* 2/12/26 - Civic Federation - Setting the Stage for the FY2027 Illinois State Budget + Understanding H.R. 1: How Federal Tax Code Changes Could Impact Illinois ..

Buzz Sawyer

https://www.civicfed.org/setting-stage-fy2027-illinois-state-budget

Setting the Stage for the FY2027 Illinois State Budget

February 12, 2026

The State of Illinois (Illinois or ‘the State’) enters the FY2027 budget process at a pivotal moment. After several years of improved fiscal stability, marked by the reduction of the State’s bill backlog, incremental reserve building, and progress toward mitigating chronic structural deficits, the long-standing baseline fiscal pressures are tightening the State’s finances. While recent federal tax law changes initially raised concerns about substantial revenue losses, the State has taken steps to partially mitigate those impacts through decoupling from portions of the federal tax code to preserve corporate income tax revenues. Most of those effects are felt in the current 2026 fiscal year. Revenue performance this fiscal year has also been better than anticipated, which will help offset the revenue impacts associated with federal policy changes in the current year.

However, the fiscal outlook heading into FY2027 is shaped by slowing revenue growth, rising costs, the phase-out of one-time federal pandemic aid, and increasing uncertainty surrounding federal funding for core state programs. The Governor’s Office in the fall projected an FY2027 operating budget gap of $2.2 billion, driven by a structural imbalance between recurring revenues and largely fixed costs (pensions and debt), as well as federal impacts, including increased costs to administer SNAP food assistance. Together, these pressures leave the State with limited budgetary flexibility.

The FY2027 budget warrants close attention, given heightened economic uncertainty and increasing exposure to factors beyond the State’s direct control. Federal policy changes, enacted in H.R. 1, passed by Congress last summer, along with emerging federal funding reductions, delays, and cost-shifting, will affect tax revenues, healthcare financing, and safety-net programs in future years. With fixed costs continuing to consume a significant share of General Funds, discretionary choices remain constrained, amplifying the consequences of forecasting errors or policy missteps.

Where the State Stands Entering the FY2027 Budget Process

Overview of Illinois’ Current Fiscal Position and Revenue Performance

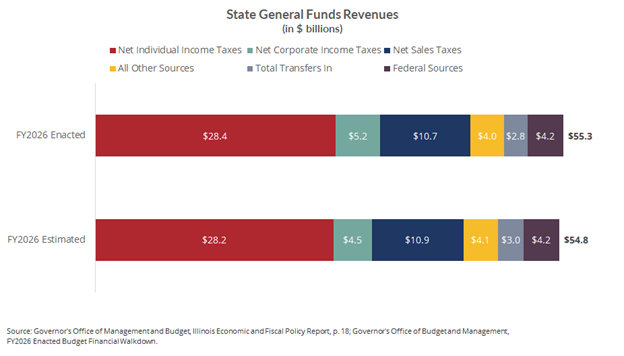

According to the Governor’s Office of Management and Budget’s (GOMB) October estimates, Illinois faces a modest but material general funds deficit of $267 million in the current fiscal year. Higher-than-expected expenditures on pensions and debt service slightly contribute to the gap, but revised revenue projections stemming from the impacts of H.R. 1 are the principal factor. Specifically, changes to the federal tax code and other corporate income tax changes will reduce income tax revenues by $981 million in FY2026. These factors have reduced expected general funds resources to $54.8 billion, down nearly $450 million, or 0.8%, from expected levels reflected in the balanced budget passed last year, despite better-than-expected sales tax revenues and other sources that increased revenues by $532 million.

Federal Policy Impacts and Revenue Risks

H.R. 1 (July 2025)

Illinois’ revenue base is particularly sensitive to federal tax policy changes due to its reliance on income taxes. As a result, federal actions under H.R. 1 have had outsized impacts on State revenues. Several H.R. 1 tax-related provisions, most notably expanded business expensing and changes to the treatment of international income, reduce the amount of income subject to taxation. Because Illinois’ income tax base is closely tied to federal definitions of taxable income, these federal changes flow through to the State absent legislative action, reducing Illinois’ expected income tax revenues by more than $830 million in FY2026 alone.

In response, GOMB recommended targeted “decoupling” from the most impactful federal provisions, including bonus depreciation and updates related to the transition from Global Intangible Low-Taxed Income (GILTI) to Net Controlled Tested Income (NCTI). During the 2025 Veto Session, the Illinois General Assembly enacted legislation to partially decouple the State’s income tax base from federal changes related to NCTI and the expensing of certain structural investments. This action reduced the projected revenue loss by more than $230 million, or 28.0%, lowering the estimated income tax revenue reduction to about $600 million in FY2026.

In addition to the revenue impacts of H.R. 1, Illinois’ share of SNAP administrative costs will increase sharply beginning in FY2027 as the federal match declines from 50% to 25%, adding roughly $80 million in annual state costs.

In FY2028, the State may also be required to fund a portion of SNAP benefit costs if payment error rates remain above federal thresholds. And on the healthcare front, new federal limits on Medicaid provider taxes are scheduled to phase in beginning in FY2028, reducing Medicaid-related revenues.

Most Recent Federal Funding Freeze (January 2026)

In early January 2026, the U.S. Department of Health and Human Services announced the freezing of $10 billion in social service and child care funding across five states, including Illinois. This action affects funds for the Child Care and Development Block Grant, Temporary Assistance for Needy Families (TANF) program, and the Social Services Block Grant. These programs collectively support childcare services, low-income families, and human services providers.

While the duration and scope of the freeze remain uncertain, the action underscores Illinois’ growing exposure to federal funding volatility. The governor’s office estimates that about $1 billion in federal funding could be withheld from state programs, though the actual impacts will depend on subsequent federal decisions and program-specific guidance.

Although this action has not yet been incorporated into official State revenue or expenditure forecasts, it highlights a broader fiscal risk facing Illinois and other states: federal funding reductions, delays, or policy changes that are difficult to predict and challenging to offset with State resources. Given the limited discretionary capacity within the General Funds budget, even temporary disruptions in federal support for healthcare and human services could strain State operations and funding priorities.

Recent Progress and Remaining Structural Constraints

Over the past several years, the State has made sustained progress in stabilizing its finances, including normalizing the bill payment cycle, reducing outstanding debt, and partially rebuilding reserves. While higher reserves improve resilience to short-term shocks, they are a buffer rather than a solution. These gains improve liquidity and reduce near-term risk but do not meaningfully change the share of the budget committed to statutorily required expenditures. Roughly 64% of projected General Funds expenditures in FY2027 will be devoted to fixed or largely nondiscretionary costs.

While the FY2026 enacted budget remains balanced on paper, it relied in part on targeted revenue increases and one-time or temporary measures, such as fund sweeps, to close emerging gaps. Such tools can preserve near-term balance but do not address the underlying mismatch between recurring revenues and expenditure growth.

Spending Pressures and Cost Drivers

Increases in spending in FY2026 and projected outyears are concentrated in pensions, healthcare, education, and other required costs. Growth in healthcare spending, particularly Medicaid, is a key driver of projected expenditure growth, driven by underlying cost trends and federal policy changes. Education funding commitments further contribute to baseline spending growth. Within human services, recent federal policy changes affecting SNAP increase state administrative and fiscal exposure. The FY2026 enacted budget shows notable increases in human services and healthcare spending, signaling baseline cost growth likely to carry into FY2027.

Long-Term Fiscal Outlook

GOMB Multi-Year Projections

GOMB’s five-year outlook projects that—excluding the decoupling measured passed in October 2025 and absent additional policy adjustments—Illinois’ fiscal position will experience significant budget gaps over time as revenue growth fails to keep pace with expenditure demands. The October 2025 projected imbalance of revenues and expenditures is projected to be $2.2 billion in FY2027, which will continue to expand in subsequent years, reaching $5.3 billion by FY2031.

The $2.2 billion budget deficit estimated by GOMB for FY2027 is due to the federal tax code changes and the start of the reduced funding and increased costs for SNAP. Although GOMB’s official projections do not incorporate the federal funding freeze announced in January 2026, the action adds fiscal risk on top of the structural gaps already identified in the forecast.

Drivers of Out-Year Gaps

Growth in pension obligations, education spending, Medicaid and other healthcare costs, and constrained revenue performance drive the structural gaps in the multi-year outlook. Pension contributions are scheduled to rise under existing law. At the same time, healthcare spending continues to grow faster than overall revenue, resulting in a persistent mismatch between recurring revenues and the cost of maintaining existing services. Additional federal policy changes, including scheduled limits on Medicaid provider taxes, are expected to add pressure in the later years of the forecast.

Over the five-year period, General Fund revenues are expected to grow at an annualized growth rate of 2.1%, while expenditures are projected to increase at an annualized growth rate of 3.7% per year. This persistent gap between revenue growth and expenditure growth indicates that Illinois’ fiscal challenge in the out-years is structural and will not be resolved absent policy changes or sustained economic outperformance.

What to Watch for in the FY2027 Budget Proposal

As the Governor prepares to release the FY2027 budget proposal, central considerations include how to address slowing revenues, whether known cost increases are fully acknowledged, how reserves are treated, and how the State is positioned to manage federal uncertainty.

The FY2026 enacted budget shows that the State has limited capacity to backstop significant federal funding losses. As a result, any reduction in federal support will place pressure on state operations and spending priorities, making it difficult to offset with State resources, and underscoring the importance of how the FY2027 budget addresses potential federal reductions in healthcare and human services.

The State has taken targeted actions to mitigate some federal revenue impacts. The General Assembly adopted partial decoupling measures consistent with recommendations from GOMB, reducing projected income tax revenue losses in FY2026. Whether additional adjustments are pursued will be an important indicator of the State’s revenue strategy.

The Governor’s office has also taken administrative steps in response to federal uncertainty, including directing agencies to prepare for potential reductions and to reserve a portion of appropriations. Together, these actions point to a cautious budget approach focused on managing risk amid constrained resources.

Illinois’ recent fiscal progress has improved its capacity to manage near-term challenges, particularly compared to previous budget cycles marked by chronic deficits and liquidity stress. Stronger revenues, a normalized payment bill cycle, and targeted actions to mitigate federal tax impacts provide a more stable foundation entering FY2027.

At the same time, GOMB’s projections and recent federal actions indicate that the margin for error has narrowed. Structural cost pressures continue to outpace revenue growth, and the State faces increasing exposure to federal funding reductions, cost shifts, and policy uncertainty, particularly in healthcare and human services. These risks are difficult to address within a budget where most resources are already committed to fixed or nondiscretionary obligations.

As the Governor prepares to release the FY2027 budget proposal on February 18, the key question is not whether the budget balances in the coming year, but whether it realistically accounts for known cost drivers and federal uncertainty without relying on short-term solutions that shift risk forward. And, it must be noted, the choices made in the FY2027 budget will carry implications beyond the coming fiscal year. The Civic Federation will be paying close attention to how the Governor proposes to close the $2.2 billion structural budget gap and position the State to manage fiscal challenges that extend beyond a single fiscal year.

Related Research

Understanding H.R. 1: How Federal Tax Code Changes Could Impact Illinois

On the Right Track: Illinois' New Transit Agency and Path to Sustainability

Understanding H.R. 1: How New Federal Rules Could Reshape SNAP in Illinois

GOMB Report Projects Pressure on Illinois’ Budget Amid Federal Policy Changes

Federal Shutdown Threatens Food Assistance for Illinois Families

State of Illinois FY2026 Budget Roadmap: Landscape, Issues, and Recommendations

Understanding H.R. 1: How Federal Tax Code Changes Could Impact Illinois

Executive Summary

As the State of Illinois (Illinois or ‘the State’) budget season approaches, the Civic Federation continues its work on the State’s fiscal outlook and potential budget issues likely to emerge in the next few months. In previous reports, we have considered the State’s fiscal outlook as of mid-fall and explored how federal H.R. 1, signed into law on July 4, 2025, may affect the Supplemental Nutrition Assistance Program (SNAP). In this “explainer,” we continue our focus on H.R. 1, particularly its tax code provisions. We describe selected changes and their impacts on Illinois, assess the State’s responses to date, and briefly discuss other policy adjustments the state might consider going forward.

H.R. 1, the Budget Reconciliation Bill, passed by Congress last summer and signed into law on July 4, 2025, as P.L. 119-21, significantly revised federal individual and business income tax provisions. Illinois is among 26 states whose state income tax code “rolls with” changes in the federal Internal Revenue Code (IRC), meaning federal tax changes automatically affect state tax liabilities unless the state legislature intervenes to “decouple.” While rolling conformity simplifies tax administration and compliance for taxpayers, especially those operating in multiple states, full conformity can expose a state to considerable and often unpredictable shifts in revenue.

Illinois faced an over $830 million revenue loss in the current 2026 fiscal year from all federal tax code changes included in last year’s federal legislation, primarily due to changes to business taxation—most notably, expanded “expensing” provisions that allow corporations to immediately deduct the full cost of certain investments.

To mitigate these negative fiscal impacts, Illinois passed Senate Bill 1911, enacted into state law as Public Act (P.A.) 104-0453 in December 2025. This post highlights three specific provisions of Illinois’s new law:

- First, the State formally “decoupled” from provisions related to the expensing of investments in qualified production property, which is nonresidential real property used in the manufacturing, production, or refining of tangible personal property, saving the state an estimated $144 million in FY2026.

- Second, the State essentially chose to conform with federal changes to treatment of international income earned by corporations with foreign subsidiaries: by tweaking its own legal definition of foreign income to align with the federal definition, the state protects an additional $90 million in tax revenues in FY2026.

- Third, P.A. 104-0453 removed the sunset date of Illinois’s pass-through entity tax “workaround”, providing continued federal tax relief to individuals subject to the SALT (state and local tax) deduction cap.

These changes, combined with better-than-expected sales tax and individual income tax revenues received to date, will help the State close a projected $267 million budget gap in FY2026. The changes will also contribute modestly to closing a far larger projected $2.2 billion gap in FY2027—a gap which reflects essentially flat revenues due to slowing growth and continuing H.R. 1 impacts in the face of a $1.9 billion increase in expenditures.

Going forward, Illinois must weigh the administrative simplicity and economic incentives of tax code conformity against the need for local fiscal stability, making selective, strategic decisions on federal-state tax alignment in a world where federal-state relationships are undergoing significant change.

Why Federal Tax Policy Matters To Illinois

Illinois is one of 26 states whose income tax provisions “roll with” changes in the federal Internal Revenue Code (IRC). That is, Illinois’s income tax structure has rolling conformity with federal tax provisions, automatically aligning with the current IRC. Explicit state action is typically needed to “decouple” the state’s provisions from the federal code.[1] In general, alignment through conformity simplifies state tax returns, benefiting both taxpayers and tax administrators, including taxpayers with tax liabilities in multiple states.

Non-conformity, on the other hand, adds complexity to tax compliance, as “documenting and tracking the differences between federal and state taxable income invariably leads to audit issues”. So why don’t states fully conform and simply adopt federal code provisions as-is? Well, it’s complicated.

Some federal IRC changes will help states while others will hurt them, so states may selectively conform or decouple based on predicted revenue impacts on their budgets. More generally, because non-conformity provides states with greater fiscal autonomy in managing their affairs and preserving state tax revenues, states may act “to protect their budgets and residents from unpredictable or unfavorable federal tax policy changes," according to one expert.

Under the pre-H.R. 1 status quo, Illinois, like many states, had selectively decoupled from and conformed to various tax provisions, resulting in a somewhat complex tax structure. For instance, the State had long ago decoupled from net operating loss provisions and from Section 168(k) bonus depreciation provisions. With H.R. 1’s changes, Illinois faced negative and significant revenue impacts: in the absence of state action, the Governor’s Office of Management and Budget (GOMB) estimated in October 2025 that H.R. 1’s tax code provisions would cost the State of Illinois over $830 million in tax collections in FY2026 alone. Further, it is worth noting that Illinois is not alone in facing potential revenue hits from H.R. 1: the Tax Foundation’s state-level estimates point to billions of dollars in revenue losses should states simply allow H.R. 1’s changes to flow through to their state-specific income tax codes.

Thus, Illinois and other states face choices: conform or decouple, provision by provision? Spoiler alert: Illinois, like some other states, has so far acted to protect its revenues, decoupling from provisions that threaten to decrease state tax collections (but potentially boost business investment) and embracing provisions that promise to protect or increase state tax collections.[2]

Illinois’ Response to H.R. 1

For individuals, H.R. 1’s provisions serve to increase deductions from income in multiple ways—for example, through exclusion of tips income and by allowing auto loan interest deductions. At the federal level, these provisions reduce taxable income, thereby decreasing individual tax liabilities. At the state level, however, Illinois is unaffected because the “starting point” for the State’s individual income taxation is the federal measure of adjusted gross income (AGI)—that is, income before standardized and itemized deductions. H.R. 1’s “below the line” deductions, therefore, affect federal but not state taxable income and liabilities.[3] Further, these deductions seem unlikely to generate meaningful investment incentives. On balance, then, Illinois officials can essentially ignore these federal tax code changes, as they have little to no direct effect on the state treasury.

The situation for business taxes is quite different. We discuss three key H.R. 1 business tax provisions below:

- H.R. 1 aimed to incentivize business investment by reducing federal tax liabilities, primarily via more generous “expensing” provisions, which allow business taxpayers to “write off” (deduct) more—indeed, sometimes all!—of a given business investment during the year in which it is made;

- It changed the tax treatment of corporations operating internationally; and

- It increased the state & local tax deduction cap on individuals from $10,000 to $40,000.

Absent state action, some of these changes would increase state tax collections, while others would decrease those revenue streams. In the fall, the Governor’s Office released a report estimating the negative revenue impacts to Illinois, anticipated to exceed $830 million in FY2026 alone. In response, the Illinois legislature passed Senate Bill 1911 during its fall veto session, decoupling from selected provisions expected to decrease tax collections and essentially retaining conformity with certain provisions expected to increase tax collections. The legislation, now signed by the Governor as P.A. 104-0453, will mitigate the impact of H.R. 1 and help close an estimated $267 million operating budget gap for FY2026.

Expensing of Certain Business Investments

H.R. 1 allows businesses to immediately deduct the full cost of “qualified production property” investments, thereby incentivizing investments in structures and facilities by manufacturers and other producers. This Internal Revenue Code Section 168(n) deduction is available for investments on or after January 20, 2025, as long as the property is placed in service by the end of 2030, and the provision has numerous rules that must be met before it can be applied.

Under prior law, businesses typically had to amortize such investments over time—up to 39 years in many cases; that is, they could deduct from income only a portion of their investments according to set depreciation schedules. As argued elsewhere, depreciation makes sense from an accounting perspective (“What is the value today of a machine installed two years ago?”) but not from a tax perspective. By permitting full expensing—full deductions from income in the year of the investment--instead of amortizing over many years, the new provision significantly decreases taxable income in the near term. Expensing increases the present value of these deductions from income, providing potentially powerful incentives for firms to increase their investments in production facilities.[4]

Implications for Illinois

Increased income tax deductions directly imply lower taxable business income, and, absent state action, Illinois faced an estimated FY2026 tax revenue loss of $144 million; the Tax Foundation’s estimate was $153 million. P.A. 104-0453 “undoes” this expensing provision by requiring businesses to add back their “bonus” depreciation deductions for these investments to their adjusted gross income. The “price” of this decoupling, of course, is added complexity in tax administration and weakening of the business investment incentives Congress intended to create via H.R. 1.

Treatment of International Income

Prior to the passage of H.R. 1, U.S. firms with foreign subsidiaries were subject to a global intangible low-taxed income (GILTI) tax intended to discourage profit-shifting, whereby firms shifted profits to low-tax jurisdictions (countries). According to the Tax Policy Center, GILTI was “intended to approximate the income from [highly mobile] intangible assets (such as patents, trademarks, and copyrights) held abroad.” By adding GILTI to a firm’s taxable income and subjecting it to corporate income taxation, the federal government sought to discourage aggressive shifts of these assets to low-tax countries. This pre-H.R. 1 regime was complicated, involving offsets, credits for foreign taxes paid, deductions (“qualified business asset investment” (QBAI) exclusion), and various approximations. Still, in essence, it served (imperfectly) to limit the under-taxation of corporate income earned abroad.

H.R. 1 made several key changes to the tax treatment of business income earned abroad, essentially aiming to broaden the tax base while providing increased credits for foreign taxes paid. These changes included:

- Changing the name of the tax from GILTI to NCTI, or “Net CFC Tested Income” (NCTI), where CFC refers to controlled foreign corporations in which U.S. shareholders own more than 50% of the corporation.

- Eliminating the QBAI, bringing all foreign net income into the tax base.

- Reducing an income deduction from 50% to 40%, also increasing the tax base.

- Increasing the credit for foreign taxes paid from 80% to 90%, which decreased the tax base.

These changes, along with new provisions related to where and how firms can deduct certain expenses from income, thus reducing taxable income and tax liabilities, were expected to be revenue neutral or even generate net tax cuts at the federal level.

Implications for Illinois

H.R. 1’s changes to the treatment of income earned by foreign subsidiaries are expected to have opposite effects on state corporate income tax collections: that is, conformity would likely raise state corporate income tax collections, not decrease them. Two factors underpin this perverse effect: Illinois, like most states, does not allow deductions from business income of foreign taxes paid; and its “single-sales factor” apportionment rule means that the share of a corporation’s income subject to Illinois state taxation equals the share of the firm’s domestic—excluding foreign—sales that took place in Illinois. Both features (no deductions for foreign taxes paid and apportionment based on domestic sales only) increase the tax base and tax liabilities of corporations active in Illinois that also earn international income.

While Illinois conformed to the pre-H.R. 1 GILTI regime, it did so by referring specifically to GILTI by statute—meaning that under H.R. 1, absent state action, Illinois would lose the ability to include foreign-earned income in its corporate income tax base at all. To retain substantive conformity with the new federal rules, P.A. 104-0453 tweaked the concept of taxable income to refer to GILTI or NCTI. In other words, the legislation changed the definition of international income to align with that of H.R. 1. This change meant that Illinois would continue to collect the additional revenues expected when it changed its own treatment of GILTI at the start of FY2026.[5]

Thus, in this instance, the State chose to essentially conform to the new provisions, protecting $90.0 million in state corporate income tax revenues in FY 2026. In this instance, the State’s choice of conformity eases compliance and protects state revenues, but it does so at the expense of fairness in taxation: state taxable income increases with foreign tax payments, thus exacerbating the “double taxation” implicit in this structure; and domestic-based apportionment shares continue to punish firms with high levels of foreign-derived gross sales.

SALT Cap and Pass-Through Entity Tax Provisions

Another H.R. 1 provision of interest has no direct impact on state revenues but warrants mention nonetheless. Specifically, H.R. 1 increases the individual cap on itemized SALT (state and local tax) deductions from $10,000 to $40,000, with a phaseout for high-income taxpayers. The change is effective for tax years 2025-2030. Increasing the cap provides federal tax relief, primarily to high-income taxpayers and those living in states with higher state and local taxes.[6]

Because the SALT cap, first put in place in the 2017 TCJA, applies to individuals and not to pass-through entities such as partnerships and S-corporations, many states—including Illinois—created tax law workarounds to allow the entities to pay the individual state and local taxes. These pass-through entity taxes (PTET) are reported and paid by the business entities themselves—without facing the limitation placed on individuals—before distributing taxable income to individual owners, who would be subject to the cap if paying the taxes at the individual level. Illinois’s PTET, established via P.A. 102-0658 in 2021, was set to expire at the end of 2025, and P.A. 104-0453 removed this sunset date.

While not direct determinants of the State’s income tax collections, the SALT cap and PTET workaround have complicated the recent treatment and categorization of income tax payments made by pass-through entities in Illinois. In fact, a large increase in tax payments by pass-through entities since 2021 led to overstated corporate income tax revenues and understated individual income tax revenues—and to painful if temporary “true-ups” of revenue classifications and “claw-backs” of related personal property tax replacement tax (PPRT) revenues directed to local governments. With the PTET provisions now made permanent, near-term state income tax collections are best viewed in aggregate as the sum of individual and corporate income taxes, as the recategorization and true-up processes work through the system.

What Might Come Next

The State’s economic and fiscal policy report and its recent update highlight H.R. 1’s potential budgetary impacts from tax code changes, as well as programmatic changes to Medicaid and SNAP, and fiscal threats from other potential shifts in federal policies and priorities. P.A. 104-0453 “undoes” significant negative tax-code driven revenue impacts for FY2026, though there remain significant expected tax-related impacts in current FY2026, in part due to complexities related to effective dates, estimated tax payment deadlines, and final tax payment dates.

Of the remaining H.R. 1 tax-related provisions, the one with the largest revenue impact in FY2026 is the return of full expensing of research and experimental (R&E) expenditures. Hence, one future possibility is that the State chooses to decouple somewhat from this federal policy. Other states may do the same during this budget cycle: For example, Governor Kathy Hochul of New York has proposed a FY2027 budget that would decouple from both the R&D provision and the “bonus depreciation” provisions, saving the State an estimated $1.4 billion in revenues.

Nonetheless, the changes enacted in Illinois so far, combined with better-than-expected sales tax and individual income tax revenues received to date, will help the State close a projected $267 million budget gap in FY2026. The changes will also contribute modestly to closing a far larger projected $2.2 billion gap in FY2027—a gap which reflects essentially flat revenues due to slowing growth and continuing H.R. 1 impacts in the face of $1.9 billion more in expenditures.

In fact, recently updated projections indicate that as of mid-fiscal year, the State was on track to meet its general funds revenue target of $55.3 billion in the current fiscal year, as weakness in corporate income taxes and federal funding has been offset by strength in individual income and sales taxes. That said, there remains considerable uncertainty about revenues in the second half of the current fiscal year, not to mention unpredictable federal government policies and priorities that pack a significant fiscal punch. The Governor’s recommended budget, due to be released on February 18, will no doubt reflect the most recent assessments of economic conditions, federal government supports, and revenue dynamics, and the Civic Federation will share its analysis and recommendations as appropriate over the next few months.

Related Research

Setting the Stage for the FY2027 Illinois State Budget

On the Right Track: Illinois' New Transit Agency and Path to Sustainability

Understanding H.R. 1: How New Federal Rules Could Reshape SNAP in Illinois

GOMB Report Projects Pressure on Illinois’ Budget Amid Federal Policy Changes

Federal Shutdown Threatens Food Assistance for Illinois Families

State of Illinois FY2026 Budget Roadmap: Landscape, Issues, and Recommendations

References

[1]Alternatively, states may have what is called “static” conformity, based on the current federal IRC, or based on a statutory “as of” date. These states may have to update statutory references to effectively conform or decouple from the federal IRC provisions as they desire.

[2]Delaware passed legislation in November 2025 to decouple from several provisions related to business investments, essentially forcing businesses to amortize those investments over five years instead of taking deductions all at once. In October 2025, California updated its “as of” conformity date from January 1, 2015 to January 1, 2025 but also explicitly decoupled from several provisions of P.L. 119-21. Both states estimated significant positive revenue effects from their changes.

[3]States whose tax codes start from federal taxable income, instead of AGI, would see decreased taxable incomes, hence expect negative revenue impacts from the provision.

[4]A simple example may clarify these points. Suppose a firm is considering making a facilities investment of $60.0 million. If the firm uses “straight-line” depreciation over three years’ time, it deducts $20.0 million in expenses each year (0, 1, and 2) from its income, yielding $58.3 million in the present value of deductions from income (assuming a discount rate of 3.0%). Under expensing, the firm deducts the full cost at the time of the investment. Deductions from income would thus be $60.0 million in year 0, followed by no deductions in the next two years. In present value terms under expensing, the deductions amount to $60.0 million. The ultimate value of these accelerated deductions to taxpayers depends on several factors: expensing is particularly valuable when tax rates are high, future incomes are low, and discount rates are high.

[5] Prior to passage of P.A. 104-0006 in the spring of 2025, Illinois treated GILTI as a foreign dividend, which was generally eligible for a 100% dividends-received deduction (DRD), meaning it was effectively not taxed at the state level. With that legislation, Illinois effectively decoupled from the full federal deduction and allowed only a 50% DRD for GILTI. This change was expected to increase the state tax base for corporations with foreign subsidiaries and generate significant state tax revenues in FY 2026--$264 million according to one estimate.

[6]Note that prior to the 2017 Tax Cuts and Jobs Act (TCJA), there was no such cap in place; TCJA served to increase federal tax liabilities relative to a no-cap regime, as taxpayers who itemize can only deduct a limited amount of their state and local taxes.