckrodt's primary focus is on the safety of patients and, while ALS patients are among those most in need of new therapies and treatment options, we believe this is the right decision. It is critical to stress, however, that these findings do not impact the current positive benefit/risk profile of Acthar for use in current on-label indications," said Steven Romano, M.D., Executive Vice President and Chief Scientific Officer at Mallinckrodt. "Though the probability of success for the ALS population was acknowledged as being low, this study was initiated based on compelling analyses carried out following the completion of a small pilot study and we were hopeful it would have translated into a benefit for this group of patients in great need of effective therapies. We thank the DSMB, the investigators and the patients who participated in the study."

This action does not affect any other ongoing clinical studies for Acthar Gel. Mallinckrodt is committed to responsible and ethical scientific exploration that adds to the body of clinical and economic data for critical illnesses. Mallinckrodt has invested more than $500 million into Acthar Gel's modernization, specifically initiating company-sponsored clinical studies building on substantial clinical experience as well as previously completed and largely independent clinical case series and smaller trials; modernizing manufacturing; and expanding medical affairs and research activities. The company's investment into Acthar Gel and these activities remains an important focus.

About the PENNANT Trial

The Phase 2B clinical study is titled "A Multicenter, Double Blind, Placebo-Controlled Study to Assess the Efficacy and Safety of Acthar Gel in the Treatment of Subjects with Amyotrophic Lateral Sclerosis." The study targeted enrollment of patients ages 18 to 75 with ALS and symptom onset (defined as first muscle weakness or dysarthria) ≤ two years prior to the screening visit. Subjects were randomized on a 2:1 basis to receive subcutaneous (SC) Acthar Gel 0.2 mL (16 units) daily or SC matching placebo 0.2 mL daily for 36 weeks.

The efficacy of Acthar Gel was assessed using standard measures of functional decline, including change from baseline in the ALS Functional Rating Scale-Revised, assessed after 36 weeks of therapy.

About ALS

ALS is a progressive neurodegenerative disease that affects motor neuron cells in the brain and the spinal cord. Motor neurons reach from the brain and the spinal cord to the muscles throughout the body. The progressive degeneration of the motor neurons in ALS eventually leads to their demise and when the motor neurons die, voluntary and involuntary muscle movement is lost. With the progressive loss of motor neurons, people with ALS may lose the ability to speak, eat, move and breathe.1

Acthar Gel (repository corticotropin injection) Indications

Acthar Gel is an injectable drug approved by the FDA for the treatment of 19 indications. Of these, today the majority of Acthar Gel use is in these indications:

Adjunctive therapy for short-term administration (to tide the patient over an acute episode or exacerbation) in rheumatoid arthritis, including juvenile rheumatoid arthritis (selected cases may require low-dose maintenance therapy)

The treatment of symptomatic sarcoidosis

Monotherapy for the treatment of infantile spasms in infants and children under 2 years of age

Treatment during an exacerbation or as maintenance therapy in selected cases of systemic lupus erythematosus

The treatment of acute exacerbations of multiple sclerosis in adults. Controlled clinical trials have shown Acthar Gel to be effective in speeding the resolution of acute exacerbations of multiple sclerosis. However, there is no evidence that it affects the ultimate outcome or natural history of the disease

Inducing a diuresis or a remission of proteinuria in nephrotic syndrome without uremia of the idiopathic type or that due to lupus erythematosus

Treatment during an exacerbation or as maintenance therapy in selected cases of systemic dermatomyositis (polymyositis)

Treatment of severe acute and chronic allergic and inflammatory processes involving the eye and its adnexa such as: keratitis, iritis, iridocyclitis, diffuse posterior uveitis and choroiditis, optic neuritis, chorioretinitis, anterior segment inflammation

IMPORTANT SAFETY INFORMATION

Contraindications

Acthar should never be administered intravenously

Administration of live or live attenuated vaccines is contraindicated in patients receiving immunosuppressive doses of Acthar

Acthar is contraindicated where congenital infections are suspected in infants

Acthar is contraindicated in patients with scleroderma, osteoporosis, systemic fungal infections, ocular herpes simplex, recent surgery, history of or the presence of a peptic ulcer, congestive heart failure, uncontrolled hypertension, primary adrenocortical insufficiency, adrenocortical hyperfunction or sensitivity to proteins of porcine origins

Warnings and Precautions

The adverse effects of Acthar are related primarily to its steroidogenic effects

Acthar may increase susceptibility to new infection or reactivation of latent infections

Suppression of the hypothalamic-pituitary-axis (HPA) may occur following prolonged therapy with the potential for adrenal insufficiency after withdrawal of the medication. Adrenal insufficiency may be minimized by tapering of the dose when discontinuing treatment. During recovery of the adrenal gland patients should be protected from the stress (e.g. trauma or surgery) by the use of corticosteroids. Monitor patients for effects of HPA suppression after stopping treatment

Cushing's syndrome may occur during therapy but generally resolves after therapy is stopped. Monitor patients for signs and symptoms

Acthar can cause elevation of blood pressure, salt and water retention, and hypokalemia. Blood pressure, sodium and potassium levels may need to be monitored

Acthar often acts by masking symptoms of other diseases/disorders. Monitor patients carefully during and for a period following discontinuation of therapy

Acthar can cause GI bleeding and gastric ulcer. There is also an increased risk for perforation in patients with certain gastrointestinal disorders. Monitor for signs of bleeding

Acthar may be associated with central nervous system effects ranging from euphoria, insomnia, irritability, mood swings, personality changes, and severe depression, and psychosis. Existing conditions may be aggravated

Patients with comorbid disease may have that disease worsened. Caution should be used when prescribing Acthar in patients with diabetes and myasthenia gravis

Prolonged use of Acthar may produce cataracts, glaucoma and secondary ocular infections. Monitor for signs and symptoms

Acthar is immunogenic and prolonged administration of Acthar may increase the risk of hypersensitivity reactions. Neutralizing antibodies with chronic administration may lead to loss of endogenous ACTH activity

There is an enhanced effect in patients with hypothyroidism and in those with cirrhosis of the liver

Long-term use may have negative effects on growth and physical development in children. Monitor pediatric patients

Decrease in bone density may occur. Bone density should be monitored for patients on long-term therapy

Pregnancy Class C: Acthar has been shown to have an embryocidal effect and should be used during pregnancy only if the potential benefit justifies the potential risk to the fetus

Adverse Reactions

Common adverse reactions for Acthar are similar to those of corticosteroids and include fluid retention, alteration in glucose tolerance, elevation in blood pressure, behavioral and mood changes, increased appetite and weight gain

Specific adverse reactions reported in IS clinical trials in infants and children under 2 years of age included: infection, hypertension, irritability, Cushingoid symptoms, constipation, diarrhea, vomiting, pyrexia, weight gain, increased appetite, decreased appetite, nasal congestion, acne, rash, and cardiac hypertrophy. Convulsions were also reported, but these may actually be occurring because some IS patients progress to other forms of seizures and IS sometimes mask other seizures, which become visible once the clinical spasms from IS resolve

Other adverse events reported are included in the full Prescribing Information.

Please see full Prescribing Information.

ABOUT MALLINCKRODT

Mallinckrodt is a global business consisting of multiple wholly owned subsidiaries that develop, manufacture, market and distribute specialty pharmaceutical products and therapies. The company's Specialty Brands reportable segment's areas of focus include autoimmune and rare diseases in specialty areas like neurology, rheumatology, nephrology, pulmonology and ophthalmology; immunotherapy and neonatal respiratory critical care therapies; analgesics and gastrointestinal products. Its Specialty Generics reportable segment includes specialty generic drugs and active pharmaceutical ingredients. To learn more about Mallinckrodt, visit www.mallinckrodt.com.

Mallinckrodt uses its website as a channel of distribution of important company information, such as press releases, investor presentations and other financial information. It also uses its website to expedite public access to time-critical information regarding the company in advance of or in lieu of distributing a press release or a filing with the U.S. Securities and Exchange Commission (SEC) disclosing the same information. Therefore, investors should look to the Investor Relations page of the website for important and time-critical information. Visitors to the website can also register to receive automatic e-mail and other notifications alerting them when new information is made available on the Investor Relations page of the website.

CAUTIONARY STATEMENTS RELATED TO FORWARD-LOOKING STATEMENTS

This release includes forward-looking statements with regard to Acthar Gel including expectations specific to this Phase 2B study, as well as its potential impact on patients. The statements are based on assumptions about many important factors, including the following, which could cause actual results to differ materially from those in the forward-looking statements: clinical trial results; satisfaction of regulatory and other requirements; actions of regulatory bodies and other governmental authorities; changes in laws and regulations; issues with product quality, manufacturing or supply, or patient safety issues; and other risks identified and described in more detail in the "Risk Factors" section of Mallinckrodt's most recent Annual Report on Form 10-K and other filings with the SEC, all of which are available on its website. The forward-looking statements made herein speak only as of the date hereof and Mallinckrodt does not assume any obligation to update or revise any forward-looking statement, whether as a result of new information, future events and developments or otherwise, except as required by law.

CONTACTS

Uhohinc

Athcar’s setback in this phase II ALS appears to be immune suppression related leading to pneumonia, which ALS patients are predisposed susceptible.

Most probable this negative effect is thru melanocortin 2, as inferred in the announcement for the stoppping of thetrial.

Athcar is more a percursor hormone that expresses all melanocortins on all healthy immune cells

Clinuvels Sceness has virtually no expression of melanocortin 2 on no cells. For retrospects, Martin Skhreli attempted to buy Athcar but was sniped out with a higher price at the last minute by Mallinckrodt.

Skhreli then set sites on Clinuvel. Ironically in that Athcars price was astronomically raised without the repercussion Skhreli got when he did the same to a Aids drug. This and his cavalier attitude and public self persona brought focus which led to his imprisonment.

Mallinckrodt probably recognizes the disadvantages of its Athcar, and the advantages of melanocyte stimulating hormone/Sceness/Clinuvel.

Uhohinc

https://www.evaluate.com/vantage/articles/analysis/biogen-leads-way-renewed-amyotrophic-lateral-sclerosis-push

Uhohinc

Uhohinc

Advanced SearchGo

- Company sells not-yet-approved drug for Niemann-Pick Disease

- Purchase price includes cash, percentages of future sales

Mallinckrodt Plc received a judge’s approval to sell its neurodegenerative treatment adrabetadex, ensuring the drug’s continued trials and patients’ access while the company’s bankruptcy proceedings continue.

Mandos LLC will pay $1 million and a portion of future sales, up to 6%. Mallinckrodt will also receive an additional $1.5 million if the Federal Drug Administration approves the medication, which treats a rare, fatal childhood disease, Niemann-Pick Type C Disease (“NPC”).

The sale, approved Tuesday by Judge John T. Dorsey of the U.S. Bankruptcy Court for the District of Delaware, also calls for Mandos to pay an additional $500,000 upon approval ...

To read the full article log in.

Learn more about a Bloomberg Law subscription.

Uhohinc

DUBLIN, Oct. 12, 2020 /PRNewswire/ -- Mallinckrodt plc (NYSE: MNK) ("Mallinckrodt" or the "Company") today announced that it has voluntarily initiated Chapter 11 proceedings in the U.S. Bankruptcy Court for the District of Delaware to modify its capital structure, including restructuring portions of its debt, and resolve several billion dollars of otherwise unmanageable potential legal liabilities. Mallinckrodt and all of its subsidiaries are continuing to operate and supply customers and patients with products as normal.

The entities that filed Chapter 11 petitions include Mallinckrodt plc, substantially all of its U.S. subsidiaries, including its specialty generics-focused subsidiaries (collectively, "Specialty Generics") and specialty brands-related subsidiaries (collectively, "Specialty Brands"), and certain of its international subsidiaries.

The Company intends to use the Chapter 11 process to provide a fair, orderly, efficient and legally binding mechanism to implement a restructuring support agreement ("RSA") that, among other things, provides for an amended proposed opioid claims settlement and a financial restructuring that would:

- Reduce the Company's total debt by approximately $1.3 billion, improving the Company's financial position and better positioning it for long-term growth;

- Resolve opioid-related claims against the Company, its subsidiaries and related entities; and

- Resolve various Acthar Gel-related matters, including the CMS Medicaid rebate dispute, an associated False Claims Act ("FCA") lawsuit and an FCA lawsuit relating to Acthar's previous owner's interactions with an independent charitable foundation.

Taken together, these actions are intended to enable the Company to move forward with its vision to become an innovation-driven biopharmaceutical company meeting the needs of underserved patients with severe and critical conditions.

Mark Trudeau, President and Chief Executive Officer of Mallinckrodt, said, "After many months of deliberation, negotiation and consideration of alternatives, Mallinckrodt's management and Board of Directors determined that implementing a Chapter 11 restructuring provides the best opportunity to maximize the value of the enterprise and position the Company for the future in light of the current challenges it faces. The actions we are taking are an important step forward for Mallinckrodt and our patients, employees, customers, suppliers and other partners. We have worked diligently over the last several months to evaluate all available options to achieve a comprehensive resolution to the significant litigation and debt issues overhanging our business. Having entered our restructuring support agreement and reached agreements in principle with a key group of opioid plaintiffs, other governmental parties and our guaranteed unsecured noteholders, we are beginning this process in a highly organized manner. We are now on a clear path to eliminating legal uncertainties, maximizing enterprise value, strengthening our balance sheet and moving ahead with our strategic plans. At the same time, we remain committed to improving health outcomes and developing and bringing to market therapies for patients with severe and critical conditions."

Trudeau continued, "We are grateful to our employees for their continued commitment to our customers and the patients we serve. We also thank our suppliers and business partners for their support as we continue working together to improve the lives of patients."

Overview of Key RSA Terms

In connection with the Chapter 11 filing, the Company has entered into an RSA that provides for a financial restructuring designed to strengthen the Company's balance sheet and reduce its total debt by approximately $1.3 billion, improving the Company's financial position and allowing the Company to continue driving its strategic priorities and investing in the business to develop and commercialize therapies to improve health outcomes.

Parties to the RSA include:

- Holders of approximately 84% of the Company's guaranteed unsecured notes;

- 50 states and territories; and

- The court-appointed plaintiffs' executive committee representing the interests of thousands of plaintiffs in the opioid multidistrict litigation1 ("Opioid MDL"), which has agreed to recommend that the more than 1,000 counties, municipalities (including cities, towns and villages), Native American tribes and other opioid claimants in the Opioid MDL support the RSA.

Under the terms of the RSA, at the end of the court-supervised process:

- All allowed First Lien Credit Agreement Claims, First Lien Note Claims and Second Lien Note Claims are expected to be reinstated at existing rates and maturities;

- Holders of allowed Guaranteed Unsecured Note Claims are expected to receive their pro rata share of $375 million of new secured second lien notes due seven years after emergence and 100% of New Mallinckrodt Ordinary Shares, subject to dilution by the warrants described below and certain other equity;

- Trade creditors and holders of allowed General Unsecured Claims are expected to share in

- $150 million in cash; and

- Equity holders and non-guaranteed unsecured noteholders are expected to receive no recovery.

Amended Proposed Opioid Settlement

The Company has reached an agreement in principle on the terms of an amended proposed settlement that would resolve opioid-related claims against Mallinckrodt and its subsidiaries and eliminate billions of dollars in alleged liabilities. The amended proposed settlement is supported by a broad array of opioid plaintiffs as detailed above.

Under the terms of the amended proposed settlement, which would become effective upon Mallinckrodt's emergence from the Chapter 11 process, subject to court approval and other conditions:

- Opioid claims would be channeled to one or more trusts, which would receive $1.6 billion in structured payments.

- $450 million would be received upon the Company's emergence from Chapter 11;

- $200 million would be received on each of the first and second anniversaries of emergence; and

- $150 million would be received on each of the third through seventh anniversaries of emergence with a one-year prepayment option at a discount for all but the first payment.

- Opioid claimants would also receive warrants for approximately 19.99% of the Company's fully diluted outstanding shares, including after giving effect to the exercise of the warrants, exercisable at a strike price reflecting an aggregate equity value of $1.551 billion.

- Upon commencing the Chapter 11 filing, the Company will comply with an agreed-upon operating injunction with respect to the operation of its opioid business.

Copies of term sheets outlining the terms of the RSA and the amended opioid settlement, as well as materials with additional information relating to the Company and its Chapter 11 filing, are available on www.advancingmnk.com. The term sheets and additional materials are expected be filed as an exhibit to a Current Report on Form 8-K with the U.S. Securities and Exchange Commission tomorrow.

Resolution of Certain Acthar Gel-Related Matters

Mallinckrodt has reached an agreement in principle with certain governmental parties to resolve certain disputes relating to Acthar Gel. The agreement in principle is conditioned upon Mallinckrodt entering the Chapter 11 restructuring process. The Company has agreed to pay $260 million over seven years and reset Acthar Gel's Medicaid rebate calculation as of July 1, 2020, such that state Medicaid programs will receive 100% rebates on Acthar Gel Medicaid sales, based on current Acthar Gel pricing. Additionally, upon execution of the settlement, the Company will dismiss its appeal of the CMS Medicaid rebate ruling currently pending in the U.S. Court of Appeals for the D.C. Circuit. The settlement would resolve the CMS Medicaid rebate dispute, the associated FCA lawsuit in Boston and an FCA lawsuit in the Eastern District of Pennsylvania relating to Acthar's previous owner's interactions with an independent charitable foundation.

Mallinckrodt expects to complete the settlement over the next several months, subject to Bankruptcy Court approval.

Continuing to Serve Patients and Customers as Normal

The current consolidated cash balance of the Chapter 11 filing entities is more than $650 million. Together with cash generated from ongoing operations, this is expected to provide ample liquidity to support continued operations during the court-supervised process.

The Company has filed a number of customary motions seeking court authorization to continue to support its business operations during the court-supervised process, including the continued payment of employee wages and benefits without interruption. The Company intends to pay vendors and suppliers in full under normal terms for goods received and services rendered on or after the filing date. The Company expects to receive court approval for all of these routine requests. The Company's foreign non-debtor affiliates will continue to operate their businesses in the ordinary course.

Separating the Specialty Generics and Specialty Brands businesses remains one of Mallinckrodt's goals. The Company will continue to evaluate strategic options for the Specialty Generics business at an appropriate time and when market conditions are favorable.

Additional Information

Additional information about the court-supervised process is available at www.advancingmnk.com. Court filings and other information related to the court-supervised process are available on a separate website administered by the Company's claims agent, Prime Clerk, at http://restructuring.primeclerk.com/Mallinckrodt; by calling Prime Clerk representatives toll-free in the U.S. and Canada at 877-467-1570 or 347-817-4093 for international calls; or by emailing Prime Clerk at Mallinck...@primeclerk.com.

For supplier-related inquiries, please call the Company toll-free in the U.S. at +1-833-954-2209 or +1-314-654-3008 for international calls, or email the Company at Supplier...@mnk.com.

Advisors

Latham & Watkins LLP, Ropes & Gray LLP and Wachtell, Lipton, Rosen & Katz are serving as counsel, Guggenheim Securities, LLC is serving as investment banker and AlixPartners LLP is serving as restructuring advisor to Mallinckrodt. Hogan Lovells is serving as counsel with respect to the Acthar Gel matter.

About Mallinckrodt

Mallinckrodt is a global business consisting of multiple wholly owned subsidiaries that develop, manufacture, market and distribute specialty pharmaceutical products and therapies. The company's Specialty Brands reportable segment's areas of focus include autoimmune and rare diseases in specialty areas like neurology, rheumatology, nephrology, pulmonology and ophthalmology; immunotherapy and neonatal respiratory critical care therapies; analgesics and gastrointestinal products. Its Specialty Generics reportable segment includes specialty generic drugs and active pharmaceutical ingredients. To learn more about Mallinckrodt, visit www.mallinckrodt.com.

Mallinckrodt uses its website as a channel of distribution of important company information, such as press releases, investor presentations and other financial information. It also uses its website to expedite public access to time-critical information regarding the company in advance of or in lieu of distributing a press release or a filing with the U.S. Securities and Exchange Commission (SEC) disclosing the same information. Therefore, investors should look to the Investor Relations page of the website for important and time-critical information. Visitors to the website can also register to receive automatic e-mail and other notifications alerting them when new information is made available on the Investor Relations page of the website.

CAUTIONARY STATEMENTS RELATED TO FORWARD-LOOKING STATEMENTS

Statements in this document that are not strictly historical, including statements regarding future financial condition and operating results, legal, economic, business, competitive and/or regulatory factors affecting Mallinckrodt's businesses, and any other statements regarding events or developments the company believes or anticipates will or may occur in the future, may be "forward-looking" statements within the meaning of the Private Securities Litigation Reform Act of 1995, and involve a number of risks and uncertainties.

There are a number of important factors that could cause actual events to differ materially from those suggested or indicated by such forward-looking statements and you should not place undue reliance on any such forward-looking statements. These factors include risks and uncertainties related to, among other things: the proposed settlement with governmental parties to resolve certain disputes relating to Acthar Gel; the possibility that such settlement will not be consummated and the risks and uncertainties related thereto, including the time and expense of continuing to litigate this dispute and the impact of this dispute on Mallinckrodt's financial condition and expectations for performance; the impact of the outbreak of the COVID-19 coronavirus; the bankruptcy process, the ability of Mallinckrodt and its subsidiaries to obtain approval from the bankruptcy court with respect to motions or other requests made to the bankruptcy court throughout the course of the Chapter 11 cases and to negotiate, develop, obtain court approval of, confirm and consummate the plan of reorganization contemplated by the restructuring support agreement or any other plan that may be proposed, the effects of the Chapter 11 cases, including increased professional costs, on the liquidity, results of operations and businesses of Mallinckrodt and its subsidiaries; the consummation of the transactions contemplated by the restructuring support agreement, including the ability of the parties to negotiate definitive agreements with respect to the matters covered by the term sheets included in the restructuring support agreement, the occurrence of events that may give rise to a right of any of the parties to terminate the restructuring support agreement and the ability of the parties to receive the required approval by the bankruptcy court and to satisfy the other conditions of the restructuring support agreement; governmental investigations and inquiries, regulatory actions and lawsuits brought against Mallinckrodt by government agencies and private parties with respect to its historical commercialization of opioids, including the amended non-binding agreement in principle reached by Mallinckrodt in connection with the announcement of its filing of the Chapter 11 petitions regarding the terms and conditions of a global settlement to resolve all current and future opioid-related claims; Mallinckrodt's ability to comply with the continued listing criteria of the New York Stock Exchange (the "NYSE") and risks arising from the potential suspension of trading of Mallinckrodt's ordinary shares on, or delisting from, the NYSE and the effects of Chapter 11 on the interests of various constituents; scrutiny from governments, legislative bodies and enforcement agencies related to sales, marketing and pricing practices; pricing pressure on certain of Mallinckrodt's products due to legal changes or changes in insurers' reimbursement practices resulting from recent increased public scrutiny of healthcare and pharmaceutical costs; the reimbursement practices of governmental health administration authorities, private health coverage insurers and other third-party payers; complex reporting and payment obligations under the Medicare and Medicaid rebate programs and other governmental purchasing and rebate programs; cost containment efforts of customers, purchasing groups, third-party payers and governmental organizations; changes in or failure to comply with relevant laws and regulations; Mallinckrodt's and its partners' ability to successfully develop or commercialize new products or expand commercial opportunities; Mallinckrodt's ability to navigate price fluctuations; competition; Mallinckrodt's and its partners' ability to protect intellectual property rights; limited clinical trial data for Acthar Gel; clinical studies and related regulatory processes; product liability losses and other litigation liability; material health, safety and environmental liabilities; potential indemnification liabilities to Covidien pursuant to the separation and distribution agreement; business development activities; retention of key personnel; the effectiveness of information technology infrastructure including cybersecurity and data leakage risks; customer concentration; Mallinckrodt's reliance on certain individual products that are material to its financial performance; Mallinckrodt's ability to receive procurement and production quotas granted by the U.S. Drug Enforcement Administration; complex manufacturing processes; conducting business internationally; Mallinckrodt's ability to achieve expected benefits from restructuring activities; Mallinckrodt's significant levels of intangible assets and related impairment testing; labor and employment laws and regulations; natural disasters or other catastrophic events; Mallinckrodt's substantial indebtedness and its ability to generate sufficient cash to reduce its indebtedness; future changes to U.S. and foreign tax laws or the impact of disputes with governmental tax authorities; and the impact of Irish laws.

These and other factors are identified and described in more detail in the "Risk Factors" section of Mallinckrodt's Annual Report on Form 10-K for the fiscal year ended December 27, 2019 and Form 10-Q for the fiscal quarter ended June 26, 2020. The forward-looking statements made herein speak only as of the date hereof and Mallinckrodt does not assume any obligation to update or revise any forward-looking statement, whether as a result of new information, future events and developments or otherwise, except as required by law.

CONTACTS

Investor Relations

Daniel J. Speciale

Vice President, Finance and Investor Relations Officer

314-654-3638

daniel....@mnk.com

Media

Michael Freitag / Aaron Palash / Aura Reinhard

Joele Frank, Wilkinson Brimmer Katcher

212-355-4449

Government Affairs

Mark Tyndall

Senior Vice President, Government Affairs

& Chief Counsel, Litigation

202-459-4141

mark.t...@mnk.com

1Captioned In re National Prescription Opiate Litigation, Case No. 17-md-2804 (N.D. Ohio).

2Mallinckrodt, the "M" brand mark and the Mallinckrodt pharmaceuticals logo are trademarks of a Mallinckrodt company. Other brands are trademarks of a Mallinckrodt company or their respective owners. © 2020 10/20.

View original content to download multimedia:http://www.prnewswire.com/news-releases/mallinckrodt-secures-broad-consensus-with-key-stakeholders-on-comprehensive-chapter-11-restructuring-301149931.html