scikit-learn as optional dependency - case: covariances

37 views

Skip to first unread message

josef...@gmail.com

Sep 18, 2016, 12:26:55 PM9/18/16

to pystatsmodels

One set of tools that we need for various models are covariance or

precision (inverse covariance) estimators that are penalized,

sparsified or robust to outliers. (*)

I was looking at the related scikit-learn functionality and that's too

much code and implementation details to copy or duplicate it in

statsmodels.

So, I think it would be useful to add scikit-learn as optional

dependency and wrap it for some optional alternative implementation or

methods. A possible pattern would be to have a simple version of our

own, and delegate fancier methods to scikit-learn.

One implementation detail is for example cross-validation and the

choice of regularization, shrinkage or thresholding. I don't know

whether it's a theoretical or an implementation problem, but k-fold

likelihood cross-validation doesn't seem to work well if the data has

nobs > k_vars.

I ran into CV problems in

https://github.com/statsmodels/statsmodels/issues/3197 but I also seem

to run into problems with scikit-learn GraphLassoCV.

an example based on the scikit-learn example with larger nobs and less sparsity

n_samples = 600

n_features = 20

alpha=0.7 # sparsity in random sample

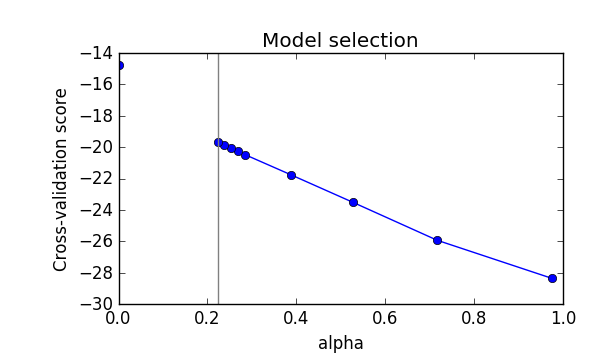

graph lasso cross-validation doesn't converge for small positive

regularization and over sparsifies. In the range that CV is plotted,

the CV score looks monotonic decreasing.

The Ledoit-Wolf estimate in the plot has been changed to thresholding

at a semi arbitrary partial correlation threshold of 0.05, and that

looks good

>>> (prec == 0).mean() # true, data generating zero entries in inverse covariance (precision) matrix

0.40999999999999998

>>> (lwp == 0).mean() # zeros in thresholded ledoit_wolf precision matrix

0.39500000000000002

>>> ((lwp == 0) & (prec == 0)).mean() common

0.34999999999999998

>>> ((lwp != 0) & (prec == 0)).mean() false non-zeros

0.059999999999999998

>>> ((lwp == 0) & (prec != 0)).mean() false zeros

0.044999999999999998

----

(*)

sparse: there is no way to estimate an even a bit larger VAR or VECM

model without a lot of sparsity. sparse inverse covariance is needed

for efficient estimation

outlier robust: We need a robust version of something like Mahalanobis

distance to remove the distorting effect influential outlier

observations.

penalized/shrunk: We need regularized covariances, shrunk but not

necessarily sparse, when we cannot estimate covariances with good

statistical precision, e.g. for robust sandwich covariance, GMM

weights or GEE correlations.

Josef

precision (inverse covariance) estimators that are penalized,

sparsified or robust to outliers. (*)

I was looking at the related scikit-learn functionality and that's too

much code and implementation details to copy or duplicate it in

statsmodels.

So, I think it would be useful to add scikit-learn as optional

dependency and wrap it for some optional alternative implementation or

methods. A possible pattern would be to have a simple version of our

own, and delegate fancier methods to scikit-learn.

One implementation detail is for example cross-validation and the

choice of regularization, shrinkage or thresholding. I don't know

whether it's a theoretical or an implementation problem, but k-fold

likelihood cross-validation doesn't seem to work well if the data has

nobs > k_vars.

I ran into CV problems in

https://github.com/statsmodels/statsmodels/issues/3197 but I also seem

to run into problems with scikit-learn GraphLassoCV.

an example based on the scikit-learn example with larger nobs and less sparsity

n_samples = 600

n_features = 20

alpha=0.7 # sparsity in random sample

graph lasso cross-validation doesn't converge for small positive

regularization and over sparsifies. In the range that CV is plotted,

the CV score looks monotonic decreasing.

The Ledoit-Wolf estimate in the plot has been changed to thresholding

at a semi arbitrary partial correlation threshold of 0.05, and that

looks good

>>> (prec == 0).mean() # true, data generating zero entries in inverse covariance (precision) matrix

0.40999999999999998

>>> (lwp == 0).mean() # zeros in thresholded ledoit_wolf precision matrix

0.39500000000000002

>>> ((lwp == 0) & (prec == 0)).mean() common

0.34999999999999998

>>> ((lwp != 0) & (prec == 0)).mean() false non-zeros

0.059999999999999998

>>> ((lwp == 0) & (prec != 0)).mean() false zeros

0.044999999999999998

----

(*)

sparse: there is no way to estimate an even a bit larger VAR or VECM

model without a lot of sparsity. sparse inverse covariance is needed

for efficient estimation

outlier robust: We need a robust version of something like Mahalanobis

distance to remove the distorting effect influential outlier

observations.

penalized/shrunk: We need regularized covariances, shrunk but not

necessarily sparse, when we cannot estimate covariances with good

statistical precision, e.g. for robust sandwich covariance, GMM

weights or GEE correlations.

Josef

{kind=link}

{kind=link}

Reply all

Reply to author

Forward

0 new messages